For your convenience, you can now securely pay your tax preparation bill online! Our team continues to focus on the ease of our clients’ experience through secure and simple options to do business with us. It is as easy as 1, 2, 3 to view your invoice and pay it with a credit card or direct from a bank account via QuickBooks. Our website has a quick reference guide so you know what to expect: http://www.valleynationalgroup.com/webpay

YOU HAVE OPTIONS! We strive to make your financial life as simple as possible. Please use the method of payment that is most convenient for you – online, in person, over the phone, by mail.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

US ECONOMIC HEAT MAP

The health of the US economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

CONSUMER SPENDING

A+

Consumer spending is expected to strengthen as individuals with lower tax rates spend their windfalls.

FED POLICIES

C-

The Federal Reserve increased the Fed Funds Rate by 0.25% in March, and is expected to implement at least 2 more hikes this year. Rising interest rates tend to reduce economic growth potential and can lead to repricing of income producing assets.

BUSINESS PROFITABILITY

A-

4th quarter earnings season was stellar, with S&P profits growing at a fast pace. Q1 2018 earnings season starts in just a few short weeks.

EMPLOYMENT

A+

The unemployment rate currently stands at 4.1%, the lowest reading since 2000. The economy added 313,000 new jobs in February, a very strong number.

INFLATION

B

Inflation is often a sign of “tightening” in the economy, and can be a signal that growth is peaking. The inflation rate remains benign at this time, but we see the potential for an increase moving forward. This metric deserves our attention.

OTHER CONCERNS

INTERNATIONAL RISKS

5

The above ratings assume no international crisis. On a scale of 1 to 10 with 10 being the highest level of crisis, we rate these international risks collectively as a 5. These risks deserve our ongoing attention.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

The Friday before Easter is the only non-federal holiday among the exchange’s nine closed days. The New York Stock Exchange has been closed every Good Friday for more than 150 years, with the exception of 1898, 1906, and 1907.

Why? Several myths surrounding this market closure exist. The stories range of religious agreements, to historically low trade volume, to good old fashioned superstitions about bad luck. Whatever the reasons, the long-standing tradition remains.

The other eight stock market holidays in the U.S. are New Year’s Day, Martin Luther King Jr.’s birthday, Washington’s Birthday, Memorial Day, Independence Day, Labor Day, Thanksgiving and Christmas.

The show airs on WDIY Wednesday evenings, from 6-7 p.m. The show is hosted by Valley National’s Laurie Siebert CPA, CFP®, AEP®. This week Laurie will discuss:

“Potpourri of taxes – extensions, estimates, 2018 planning.”

Laurie will take your calls on this or other topics. This show will be broadcast at the regular time WDIY is broadcast on FM 88.1 for reception in most of the Lehigh Valley; and, it is broadcast on FM 93.9 in the Easton and Phillipsburg area– or listen to it online from anywhere on the internet. For more information, including how to listen to the show online, check the show’s website www.yourfinancialchoices.com and visit www.wdiy.org.

by Connor Darrell, Head of InvestmentsCLICK HERE TO GET TO KNOW CONNOR It was another bumpy week on Wall Street, though markets closed out the month of March and rolled into the holiday weekend on a positive note. Bonds outperformed stocks as the 10 year treasury yield slipped down to 2.77% after reaching as high as 2.94% during the middle of the prior week. A lot has been made of tariffs and trade policy over the past few weeks, and we touched upon that a bit in last week’s update, but moving forward our primary focus is elsewhere. See below for more details.

What We Are Focusing On As investment managers, we must always be challenging ourselves to identify possibilities that markets haven’t yet appreciated. After all, a portfolio manager who follows the common “consensus” will never outperform. Sound risk management is about recognizing risks in the market before they have major impacts on asset returns, and identifying strategies that can mitigate their effects on a portfolio. As such, we are constantly asking ourselves “What could conceivably transpire that would cause us to fundamentally change our market outlook?”

Following years of historically low levels of volatility, we believe that the equity sell-offs in February and March were simply a return to what might be considered “normal”, and that economic fundamentals remain supportive of further gains. However, as we evaluate the state of the economy and markets, we see two interrelated risks that could temper our optimism; interest rates and inflation.

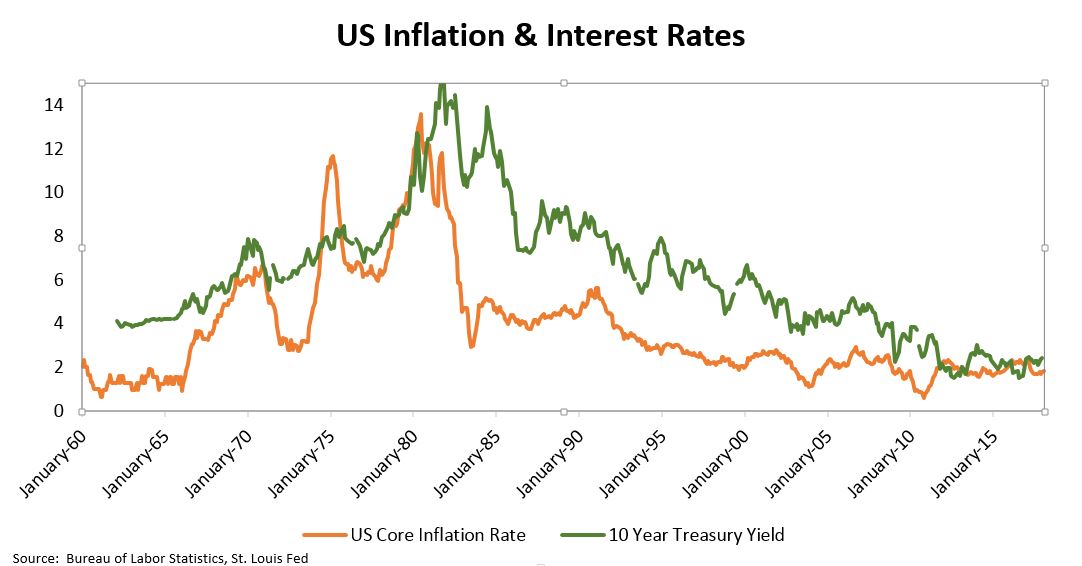

Since the 2008 financial crisis, central banks around the world have taken extreme measures to try and breathe life back into the global economy. Pushing interest rates lower and lower in an attempt to encourage lending and stimulate the economy. Over longer periods of time however, interest rates are driven primarily by inflation and growth expectations, not central bank policy. The chart below shows the US Inflation rate alongside the yield on the 10 Year Treasury. As you can see, there is a strong relationship between the two.

There is a theory in economics that inflation should be negatively correlated to the unemployment rate in an economy. The logic is that as the unemployment rate declines, there are fewer workers available for hire, and companies must increase wages to attract new employees from a smaller supply of available workers. These increased wages put pressure on profits and force companies to increase prices, leading to inflation. While far from an infallible rule of economics, this phenomenon has been observed through a variety of different periods in history.

With the US unemployment rate approaching its lowest level since the turn of the century (which itself was the lowest level since May of 1969), the potential for rising wages and input costs to begin putting upward pressure on inflation has increased. When we combine this possibility with the fact that interest rates have been moving steadily lower for over 35 years (see chart from above), we believe it will be incredibly important to watch inflation expectations moving forward. Since long term trends tend to break suddenly rather than gradually, a meaningful upward shift in inflation expectations could impact interest rates and cause disruption in the market.

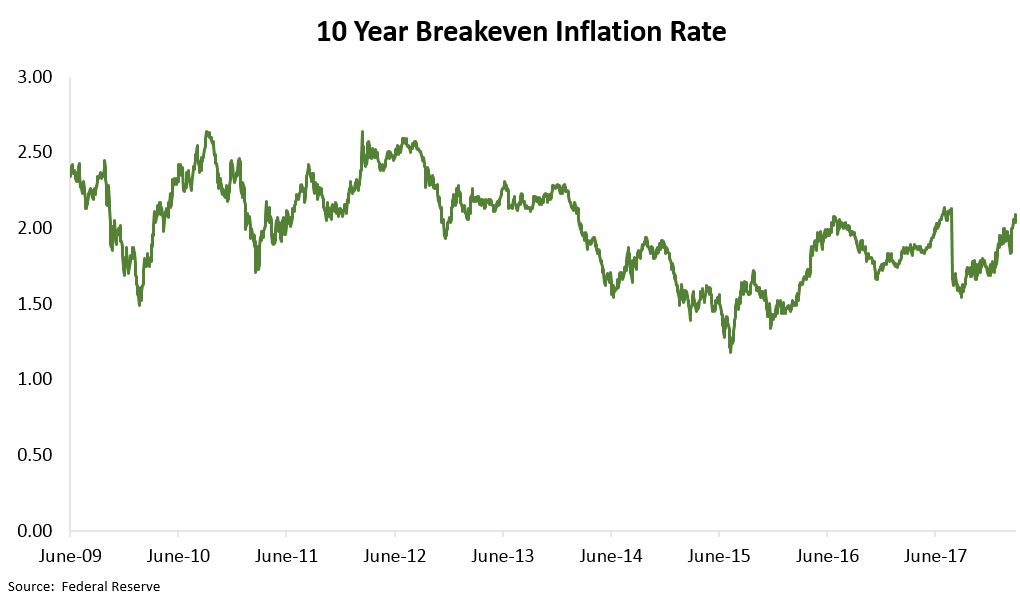

Building upon the notion that portfolios tracking consensus expectations do not outperform, the below chart shows how inflation expectations have evolved since we emerged from the financial crisis.

The 10 Year breakeven Inflation Rate is calculated by subtracting the yield on 10 Year Inflation Protected Treasuries from the yield on 10 Year Treasury Bonds and is used as a proxy for the market’s expectation of inflation over that time period. Thus, we can gather from the chart that inflation expectations have remained quite subdued over the past ten years or so. We saw a slight increase recently, but far from meaningful given expectations are still very close to where they were back in 2016. The key takeaway from this chart is that markets are still not convinced that inflation, and therefore long term interest rates, will push significantly higher over the next few years. We at Valley National are not “convinced” either, but we do believe that there exists a distinct possibility that inflation expectations are adjusted upward as economic growth continues to improve and unemployment continues to decline. Shielding a portfolio from this risk involves reducing interest rate sensitivity by shifting towards short term bonds. We view this as relatively inexpensive “insurance”, since it does not require investors to sacrifice a significant amount of income given that bond yields are already at historic lows. If you have any questions about specific strategies for your portfolio, please contact your financial advisor.

For your convenience, you can now securely pay your tax preparation bill online! Our team continues to focus on the ease of our clients’ experience through secure and simple options to do business with us. It is as easy as 1, 2, 3 to view your invoice and pay it with a credit card or direct from a bank account via QuickBooks. Our website has a quick reference guide so you know what to expect: http://www.valleynationalgroup.com/webpay

For your convenience, you can now securely pay your tax preparation bill online! Our team continues to focus on the ease of our clients’ experience through secure and simple options to do business with us. It is as easy as 1, 2, 3 to view your invoice and pay it with a credit card or direct from a bank account via QuickBooks. Our website has a quick reference guide so you know what to expect: http://www.valleynationalgroup.com/webpay