The show airs on WDIY Wednesday evenings, from 6-7 p.m. The show is hosted by Valley National’s Laurie Siebert CPA, CFP®, AEP®. This week Laurie will discuss:

“A review of tax season take-aways – AGAIN.”

Laurie will take your calls on this or other topics. This show will be broadcast at the regular time WDIY is broadcast on FM 88.1 for reception in most of the Lehigh Valley; and, it is broadcast on FM 93.9 in the Easton and Phillipsburg area– or listen to it online from anywhere on the internet. For more information, including how to listen to the show online, check the show’s website www.yourfinancialchoices.com and visit www.wdiy.org.

by Connor Darrell, Head of Investments Both large cap stocks and bonds ended the week marginally lower, but the heightened volatility observed over the past few months seems to have waned for the time being. Internationally, stocks traded largely in line with those in the U.S., although emerging markets stocks had their worst week in quite some time. Emerging markets stocks have faced headwinds from the increasing strength of the U.S. Dollar, which reached a five-month high last week.

US small cap stocks were a bright spot last week, and have been all year. The Russell 2000, which tracks a broad basket of small cap stocks, is up over 6% so far this year, outperforming the S&P 500 by about 4%.

Oil Prices on the Move It is easy to forget that there was a solid four-year stretch from December 2010 to November 2014 where the average retail price of a gallon of gasoline in the US was well over $3. But a confluence of factors (including technological advances that increased US oil production, as well as a concerted effort by members of OPEC to put a squeeze on those same U.S. producers) led to a massive decline in the price of oil beginning in late 2014. From peak to trough, the total price decline was over 70%, and consumers reaped the benefits for a number of years. However, that has changed rather dramatically in the last 12 months, as prices have come roaring back.

The surge in oil prices over the past year has been driven by a variety of influences, including increasing demand driven by strong global economic growth, cooperation between Russia and OPEC, economic collapse in Venezuela, and logistical inefficiencies disrupting the distribution of US shale oil. On top of this, the Trump administration’s decision to withdraw from the Iran nuclear deal and re-impose sanctions could lead to a decline in Iranian production, which would further deepen the supply shortfall.

In the near term, the rise in oil prices has the potential to increase inflation and pose as a headwind to economic growth (albeit not nearly large enough to offset the benefits of recent tax reform). We have discussed in the past that the Fed is watching inflation closely, as it is one the key indicators that helps to dictate monetary policy. However, the Fed is unlikely to be coerced into altering its path of normalization by something as fickle (and potentially temporary) as rising oil prices. It is more likely that the worst side-effect of the recent run up in oil prices will be some pain at the pump during the summer travel season.

Tomorrow is the Volunteer Challenge event, but there is still time to vote for your favorite project (before 6:30 p.m. tonight). Click here to see them all, plus available silent auction items. Click here to go direct to our project page. Thank you for helping us support awareness for the Volunteer Center of the Lehigh Valley.

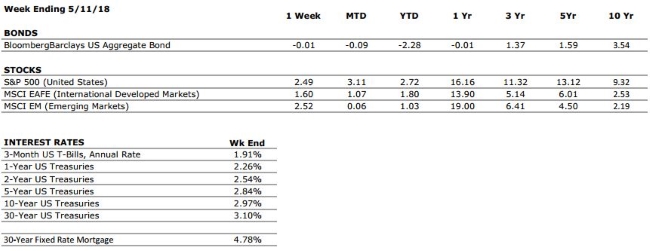

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

US ECONOMIC HEAT MAP

The health of the US economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

CONSUMER SPENDING

A+

Consumer spending is expected to remain healthy as individuals with lower tax rates spend their windfalls.

FED POLICIES

C-

The Federal Reserve increased the Fed Funds Rate by 0.25% in March, and is expected to implement at least 2 more hikes this year. Rising interest rates tend to reduce economic growth potential and can lead to repricing of income producing assets.

BUSINESS PROFITABILITY

A

Q1 Earnings season is almost over, and it has been fantastic. US companies are reporting YoY earnings growth of almost 25%.

EMPLOYMENT

A+

The unemployment rate has dropped below 4% for the first time since 2000. Additionally, there are over 6 million unfilled job openings throughout the economy; close to an all-time record.

INFLATION

B

Inflation is often a sign of “tightening” in the economy, and can be a signal that growth is peaking. The inflation rate remains benign at this time, but we see the potential for an increase moving forward. This metric deserves our attention.

OTHER CONCERNS

INTERNATIONAL RISKS

5

The above ratings assume no international crisis. On a scale of 1 to 10 with 10 being the highest level of crisis, we rate these international risks collectively as a 5. These risks deserve our ongoing attention.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

by Jessica Goedtel, Senior Associate If you are a Pennsylvania resident and are considering leasing a car, you should know that Pennsylvania imposes an additional 3% tax on the lease of motor vehicles, in addition to the state 6% sales tax. This special tax is collected and put into the Public Transportation Assistance (PTA) Fund, and is dedicated to funding mass transportation.

This tax is 3% of the total lease price, and applies to motor vehicles leased for 30 days or more. When deciding on whether to purchase or lease a new vehicle, make sure to factor in this additional cost.

Click here to read more about the PTA Fund and applicable fees and taxes on the PA Dept of Revenue website.

The show airs on WDIY Wednesday evenings, from 6-7 p.m. The show is hosted by Valley National’s Laurie Siebert CPA, CFP®, AEP®. This week Laurie and her guest, Attorney Mark Aurand of Greater Good, LLC, will discuss:

“Accessible legal considerations for small business and nonprofit startups.”

Laurie will take your calls on this or other topics. This show will be broadcast at the regular time WDIY is broadcast on FM 88.1 for reception in most of the Lehigh Valley; and, it is broadcast on FM 93.9 in the Easton and Phillipsburg area– or listen to it online from anywhere on the internet. For more information, including how to listen to the show online, check the show’s website www.yourfinancialchoices.com and visit www.wdiy.org.

by Connor Darrell, Head of Investments

Stocks posted their strongest weekly gain in over 2 months last week, with energy stocks leading the way amid further increases in the price of oil. It certainly won’t be celebrated by those of us traveling for summer vacations over the next couple of months, but oil prices are likely to remain elevated if the Trump Administration is able to reinstate economic sanctions on Iran. International markets also posted gains on the week.

Bonds had a relatively uneventful week, but remain under the microscope of many investors and media outlets as interest rates creep higher. We discuss some of our thoughts on what the market might be overlooking in our update below.

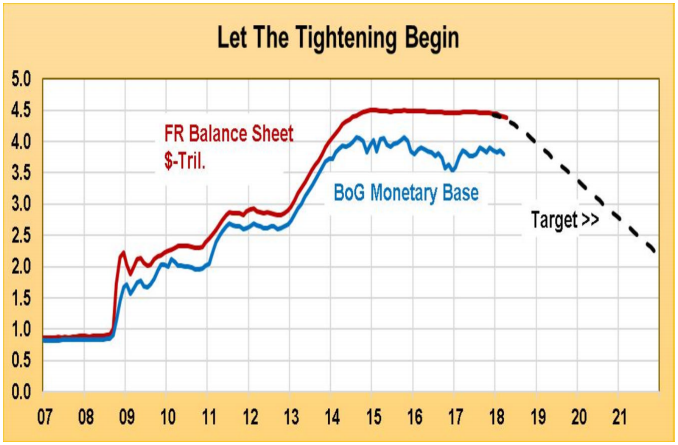

The Bigger Unknown in Monetary Policy “Normalization” Likely due to their direct influence over the interest earned on savings and paid on loans, the Fed’s interest rate decisions seem to get all of the attention when it comes to discussions of monetary policy. However, faced with the unenviable task back in 2008 of combating the deepest recession in a generation, the Fed pulled out all the stops, using every tool in its arsenal to inject life back into the US economy. As a result, in addition to the traditional (and oft discussed) avenue of pulling interest rates down near zero, the Fed also implemented multiple rounds of Quantitative Easing, an unprecedented expansion of Reserve Bank Credit (the Fed Balance Sheet). This was accomplished by purchasing trillions of dollars’ worth of bonds in the open market in order to inject more money into the financial system and increase liquidity in markets. The ultimate purpose of the policy is largely the same as the reduction in interest rates, but it is widely considered to be a much more extreme approach.

Between October of 2008 and December of 2014, the value of the Federal Reserve’s balance sheet swelled from $0.9 trillion to $4.5 trillion (see below chart from Argus Research) as it continued to purchase bonds. Since then, the balance sheet has remained largely untouched, but the Fed has made clear in its communications that this will soon change. The consensus among forecasters is that the Fed will begin the process of shrinking its balance sheet later this year by allowing maturing bonds to roll off and ceasing its reinvestment of coupon payments, to the tune of about $50 billion per month.

Like all markets, the bond market is driven primarily by supply and demand, and with the Fed reversing its policies, the underlying balance of supply and demand will undoubtedly be altered. What would this mean exactly? The ultimate results are very difficult to predict. If the Fed is able to effectively telegraph its moves (as it intends), then markets may be able to adjust gradually with no major impacts. But if the balance shifts more than anticipated, then a major dislocation could take place. Under such a scenario, the laws of supply and demand would dictate that the oversupply of bonds on the market would drive prices down, and yields up.

Source: Argus Research

That short term rates will increase from here is highly likely and largely assumed by most investors, so in our view, the potential impact of the Fed’s balance sheet unwind, which would occur in addition to the trends already in place, is the bigger “unknown” as we move away from the accommodative monetary policies of the last decade. Given its current size, it may be appropriate to say that we consider the Fed’s balance sheet to be the “elephant” in the room.

by Connor Darrell, Head of Investments Both stock and bond markets trended downward last week, until Friday’s jobs report sparked a stock market rally. The Department of Labor reported that employers added 164,000 new jobs in April, and that the unemployment rate currently stands at 3.9%. This was the first unemployment reading below 4% since 2000.

Additionally, there are more than six million unfilled job openings throughout the economy; close to an all-time record. However, despite the continued imbalance in the supply and demand for labor, wage growth has remained slightly below expectations. Wage growth is one of the last pieces of the puzzle, and because of its potential connection to inflation, will be watched closely by the Fed as it steadies its march toward normalization.

A Wacky Earnings Season Active traders often try to take advantage of earnings calls as an opportunity to buy or sell a stock ahead of its earnings report. It’s a risky proposition, and one that we do not recommend in the current environment. Per Factset, 81% of S&P 500 companies have reported Q1 earnings in excess of consensus estimates, and overall earnings growth has been over 24%; the highest rate in seven and a half years. Even so, we have witnessed dozens of companies report earnings beats, only to sell off meaningfully during the following trading session. It seems the market has lofty expectations for further growth, and companies that do not raise their forward guidance to meet those expectations are being punished. As we continue to progress deeper into the economic cycle, the heavy emphasis on forward guidance rather than past results is likely to persist.

According to research from Wells Fargo, earnings growth for Q1 would be closer to 7% in the absence of tax reform, and once we reach 2019, year-over-year comparisons will not benefit from the tax reform boost. Add this reality to the confluence of risks that the market has begun to acknowledge rather than ignore, and it becomes a little bit easier to understand why markets aren’t quite ready to break out the champagne to celebrate a successful earnings season.

As the market continues to trend sideways with higher levels of volatility, asset allocation and diversification become even more important. Periods like these are the reason we diversify in the first place.