As many of our clients already know, Senior Vice President Frank Stettner, CPA, CFP® and his team based in Valley National’s New Jersey office spend time in both our Phillipsburg location and our Bethlehem headquarters. Moving forward they will be scheduling regular weekly hours at both locations for consistency and the convenience of our clients. If you would like to have a meeting at our Phillipsburg location, please schedule in advance with your service team as the office will be closed to walk-in visitors on Tuesdays & Thursdays, and Wednesday mornings. Calls and other correspondence will be automatically re-routed to our Bethlehem office on those days during office hours.

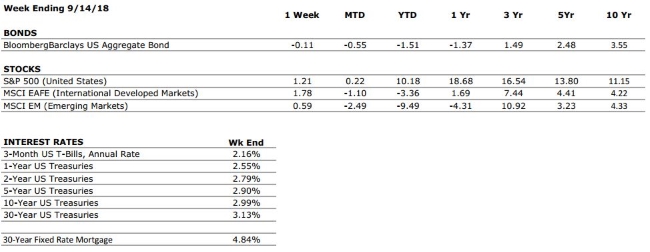

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

US ECONOMIC HEAT MAP

The health of the US economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

CONSUMER SPENDING

A+

Consumer spending is expected to remain healthy as individuals with lower tax rates spend their windfalls.

FED POLICIES

C-

The Federal Reserve held pat following its most recent meeting, but it remains probable that two more rate hikes will be implemented before year-end. Rising interest rates tend to reduce economic growth potential and can lead to repricing of income producing assets.

BUSINESS PROFITABILITY

A

Factset is reporting a blended earnings growth rate of 20% YoY for the 2nd quarter of 2018. Tax reform has played a major role, but the strength of the US consumer is boosting corporate profits as well. 80% of US companies have reported positive EPS surprises (meaning actual earnings were higher than forecasts).

EMPLOYMENT

A+

The US economy added 201,000 new jobs in August and the unemployment rate remained below 4%. The job market remains very healthy.

INFLATION

B

Inflation is often a sign of “tightening” in the economy, and can be a signal that growth is peaking. The inflation rate remains benign at this time, but we see the potential for an increase moving forward. This metric deserves our attention.

OTHER CONCERNS

INTERNATIONAL RISKS

5

The above ratings assume no international crisis. On a scale of 1 to 10 with 10 being the highest level of crisis, we rate these international risks collectively as a 5. These risks deserve our ongoing attention.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Starting on September 21, 2018 the Federal Trade Commission (FTC) will be putting a new credit file protection layers in place that will allow consumers to contact any of the three major credit reporting agencies and request a freeze on their credit files free or charge.

The Economic Growth, Regulatory Relief, and Consumer Protection Act stipulates that the reporting agencies – Equifax, Experian, and TransUnion – have until the next business day to put the requested freeze in place. Consumers can also request to lift that freeze at any time and the agencies will have to comply within an hour.

To fully freeze your credit, you must do so with all three credit reporting agencies. When freezing your credit, you will create a pin or passcode. Should you unfreeze your credit report, you will need that pin or passcode to prove your identity.

by Connor Darrell, Head of Investments Equity markets around the globe managed to climb higher last week as they recovered from a difficult start to the month. The constant strategic pivoting in the trade negotiations between the U.S. and its global trading partners (particularly China) has been the primary catalyst for markets over the course of 2018, and we expect this to remain the case at least until the mid-term elections in November. For better or for worse, polling data may begin to influence the aggressiveness of President Trump’s negotiating tactics as he strives to rally voters and keep the Republican majority in the legislative branch. In the meantime, investors will need to keep focusing on fundamentals and accept that daily headlines may foster a particularly “noisy” few weeks.

August inflation data indicated that prices rose 2.7% year over year, marking the first month in 2018 where the rate of inflation cooled. The Federal Reserve’s next policy meeting is next week, and markets are expecting another 0.25% interest rate hike.

Monetary Policy Primer With the Federal Reserve meeting again next week, we thought it might be a useful exercise to discuss the basics of monetary policy and the role of the central bank in monitoring/influencing the economy.

As the U.S. economy emerged from the depths of the financial crisis, the Federal Reserve implemented multiple rounds of an aggressive monetary policy initiative known as quantitative easing (QE). At its core, QE involves actively purchasing bonds on the open market while simultaneously lowering the short-term interest rate in the economy. Both actions work together to keep interest rates on all maturities artificially low. The theory is that lower interest rates make it more palatable for businesses to borrow money and invest in growth opportunities, stimulating the economy. Ten years later, rates are still very low in historical terms, and the U.S. stock market has benefitted from the decade of “easy money” policies. However, as the economy heats up and evidence mounts that it can stand on its own footing, the Federal Reserve must now unwind its actions and begin pushing the economy to a more “normal” state.

The influence of the central bank has certainly expanded during the 21st century, and QE was in many ways an experimental policy. Never in history had central banks implemented such a bold and large-scale policy initiative aimed at actively combating a recession. So far, with the U.S. economy looking quite healthy, it appears to have been a success. But it should be noted that we have not yet seen this play out in its entirety, and only time will tell whether the policy was optimally implemented. The one thing that seems certain however, is that it helped to support the U.S. stock market over the past 10 years. Following the 2008 recession, the U.S. stock market took only four years to recover and reach its previous highs. This is in stark contrast to the recovery following the Great Depression, when it took more than 10 years, plus the organic stimulus of a world war, to finally reach the previous market peak.

The show airs on WDIY Wednesday evenings, from 6-7 p.m. The show is hosted by Valley National’s Laurie Siebert CPA, CFP®, AEP®. This week Laurie will discuss a “Understanding what you can do with your retirement accounts.”

Laurie will take your calls on this or other topics at 610-758-8810 during the live show, or via yourfinancialchoices.com. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.