Our Senior Vice President Laurie Siebert, CPA, CFP®, AEP® will present on a panel about financial literacy at the Lehigh Valley Women’s Summit on June 5 at Cedar Crest College. READ MORE about the session and the full-day conference at lehighvalleywomen.com

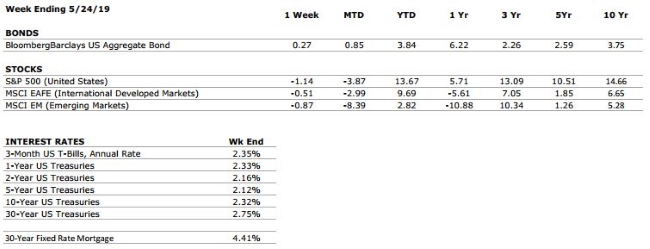

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

US ECONOMIC HEAT MAP

The health of the US economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

CONSUMER SPENDING

A

Our consumer spending grade remains an A. Surveys of US consumers continue to indicate that the consumer is in a strong position, and recent retail sales figures surprised to the upside.

FED POLICIES

C+

Following its March meeting, the Federal Reserve signaled to markets that it may not hike interest rates during 2019, and plans to halt its balance sheet reductions. The Fed’s future actions will remain data dependent, but the contractionary policies that have dominated the last two years appear to be on pause.

BUSINESS PROFITABILITY

B-

Corporate earnings remain strong, but we anticipate earnings growth will taper off in 2019. According toFacset, the expected earnings growth rate for S&P 500 companies during 2019 is around 4%. This is below the long-term average for the current cycle.

EMPLOYMENT

A

The US economy added 263,000 new jobs in April, helping to push the unemployment rate to its lowest level in over 50 years. We have now observed 100 consecutive months of job growth in the United States.

INFLATION

B

Inflation is often a sign of “tightening” in the economy, and can be a signal that growth is peaking. The inflation rate remains benign at this time, but we see the potential for an increase moving forward. This metric deserves our attention.

OTHER CONCERNS

INTERNATIONAL RISKS

7

We have raised our international risks rating to a 7 as a result of rising tensions between the US and Iran, as well as the recent decision by the Trump administration to impose a sales ban on Chinese tech company Huawei. The ban is representative of the risks associated with the growing technology rivalry between the US and China.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Executive Compensation Series – Deferred Compensation Our ExecutiveEdge financial advisors, Rod Young and Jackie Cornelius, discuss Deferred Compensation plans. What you need to know and considerations that are important when deciding on participation. WATCH NOW

by Connor Darrell CFA, Assistant Vice President – Head of Investments

Geopolitical Update: China & Iran Represent Risks We have raised our “International Risks” rating to a 7 from a 5 following recent developments in the Middle East and escalating tensions between the United States and China. We continue to stress that geopolitical events tend to have a smaller impact on markets than fundamental economic factors such as GDP, corporate earnings, and consumer confidence, but believe that recent news flow warrants investors’ close attention.

Earlier

this month, the Trump administration ordered the deployment of significant

military assets to the Persian Gulf, citing intelligence that suggested a

rising probability of Iranian attacks on U.S. interests in the region. The

Iranian economy is under significant pressure as a result of U.S. sanctions,

and there appears to be growing concern within the Iranian government that

Donald Trump will be re-elected in 2020. We have already seen multiple

instances over the past few weeks where Saudi oil assets were sabotaged, and

the general consensus in the intelligence community is that these attacks were

carried out by Yemeni rebels on behalf of Iran. U.S.-Iranian relations are at

their weakest level in years, with Secretary of State Mike Pompeo and Iranian

Foreign Minister Mohammad Javad Zarif never having directly spoken to one

another. The lack of a direct channel of communications between the two chief

diplomats underscores a growing concern that any potential confrontation may be

blown out of proportion and escalate quickly. Any meaningful escalation of

tensions in the region would have the potential to de-stabilize oil prices (20%

of the world’s oil travels through the Strait of Hormuz on its way to end

markets) and further strain the United States’ relationship with China.

The

trade negotiations between the U.S. and China have been thoroughly explored in

virtually all media outlets, as well as in previous iterations of The Weekly

Commentary, but there is another dimension to the discussions which extends

beyond trade deficits and trade surpluses; the race to 5G. It has become

increasingly apparent that the United States government views the race to

establishing and dominating the world’s first 5G (fifth generation) cellular

network technology grid as a matter of national security. First adopters of 5G

technology are expected to sustain a meaningful long-term competitive

advantage, and China is heavily focused on pushing to challenge the United

States as the dominant force in the evolution of the world wide web. China’s

approach to controlling information on the internet is vastly different from

the openness championed by traditional American values, and in many ways, the

race to 5G represents a philosophical battleground over the flow of information;

one that has continued to escalate in recent weeks.

Shortly

after the most recent round of trade discussions fell through, President Trump

announced a ban on Chinese smartphone manufacturer Huawei. The ban blocks U.S.

companies from doing business with Huawei, and essentially prevents it from

accessing key inputs to its manufacturing process (which are produced by

American companies). We see this decision as a clear and meaningful step to

explicitly hamper China’s advancement in 5G technology and keep U.S. companies

on a level playing field (Chinese companies receive direct support from the

Communist-led government).

From an investor

perspective, a meaningful disruption to the supply chain of technology

equipment or additional bans would have the potential to cause volatility in

equity markets as companies’ revenue streams are impacted. Even if a trade deal

is reached within the next several months, the complexities of the

technological rivalry between the two countries is likely to persist and will

represent potential challenges for global companies which may be caught in the

crosshairs of further policy action. Furthermore, a prolonged period where

tariffs are imposed on Chinese goods would likely have a negative impact on

economic growth. Recent research published by the New York Fed estimated that

the newest round of tariffs could cost the average American household $831 per

year. The focus on China and trade has the potential to draw the market’s focus

further away from fundamentals and toward the unpredictability of the

president’s Twitter feed. Such an environment will be very difficult to

navigate for market timers and short-term traders. In our view, the best defense for this type

of uncertainty is broad diversification and discipline. We will continue to

utilize The Weekly Commentary to share our thoughts on new developments as they

unfold.

How to Deal with Volatility Over the past 18 months or so, a variety of surfacing risks have taken their shot at derailing the bull market. Chief among them have been the deteriorating U.S./China trade relations, weakening (but not stalling) global economic growth, and of course the ever-present abundance of geopolitical tensions around the world. The market’s reaction to the setback in U.S./China trade negotiations last week led to a rough day of trading on Monday, and many investors were left wondering whether the markets would crater as they did back in 2018. But the fact of the matter is that for equity investors, volatility is to be expected. However, the very presence of volatility is the primary reason that equity returns tend to be higher than other asset classes over the long-term (we can think of returns in this context as our compensation for enduring the higher levels of risk and the stress that can come along with it). So how can we as investors better manage the emotional roller coaster that can accompany this volatility? We offer some thoughts on the subject below:

Understand your situation and your goals: As with most aspects of personal finance, it is important to reflect upon your current stage of life. For example, if your distance from retirement can be measured in decades, it is reasonable (and likely prudent) to take no action, and perhaps even look at market weakness as a buying opportunity. On the other hand, investors who are near retirement or perhaps just recently retired are likely to look at market volatility in a drastically different light. For these investors, it is important to also consider the size of your nest egg and your specific income needs relative to your portfolio. A conversation with your financial advisor (and perhaps an update to your financial plan) can go a long way in helping you determine what the best course of action might be if you are becoming concerned with the volatility in your portfolio

Maintain a Bucket of Liquid Cash Reserves When building a financial plan, we typically recommend maintaining at least 6-12 months’ worth of spending needs (this number might be lower for accumulators) in low-risk, interest-bearing assets, and refer to these assets as a liquid reserve. These reserves can serve as a source of income during periods of market weakness and can prevent you from needing to draw down your other assets after they have decreased in value. Given the still low rates offered by most checking and savings accounts, money market funds, CDs, and short-term high-quality bonds, these tend to be the best options for investors today. However, it is important to remember that these types of assets expose you to the potential opportunity costs associated with not holding investments with higher expected rates of return over the long haul.

Remind Yourself of the Long-Term Wealth Generating Power of Markets Perhaps the most important thing for long-term investors (which most of us are) to remember when volatility strikes is that the financial markets have a remarkable track record of generating and compounding wealth throughout history. Our Vice President and Financial Advisor Joe Goldfeder, CFP® recently recorded a great video on this very subject. In it, Joe shares some powerful statistics about long-term investing and the resilience of markets, and also discusses some of the above concepts in a little more detail. CLICK HERE TO WATCH

In observance of Memorial Day, our offices will be closed on Monday, May 27. All of us at Valley National wish you a safe weekend as we pause to remember those who have made the ultimate sacrifice for our freedom.

Investing: The Value of a Long-Term Approach Vice President Joseph Goldfeder, CFP® addresses volatility and recovery in the markets, and some steps you might take to understand and prepare for the future of your portfolio. WATCH NOW