Our team is honored to be the recipient of the People’s Choice Award from the Volunteer Center’s 10th Volunteer Challenge with our partners at Paxinosa Elementary and Mission Plant Company. Our Just Press Pause project for teachers was the favorite of attendees at last night’s celebration.

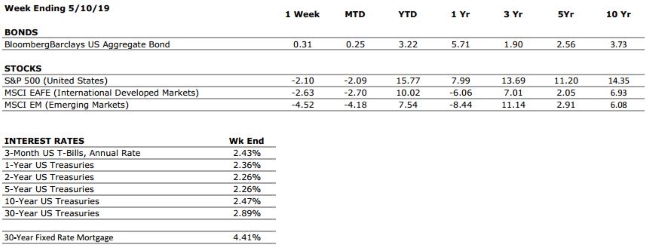

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

US ECONOMIC HEAT MAP

The health of the US economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

CONSUMER SPENDING

A

Our consumer spending grade remains an A. Surveys of US consumers continue to indicate that the consumer is in a strong position, and recent retail sales figures surprised to the upside.

FED POLICIES

C+

Following its March meeting, the Federal Reserve signaled to markets that it may not hike interest rates during 2019, and plans to halt its balance sheet reductions. The Fed’s future actions will remain data dependent, but the contractionary policies that have dominated the last two years appear to be on pause.

BUSINESS PROFITABILITY

B-

Corporate earnings remain strong, but we anticipate earnings growth will taper off in 2019. According toFacset, the expected earnings growth rate for S&P 500 companies during 2019 is around 4%. This is below the long-term average for the current cycle.

EMPLOYMENT

A

The US economy added 263,000 new jobs in April, helping to push the unemployment rate to its lowest level in over 50 years. We have now observed 100 consecutive months of job growth in the United States.

INFLATION

B

Inflation is often a sign of “tightening” in the economy, and can be a signal that growth is peaking. The inflation rate remains benign at this time, but we see the potential for an increase moving forward. This metric deserves our attention.

OTHER CONCERNS

INTERNATIONAL RISKS

5

The above ratings assume no international crisis. The ongoing trade negotiations between the US and China and the escalating geopolitical tensions in the middle east both present potential areas of concern. But on a scale of 1 to 10 with 10 being the highest level of crisis, we rate these international risks collectively as a 5 at this time.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

by Connor Darrell CFA, Assistant Vice President – Head of Investments Geopolitics dominated headlines throughout the week, as a sudden re-escalation of trade tensions between the U.S. and China forced global equities into one of their first weeks of solid losses all year. The S&P 500 shed a little over 2% of its value through week’s end, with international markets losing a bit more.

Despite appearing to be close to a final deal which would have enabled business leaders and markets to put much of the trade-related uncertainty behind them, Chinese officials reportedly backed away from multiple concessions they had made during prior negotiations. Chief among them were issues related to Chinese government subsidies, which have historically served to tip the competitive balance in favor of Chinese companies. In response, President Trump drew a hard line and raised tariffs on $200 billion worth of Chinese exports, effective immediately.

Elsewhere, diplomatic relations between

the U.S. and Iran deteriorated to their lowest level in years after a U.S.

aircraft carrier was deployed into the Persian Gulf in response to indications

of potential planned attacks on U.S. interests in the region. Oil prices have

inched higher as a result of the rising tensions in the region.

Amid all of this geopolitical “noise,” it

is important to remember that long-term growth in equity markets is driven by

earnings, which are far more connected to the strength of the consumer and the

economy than to the patterns of global trade. Both the economy and the consumer

remain on firm footing at this point in time.

Chinese Economy a Double-Edged Sword It seems that at present, any new information regarding China’s economy may be a double-edged sword. During the later end of 2018, the data coming out of China seemed to suggest that its economy was weakening, and there was speculation that the weakening economic momentum was at least in part due to U.S. trade policy. The prospects of a weakening Chinese economy were among the list of factors blamed for the market volatility during that time, just as the subsequent inflection point was considered one of the keys to the 2019 rally. The problem for markets is that China’s improving economy may have emboldened its leaders during last week’s trade negotiations, perhaps setting the stage for the setback in negotiations.

Investors are now faced with a difficult

proposition regarding China. On one hand, the improving Chinese economy is good

for global markets, and bodes well for extending the global economic cycle. On

the other hand, it provides Chinese negotiators with more leverage during trade

negotiations, which makes it much harder for US officials to reach a

satisfactory deal. As we have seen,

markets are very sensitive to meaningful shifts in the expected probability of

a final deal being inked, but since market performance tends to mirror the

health of the global economy and not trade patterns, long-term investors should

place more emphasis on the economic data when positioning portfolios.

The show airs on WDIY Wednesday evenings,

from 6-7 p.m. The show is hosted by Valley National’s Laurie Siebert CPA, CFP®,

AEP®.

Laurie

will not be live on the air this Wednesday, May 15. Tune into WDIY for a

pre-recorded Your Financial Choices episode. Questions submitted via the

website will be addressed during the next live show on May 22, when the topic

will be Cash Flow Management.