COVID SCAMS Unfortunately, fraud related to the coronavirus pandemic is part of

the new normal as many people are overwhelmed, stressed, scared and in need. We

have collected some links to help you share to recognize and report these

criminals.

Tune in Wednesday for another new “Your

Financial Choices” show on WDIY. Laurie will be recording

the show Tuesday to air at the normal time, Wednesday, 6-7 p.m. She will answer

questions that have been submitted via yourfinancialchoices.com and discuss: More on

the CARES Act.

Live episodes of “Your Financial Choices” are

postponed until further notice as Laurie and her guests are working from home

in response to guidance around the COVID-19 pandemic. WDIY will continue to

broadcast prerecorded local shows as well as available NPR programming. Please

continue to support local radio!

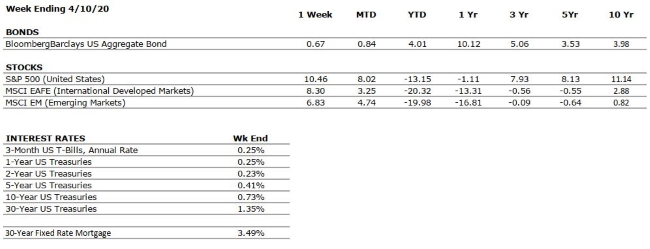

by Connor Darrell CFA, Assistant Vice President – Head of Investments In what might be a perfect example of why market timing is such a fallible investment strategy, the U.S. equity market generated its strongest weekly gain since 1974 last week. Investor sentiment has improved throughout much of the past couple of weeks as new data has started to show signs that the number of new cases of COVID-19 may be peaking. In the United States, the number of deaths projected by epidemiological models declined sharply last week as social distancing efforts have produced positive results.

Also

aiding the market’s recovery has been the unprecedentedly robust response from

the Federal Reserve, which announced additional measures last week to expand

lending programs in an effort to provide a backstop for businesses, households,

and municipalities impacted by the pandemic. As part of these new measures, the

Fed announced it would support new debt issuance for corporations which have

recently lost their investment grade credit ratings. Such companies, often

referred to as “fallen angels” face significant increases in borrowing costs

just as the need for cash has increased. Fed Chair Jerome Powell spoke on

Thursday in conjunction with the announcement of the new policy initiatives and

reiterated that there will be no limit to the aid that the Fed can provide

markets, other than where it is prohibited by law.

Europe Struggling to Pass Fiscal Stimulus All of the above continues to support much of what we have been communicating in recent weeks, which is that the economic impacts of the pandemic will be immense, but that the impact of swift and robust policy responses should not be discounted. These responses, however, are an important part of the puzzle when it comes to determining what the path forward will look like once we reach the other side. A coordinated and effective policy response will be essential for keeping the economy positioned for a recovery, and this creates potential problems for governments around the world which may still be struggling to find the consensus needed to legislate such a response. In Europe for example, economic crises tend to cause an elevated level of friction between the region’s more robust economies and those that are further behind in their development. Thus far, despite what economists around the globe identify as a dire situation, EU leaders have not been able to come to an agreement on a fiscal response to the crisis as a result of this friction. If the governments of the European Union are unable to reach such an agreement, the economic impacts of the virus could be substantially larger and longer lasting than what is seen here in the United States. And while we believe that the magnitude of the situation will eventually push leaders to find a solution, the ongoing discussions among EU leaders should be monitored closely.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

VERY NEGATIVE

The consumer has been the bedrock of the US economy through much of the current expansion, and remains in a strong position. However, we have further reduced our grade to VERY NEGATIVE as a result of the unprecedented social distancing and quarantining efforts currently being employed to fight the spread of COVID-19.

CORPORATE EARNINGS

VERY NEGATIVE

Coming into the year, analysts were expecting mid to single digit earnings growth, but the spread of COVID-19 is likely to have a substantial impact on near-term earnings forecasts. However, earnings could bounce back quickly once the pandemic has run its course.

EMPLOYMENT

VERY NEGATIVE

We have downgraded our employment grade another level as we expect the next few weeks will reveal significant job losses due to the suspension of economic activity in the services industry to combat the spread of COVID-19.

INFLATION

POSITIVE

Inflation is often a sign of “tightening” in the economy, and can be a signal that growth is peaking. The deflationary environment created by COVID-19 should provide additional room for robust stimulus from both fiscal and monetary policy initiatives.

FISCAL POLICY

VERY POSITIVE

The CARES Act provides approximately $2.2 trillion of support for businesses and families that are impacted by the economic fallout of the COVID-19 pandemic. This is by far the largest fiscal stimulus package ever passed, and we anticipate the possibility of additional support once we emerge on the other side of the curve.

MONETARY POLICY

VERY POSITIVE

In response to the threat of COVID-19, the Federal Reserve has implemented two emergency rate cuts and has moved its target interest rate back to zero. Additionally, it has announced its intention to conduct further asset purchases to support markets. We believe that the Fed is doing all it can to support the economy and markets.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

VERY NEGATIVE

With COVID-19 being declared a global pandemic, our geopolitical risks rating is VERY NEGATIVE.However, we think it is important for investors to disentangle the public health concerns over the near-term from the expectations for markets over the long-term. The pandemic remains a near-term issue at this time.

ECONOMIC RISKS

VERY NEGATIVE

The economic impacts of the COVID-19 pandemic are likely to be substantial. However, we believe that the eventual economic recovery (which will be aided by historically large economic stimulus) will occur more swiftly than from previous economic shocks.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

News and information related to COVID-19

is being released and updated very rapidly. Our team has collected just a few

of the latest links that we think may be most valuable to our clients.

New Guidance about COVID-19 Economic Impact Payments for Social Security and Supplemental Security Income (SSI) Beneficiaries from Social Security Commissioner Andrew Saul – ssa.gov/news/press/releases/

Tune in Wednesday, April 15 for a new “Your Financial Choices” show on WDIY. Laurie will be recording the show Tuesday to air at the normal time, Wednesday, 6-7 p.m. She will answer questions that have been submitted via yourfinancialchoices.com and discuss the CARES Act and delayed filings.

Live episodes of “Your Financial Choices” are

postponed until further notice as Laurie and her guests are working from home

in response to guidance around the COVID-19 pandemic. WDIY will continue to

broadcast prerecorded local shows as well as available NPR programming. Please

continue to support local radio!

The show normally airs on WDIY Wednesday evenings, from 6-7 p.m. The show is hosted by Valley National’s Laurie Siebert CPA, CFP®, AEP®. Laurie takes questions at 610-758-8810 during the live show, and address those submitted online at yourfinancialchoices.com.

“Times of transition are strenuous, but I love them. They are an opportunity to purge, rethink priorities, and be intentional about new habits. We can make our new normal any way we want.” – Kristin Armstrong

Sharing Community Needs The Volunteer Center of the Lehigh Valley has created a page on their website with links to finding volunteer opportunities; a listing of direct needs for local nonprofits and helpful links for resources for COVID-19.

If you can help or you know of a nonprofit in need of help, please visit the page and share the link. volunteerlv.org/covid-19

Equities: We cautioned in our Q4 commentary that equity market returns last year were achieved on the back of stagnant earnings growth, and that “a tempering of return expectations” may be warranted moving into 2020. Of course, nobody could have predicted that just weeks later, the world would be in the midst of a global pandemic and that financial markets would have been thrown into a state of complete disarray. The rapidity with which markets retreated from their highs in response to the global spread of COVID-19 was historic, and largely representative of the massive shock that the disease poses to the global economy. Stocks across virtually every sector lost significant value, and there was largely nowhere for investors to hide. Volatility in the US equity market (as measured by the VIX) reached its highest level in history, surpassing the previous record set in November of 2008. Over the long-term, equity market returns are driven by fundamentals, but the term “fundamentals” was completely tossed aside during the first quarter as the extraordinary level of uncertainty opened the doors for panic to become the main determinant of market prices. Unfortunately, until the world is able to emerge on the other side of “the curve”, a clearer understanding of market fundamentals will not be achievable, and volatility will continue to be the norm. However, it is vital that investors continue to remind themselves that the economic impacts of COVID-19 will be transitory.

Bonds: What made the first quarter exponentially more painful for investors was that bonds (traditionally viewed as much safer than equities) were not spared from the selloff. In fact, it could be argued that when compared to historical norms, the volatility seen in the bond market was even worse. As fear and panic took hold, buyers disappeared from bond markets just as they did in equity markets, leading to a complete evaporation of liquidity and significant markdowns in bond prices. The Federal Reserve responded swiftly by committing a significant amount of capital as a buyer of last resort, and this helped to stabilize pricing toward the end of the quarter, but much of the damage was already done. Moving forward, default rates on lower quality bonds are likely to accelerate meaningfully. However, because the massive selloff occurred across bonds of all credit quality, many investors in higher quality bonds will likely recoup their losses as their bonds eventually mature and return principal.

Outlook: It goes without saying that the equity bull market finally came to an end in the first quarter, and it is likely safe to say that the second quarter of 2020 will represent the beginning of the next economic cycle. The transition from one cycle to another is always a challenging time, but we believe there are a couple of key factors that should help to keep investor fears at bay. First, both the Federal Reserve and the US Government are responding to the crisis with full force. We have no way of knowing when life will begin returning to normal and when we will be able to shift our focus to revitalizing the economy. But when that day arrives, the impact of such massive economic policy initiatives should not be discounted. The second factor that should help to preserve some level of optimism is the health of the US financial system. Many investors are still scarred by the 2008 financial crisis, but while the banking system became the epicenter of the carnage in 2008, it is likely to be an essential part of the solution today. In order for us to successfully navigate the economic challenges that lie ahead, it will be vital for the financial system to continue operating at full capacity, extending lines of credit to otherwise sound businesses which have been negatively impacted by the temporary shutdown of the global economy. The good news is that due to the stringent regulations put in place following the global financial crisis, banks come into this situation better capitalized than at any point in history, and are well positioned to do their part.

VIDEO: Q1 2020 Market Commentary Connor Darrell CFA, Head of Investments offers his perspective on the first quarter of 2020. Connor is working remotely at his home as is our entire TeamVNFA. WATCH NOW

by Connor Darrell CFA, Assistant Vice President – Head of Investments Last week brought an official end to the worst quarter for equities since the 2008 financial crisis, as the global spread of COVID-19 brought many areas of the global economy to a virtual standstill. In our latest quarterly commentary, we provide a brief summary of what became a quarter to forget, as well as an update on why there are still some key factors that should give investors reason for cautious optimism.

A Note on Our Economic Heat Map As our economic “Heat Map” has been steadily revised lower over the past few weeks, we wanted to take a quick moment to remind readers that the Heat Map is not intended to be used as a market timing mechanism. Our team tracks a variety of economic data and uses it to guide our ratings for the Heat Map. Those ratings are intended to provide a “point in time” assessment of current economic conditions and help to assess where the strengths and weaknesses lie. Of course, the present state of the global economy is drastically different than it was just three months ago, and that is the reality behind the recent reductions to our Heat Map rankings. At present, there is an incredible amount of uncertainty regarding the depth and duration of the economic impacts of the COVID-19 pandemic. Our key takeaways from the current rankings of our Heat Map are as follows:

The global economy is under immense pressure as a

result of the quarantining efforts being put in place around the globe. In the

near-term, we are likely to continue to see historically poor economic data. However,

the long-term impacts should be reduced by the incredible amount of fiscal and

monetary stimulus being pumped into the economy.