Team VNFA is at 95% of our fundraising goal in the Community Bike Works Spin-a-Thon 2020. This virtual event has us spinning, running, walking, swimming, and tallying up our miles in celebration of Community Bike Works’ 25 years of their Earn a Bike program. Learn more about this organization and share it to support our team’s campaign. CLICK HERE

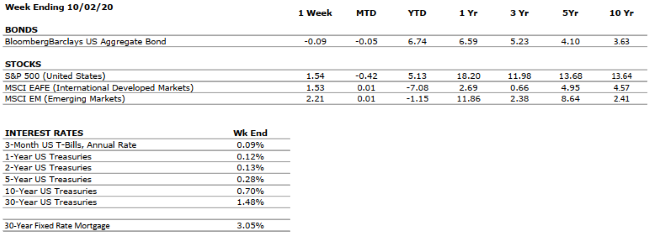

Equities Global equities showed well in Q3, as all three major U.S. indices, International, and Emerging Markets provided positive returns in the mid-to-high single digits. However, equities were ubiquitously down in September, led by the tech-heavy Nasdaq 100 Index. After bidding up technology companies – who, in many cases, have benefitted from 2020’s societal changes – since March’s lows, investors reevaluated if such companies’ positive fundamental outlooks had been over-reflected in their stock prices. Nevertheless, the Dow Jones, S&P 500 and Nasdaq all remain in the green year-to-date, as market participants shun the paltry yields available in fixed income and conclude that their best bets for satisfactory long-term returns reside in the equity markets. In light of the volatility that pervaded Q3’s close, I am reminded of the following words from John Pierpoint (J.P.) Morgan, the grandfather of what is now the largest bank in the world, when he was asked over 100 years ago what the stock market is going to do. “It will fluctuate”, he foretold.

Fixed Income Interest rates remain historically low, as the 10-year treasury yield hovers around 0.70%. Interest rates are representative of investors’ opportunity cost; with rates as low as they are, there is incentive to pay higher prices for equities, as discussed above, because the investor forgoes little by passing on fixed income. The Federal Reserve has communicated that rates are likely to stay low until 2023, meaning that market participants can incorporate minimal opportunity cost into their expectations for the foreseeable future. As Warren Buffett once said, “Interest rates are like gravity on [equity] valuations.” The gravitational pull on the stock market is likely to remain historically weak until inflation sustains at over 2% – something that has not materialized since 2008’s financial crisis – and central banks around the globe are forced to intervene with monetary tightening.

Outlook The marquee event over the next three months is, obviously, the U.S. Presidential Election. While the election has wide-ranging implications, of course, its greatest pertinence with respect to financial markets is that Congress is unlikely to pass additional stimulus until the Executive Chief perch is solidified.

Covid-19 continues to alter everyday life;

however, the U.S. economy has demonstrated some signs of a V-shaped recovery.

Most notably, for example, the unemployment rate has retreated to 7.9%; while

this figure is still considerably above historical averages, it is worth

remembering that in March and April, economists debated for how long

unemployment would persist in the double-digits, specifically, whether the

jobless rate would remain above 10% through 2020. Additionally, certain

consumer trends have emerged stronger than most anyone expected when Covid-19

roiled the markets in March. For instance, several retailers reported all-time

high sales metrics in Q2.

Multiple pharmaceutical companies, including

Pfizer, Moderna, and AstraZeneca, continue their phase 3 vaccine trials. At

this point, it appears probable that at least one vaccine will be granted FDA

approval by year-end, or, at latest, by the end of Q1 2021, and that a method

of inoculation will be available to the American public by the middle of next

year.

While the global economy will not be

unshackled from the pandemic’s recessionary forces in the near-term, risk

assets are likely to remain buoyed by accommodative monetary policy and another

round of fiscal support, the latter of which will likely come to fruition in

early 2021. It is conceivable that, around the same time, a vaccine will be in

production and dissemination, a combination that would certainly appear

facilitative of robust economic and corporate performance. In all cases, the

shrewdest investment strategy is that of adherence to one’s long-term plan and

resistance of short-term maneuvers.

VIDEO: Q3 2020 Market Commentary Our CEO, Matt Petrozelli, introduces Bill

Henderson, Head of Investments who offers a review of the third quarter, and

economic outlook and perspective on long-term investing. WATCH NOW

by William

Henderson, Vice President / Head of Investments Well, 2020 continues to

shock and awe us and the markets. The news of President Trump and Melania

Trump testing positive for COVD-19 certainly was news, and in an already packed

wild news year. A Black Swan event is an event so rare, that the results

cannot be modeled nor predicted. COVID-19 was our 2020 Black Swan event

and thus far the markets have held up and the economy is coming back from an

uncanny recession due to huge fiscal stimulus and massive monetary

stimulus. The rule on Wall Street has always been “Don’t Fight the

Fed,” and we have no plans on doing so. Fed Chairman, Jay Powell, has

promised to do whatever it takes to keep the economy on the road to recovery

and will use all tools in their monetary toolbox to do so. With that said,

we remain positive on the U.S. Economy overall, and especially with a long-term

view. There is a piece of framed artwork on the walls of the Valley

National Financial Advisors office depicting the contributions of James

Pierpont Morgan to the United States Economy in the 1800-1900s. I love

this quote in the piece attributed to J. P. Morgan, “any person who is a

bear on the future of the United States will surely go broke.”

Although

the news concerning President Trump affected Friday’s markets, all three market

averages managed to end the week in positive territory. For the week that ended

October 2, 2020, The Dow Jones Industrial Average was up +1.9%, the S&P 500

Index +1.8% and the NASDAQ +1.5%. Energy continued to be the worst performing

sector while real estate, utilities, consumer discretionary, technology and

financials all held up well. We had spells of good news in the economy.

Unemployment fell by more than forecast, dropping -0.5% to 7.9%. Year-to-date

returns remain mixed with the Dow (3.5%), S&P 500 +3.6% and the NASDAQ

+23.4%.

2020

will be remembered as one of the most difficult and tumultuous years in recent

history for investing. October surprises impact markets and Black Swan

events really impact markets but always over history, markets have recuperated.

There have been four days in in 2020 where the S&P 500 Index fell by more

than 5%: February 24 (-9.3%), March 9 (-5.3%), March 16 (-8.1%) and June 8

(-5.0%) and three days where the S&P 500 Index rose by more than

5%: March 23 (+10.9), April 6 (+8.0%) and June 1 (+5.1%). Just 7 days

in the year gave so much volatility yet on a year-to-date basis the S&P 500

index is still up 3.6% as of October 2, 2020. Our investment thesis at VNFA

remains – choose a clear and balanced investment plan, have a long-term view of

your plan and allow us to monitor and limit your risk.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEGATIVE

GDP declined at an annualized rate of 32.9% in Q2, the fourth-largest fall in the last 100 years. In mirror opposition, Q3 GDP is expected to represent the greatest quarter-over-quarter increase in history, coming in somewhere between 25-35% on an annualized basis.

CORPORATE EARNINGS

VERY NEGATIVE

S&P 500 earnings fell by around 1/3 in Q2, the sharpest year-over-year decline since 2008. However, some companies in certain sectors have reported strong results, such as in Retail and Cloud Computing.

EMPLOYMENT

VERY NEGATIVE

The unemployment rate has declined to 7.9%, from a peak of 14.7% in April. While the rebound is material, the jobless rate remains well above the historical average.

INFLATION

POSITIVE

Core inflation has come in at 1.7% over the last twelve months. The Fed plans to allow inflation to temporarily overshoot its 2% target such that the long-term average is 2%. Inflation has been tame since the Great Financial Crisis, less than 2%.

FISCAL POLICY

VERY POSITIVE

Weekly unemployment benefits are now being disseminated on a state-by-state basis, through applications to a Federal slush fund, and total $300 per week, versus the previous rate of $600 under the now-expired Federal plan.

MONETARY POLICY

VERY POSITIVE

The Federal Reserve has supported asset markets with unprecedented speed and magnitude in response to COVID-19.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

VERY NEGATIVE

The relationship between the US and China, the world’s two largest economies, was already weakened by the trade war but has deteriorated further as a result of COVID-19.

ECONOMIC RISKS

VERY NEGATIVE

The impacts from COVID-19 were as swift and pronounced as any shock in modern times. Robust monetary and fiscal stimulus stabilized the system, however, economic activity remains well- below that in 2019, and uncertainty remains high.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.