In

the Community One

of our Team VNFA Core Values is Live in the Community. We are proud to share just

a couple of recent examples of how our employees are making an impact.

Our

Founder & Chairman Tom Riddle, as part of the ArtsQuest Foundation, helped raise $1,246,326 in gifts and pledges as

of Dec. 31, 2020 in support of Musikfest. READ

MORE

Community Bike Works is featured on the cover of

Bicycling Magazine! Our team, led by the involvement of Joe Goldfeder, Vice

President and Financial Advisor, is pleased to support this organization. We

invite you to learn about their work. READ MORE

The IRS announced

that eligible educators can deduct

unreimbursed expenses for COVID-19 protective items to stop the spread of

COVID-19 in the classroom. READ

MORE

The Department of Education announced

that President Biden extended the student loan payment pause and interest waiver “at least” through

September 30, 2021. READ

MORE

by William

Henderson, Vice President / Head of Investments

Investors shrugged off

economic setbacks such as a weaker than expected jobs report and pushed stocks higher by the end of

the week hitting new records across the board. Additionally, Janet Yellen, the newly installed Treasury Secretary,

pushed for rapid fiscal stimulus while ignoring the potential for inflation. Such dovish

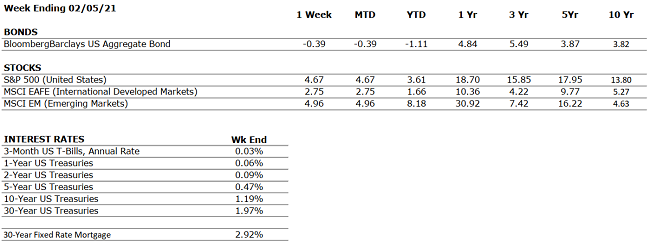

commentary pushed the 10-year U.S. Treasury note to 1.15% by the end of last week. For the week that ended February 5, 2021, the Dow Jones Industrial Average returned +3.9%, the S&P 500 Index +4.7% and the NASDAQ +6.0%. The strong returns from last week moved the averages well into positive territory for the year; with the Dow Jones Industrial Average returning +1.9%, S&P 500 Index +3.6% and the NASDAQ at +7.6%. As noted above, the 10-year U.S. Treasury note moved higher by eight

basis points to 1.15%.

With the modest rise in Treasury

yields, the yield curve, the slope of which gives an idea of future interest rates and economic

activity, is at its steepest since 2017. The steepening yield curve signals comfort by Treasury and Fed that the

economy is healing and expectations of upcoming healthy inflation. While

making the case for President Biden’s $1.9 trillion economic relief package,

Treasury Secretary Yellen noted on CNN February 7 that “too rapid inflation was a risk that needed to be

considered and that policy makers have the tools to deal with that should it

materialize.”

Other than the slightly weaker

January payroll report of only +49,000 new jobs added, there were plenty of

positive economic reports last week. The Institute for Supply Management’s

service survey topped expectations and the new-order and hiring components pointed to stronger growth

ahead and durable-goods orders topped expectation as

well. The economy will get a healthy boost from more stimulus payments, if not from a bipartisan effort than from the Democrats own $1.9

trillion package. The final driving power behind last week’s rally in the

markets was improving Covid-19 news. The weekly number of new cases continued to drop and new vaccines, including one from

Johnson & Johnson, will be on the scene soon.

With some much noise from the

media, investors oftentimes lose sight of the long-term objective which is saving for

retirement or another similar financial goal. In contrast, clear financial goals, a disciplined investment process and a long-term approach is how investors can achieve their objectives.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

U.S. GDP increased at a 4% annualized rate in Q4. For the full-year 2020, the U.S. economy contracted by 3.5%, its worst performance since 1946. GDP is expected to improve meaningfully in 2021 as the American population gets vaccinated.

CORPORATE EARNINGS

NEUTRAL

With ~60% of S&P 500 constituents having reported Q4 earnings, profit growth is coming in at 1.6% year-over-year, well in excess of analyst expectations, which figured that earnings would fall by 7%.

EMPLOYMENT

NEGATIVE

The unemployment rate declined to 6.3% in January from 6.7% in December. Labor weakness remains in sectors such as Leisure and Travel; such sectors stand to benefit as vaccine distribution accelerates.

INFLATION

POSITIVE

The Fed plans to allow inflation to temporarily overshoot its 2% target such that the long-term average is 2%. Inflation has been tame since the Great Financial Crisis, less than 2%.

FISCAL POLICY

POSITIVE

Discussions on President Biden’s a $1.9 trillion stimulus package are ongoing. If the bill passes through Congress, the U.S. economy will have received a total of approximately $4 trillion in stimulus over the trailing twelve months.

MONETARY POLICY

VERY POSITIVE

The Federal Reserve supported asset markets with unprecedented speed and magnitude in response to COVID-19.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

There are few, if any, looming geopolitical risks that could upset the economic recovery.

ECONOMIC RISKS

NEUTRAL

Although economic activity mostly remains below 2019’s levels, improvement has occurred across nearly every measure since the April 2020 nadir. With multiple vaccines in distribution, a second fiscal package in place, and interest rates low, 2021 is positioning to be a strong economic year.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Laurie

and her guest can take your questions live on the air at 610-758-8810, or

address those submitted via yourfinancialchoices.com. Recordings of

past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.