Welcome Luis Sepulveda to Team VNFA! Luis will be working remotely from the Bethlehem office as Financial Technology & Trading Associate. He joins the team with more than 15 years of trading and operations experience. In his new role, Luis will manage investment databases and assist with operational support as part of the VNFA Investment Department. Luis has a B.S. in Business Administration, Finance from Villanova University.

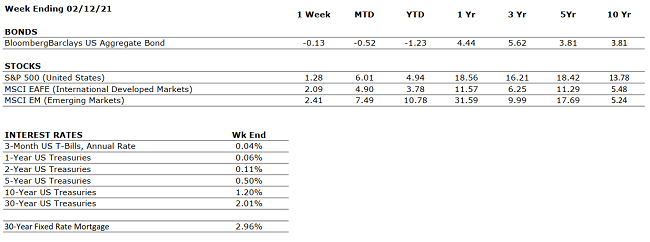

by William Henderson, Vice President / Head of Investments The markets continued to move into record high territory last week looking past COVID-19 and forward to additional stimulus, greater distribution of vaccines and a long-awaited recovery in employment. As expected, Fed Chair Jerome Powell also stuck with his dovish tone last week reminding us that the Fed has no intention of lifting from the economic accelerator for a long time. For the week ended February12, 2021, the Dow Jones Industrial Average returned +1.0%, the S&P 500 Index +1.2% and the NASDAQ +1.7%. Last week’s returns piled onto an already positive year for the markets. Year-to-date, the Dow Jones Industrial Average has returned +3.0%, the S&P 500 Index +4.9% and the NASDAQ at +9.4%. For the week, the 10-year U.S. Treasury note moved only one basis point higher to 1.16%.

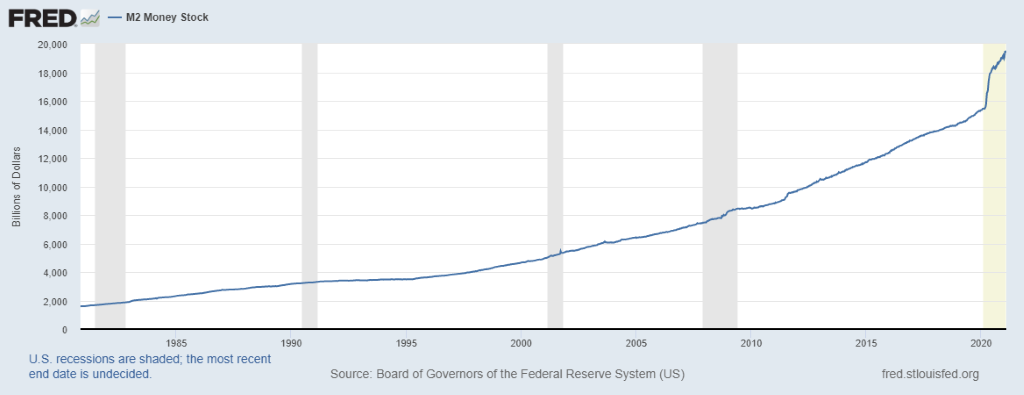

We have talked

about M2, the Money Stock of savings deposits, bank deposits and retail money market fund balances, several times

in The Weekly Commentary. The chart above from the Federal Reserve Bank of St.

Louis shows M2 sitting at record levels and indicates graphically how much

cash is sitting on the sidelines waiting to be released into a post-COVID-19

economy. An additional stimulus package of $1.5 to $1.9 trillion will only add

to those reserves. As we reach herd immunity and the magic 75% of the population vaccinated, that cash will be put to

work. Sectors like leisure, travel, energy, and retail will see a surge in

activity. It will be gradual and the journey back to normal will be bumpy and winding, but it is in sight and the markets are seeing the end game not

the path.

I feel like this

column often returns to the same thing: a dovish Fed, a willing Treasury

Secretary, an able Democratic majority party across the government, and vaccine distribution when coupled with the

sidelined cash only points to a very healthy economy in the second half of

2021. Several firms are predicting double-digit GDP prints (10%-11%) in 3Q & 4Q 2021.

Investors should look past the clamor, and instead focus on the

end game described above. It is interesting to note that on years when the

S&P 500 Index returns greater than 10%, there are between three and five market corrections

that year of 5% or more. Why does that matter? It is a reminder to investors that

corrections are normal in healthy markets and part of long-term investing.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

U.S. GDP increased at a 4% annualized rate in Q4. For the full-year 2020, the U.S. economy contracted by 3.5%, its worst performance since 1946. GDP is expected to improve meaningfully in 2021 as the American population gets vaccinated.

CORPORATE EARNINGS

NEUTRAL

With 3/4 of S&P 500 constituents having reported Q4 earnings, profit growth is coming in at 2.8% year-over-year, well in excess of analyst expectations, which figured that earnings would fall by 7%.

EMPLOYMENT

NEGATIVE

The unemployment rate declined to 6.3% in January from 6.7% in December. Labor weakness remains in sectors such as Leisure and Travel; such sectors stand to benefit as vaccine distribution accelerates.

INFLATION

POSITIVE

The Fed plans to allow inflation to temporarily overshoot its 2% target such that the long-term average is 2%. Inflation has been tame since the Great Financial Crisis, less than 2%.

FISCAL POLICY

POSITIVE

Discussions on President Biden’s a $1.9 trillion stimulus package are ongoing. If the bill passes through Congress, the U.S. economy will have received a total of approximately $4 trillion in stimulus over the trailing 12 months.

MONETARY POLICY

VERY POSITIVE

The Federal Reserve continues to indicate that the monetary environment will remain very accomodative for the foreseeable future.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

There are few, if any, looming geopolitical risks that could upset the economic recovery.

ECONOMIC RISKS

NEUTRAL

Although economic activity mostly remains below 2019’s levels, improvement has occurred across nearly every measure since the April 2020 nadir. With multiple vaccines in distribution, a second fiscal package in place, and interest rates low, 2021 is positioning to be a strong economic year.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in Wednesday, 6 PM for “Your Financial Choices” show on WDIY 88.1FM: Tax Filing Season

Laurie can take your questions live on the air at 610-758-8810, or address those submitted via yourfinancialchoices.com. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.