Tax Day is Monday, May 17! If your return has already been prepared, make sure to sign and return your 8879 forms to us authorizing filing. This is the final step for clients to make sure returns are filed with and accepted by the IRS and state authorities.

If you have not

yet given us your complete tax documentation, we are recommending filing an

extension in most cases. Extensions will extend the final filing deadline to

October 15. Please note that if it is estimated that you owe taxes, that

payment will still be due by May 17.

If you worked

with us to file your 2019 return and have made other arrangements for 2020 tax preparation,

please notify our Tax Department as soon as possible.

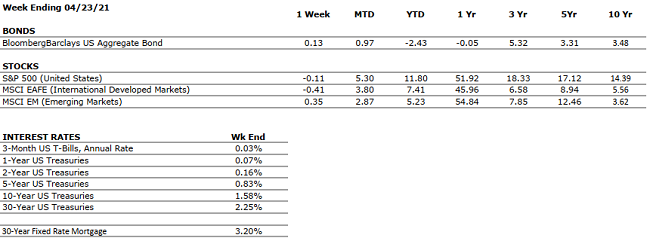

by William Henderson, Vice President / Head of Investments As is typical in any protracted bull market, major stock indices took a pause last week. As a result, we saw some selling of equities with negative returns across all three market averages. For the week that ended April 23, 2021, the Dow Jones Industrial Average fell by -0.5%, the S&P 500 Index lost -0.1% and the NASDAQ fell by -0.3%. Profit taking and selling are typical in any market especially in one that has produced such strong results since the bottom of the pandemic in March 2020. Year-to-date returns on all market indices remain solidly in the green column; with the Dow Jones Industrial Average returning +11.9%, the S&P 500 Index +11.8% and the NASDAQ +9.0%. There were whispers of a Biden-led capital gains tax increase throughout the week and demand for less risky U.S. Treasuries stayed steady. The 10-year U.S. Treasury Bond closed the week at 1.58%, unchanged from the previous week. The market still has the facets needed to sustain favorable returns going forward. Interest rates are low, fiscal stimulus is strong, corporate balance sheets are in great shape and the vaccination rate continues to increase. Quarterly earnings seasons got into full swing last week and most reports provided evidence that the economy is gradually moving to a post-pandemic environment. The last remaining market sector to continue exhibiting weakness: travel and leisure, showed a few glimmers of hope last week. Although major airlines, including Southwest, American and United, posted weak quarterly earnings, they reported seeing significant pick up in travel demand as greater numbers of people are vaccinated and therefore becoming more comfortable traveling.

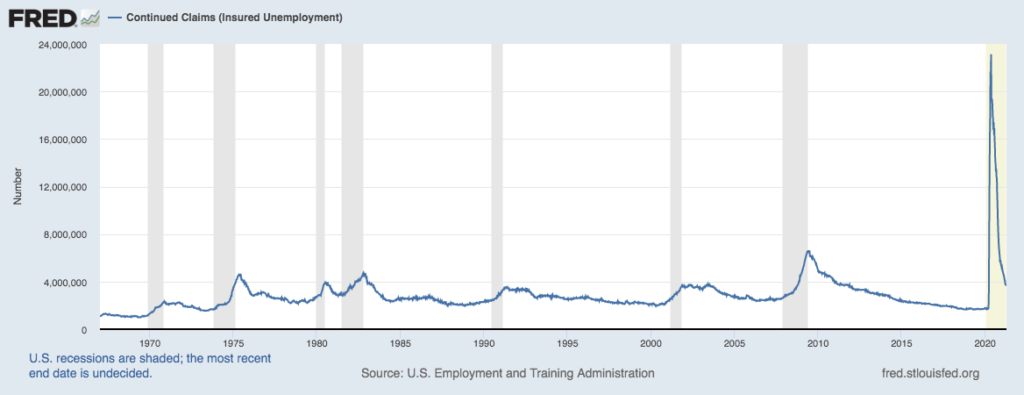

The U.S. Labor market continued

to show renewed strength. According

to the Department of

Labor and Federal Reserve Bank of St. Louis, initial

unemployment claims fell to the lowest level since the onset of the pandemic in

March 2020.

While labor and

manufacturing are showing

renewed strength, the

recovery in services on the back of vaccination efforts and the gradual lifting

of social distancing measures

should lead to accelerating growth over the remainder of

the year for

rest of the economy.

This week we have a rush of tech

stock earnings reports including

Tesla,

Facebook, Amazon, and Google. These

reports will give us a view forward to the full year of earnings if recent

strength in the sector is able to continue

its run.

Consumers have cash on hand and

healthy personal balances sheets to fuel the economic recovery well

into 2022 especially if the vaccination rate accelerates and travel and leisure

returns

to a normal level. Market setbacks like rumors of capital gains tax increases are

visible risks that

always present themselves in the short run. We like to be concerned about

the long run and staying invested and staying the course is the right plan.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

Retail sales grew nearly 10%, month-over-month, in March.

CORPORATE EARNINGS

POSITIVE

Just about 10% of S&P 500 constituents have reported Q1 earnings, however, the early results are encouraging, as sales and earnings growth has come in at 7% and 30%, respectively.

EMPLOYMENT

NEUTRAL

The unemployment rate declined to 6% in March, from 6.2% in February.

INFLATION

POSITIVE

Inflation was 2.6% in March. The Fed plans to allow inflation to temporarily overshoot its 2% target such that the long-term average is 2%. Inflation has generally been tame since the Great Financial Crisis, less than 2%.

FISCAL POLICY

POSITIVE

President Biden recently unveiled a stimulus package directed towards infrastructure that would total more than $2 trillion over eight years. President Biden is also considering a significant capital gains tax increase.

MONETARY POLICY

VERY POSITIVE

The Federal Reserve continues to indicate that the monetary environment will remain very accommodative for the foreseeable future.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

There are few, if any, looming geopolitical risks that could upset the economic recovery.

ECONOMIC RISKS

NEUTRAL

With multiple vaccines in distribution and highly accommodative fiscal and monetary policies in place, 2021 may be one of the strongest economic years on record.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.