We are pleased to welcome Brenda Hashagen to our team as Administrative Assistant. Brenda will be part of a client service team, supporting Joseph Goldfeder, CFP and working out our Bethlehem headquarters. Brenda has more than 30 years of client service experience and a background in the banking industry. Most recently she worked as a Senior Branch Operations Coordinator for M&T Bank. Brenda is immediately available to assist clients at bhashagen@valleynationalgroup.com, in the office at 610-868-9000 x136 and remotely at 610-290-4180.

by William Henderson, Vice President / Head of Investments Although the markets started the week headed down with record drops on Monday – due to a major Chinese debt holder, real estate developer Evergrande, flirting with bankruptcy, and concerns about the week’s FOMC (Federal Open Market Committee) meeting bringing Fed tapering of bond purchases – by week’s end things were in check and the markets ended flat to slightly up. Last week, the Dow Jones Industrial Average gained +0.6%, the S&P 500 Index increased +0.5%% and the NASDAQ closed unchanged. Year-to-date, the Dow Jones Industrial Average has returned +15.3%, the S&P 500 Index +19.9% and the NASDAQ +17.3%. As mentioned, China managed to stave off a major bankruptcy and the fixed income markets digested the widely anticipated tapering of the Fed’s bond-buying stimulus program. At his press conference on Wednesday, Fed Chairman Jerome Powell indicated that the Fed may cut back its bond purchases as early as this November. Further, Powell hinted that the Fed could begin a series of interest rate hikes sometime in 2022.

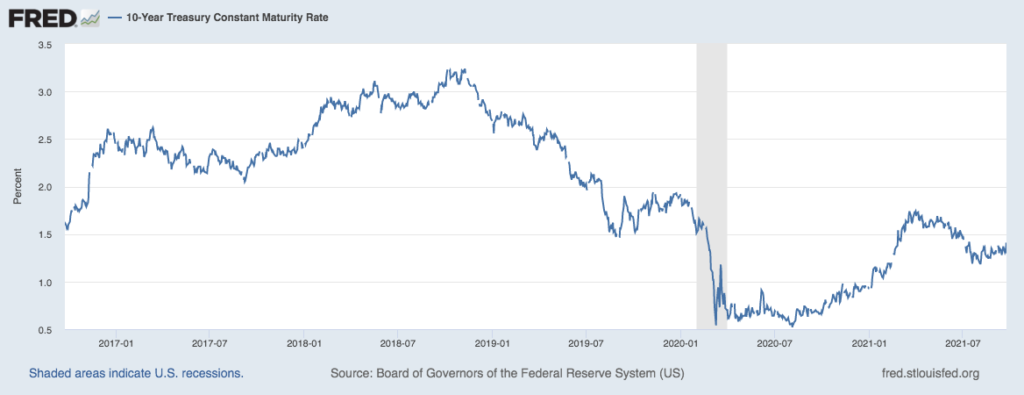

While the tapering news

was expected, the fixed

income markets still reacted negatively to

the news. By the end of the week, the 10-year

U.S. Treasury Bond reached 1.41%, eight basis

points higher than the previous week, and the

10-year note’s highest level in three months

(see chart below from the Federal Reserve

Bank of St. Louis).

Bond yields are still off their

levels seen

in March of this year when the yield on

the 10-year hit 1.74%. Investors should

understand that in a portfolio

that holds Treasury Bonds or other fixed-income securities, such as

corporate investment grade bonds, those

securities are held as a risk management tool and add stability to

the portfolio when risky assets such

as stocks sell off. While the increase in

bond yields can be attributed to Powell’s comments about tapering bond

purchases, investors garnered some comfort from the fact that monetary policy

in the form of lower interest rates will continue for

some time into 2022.

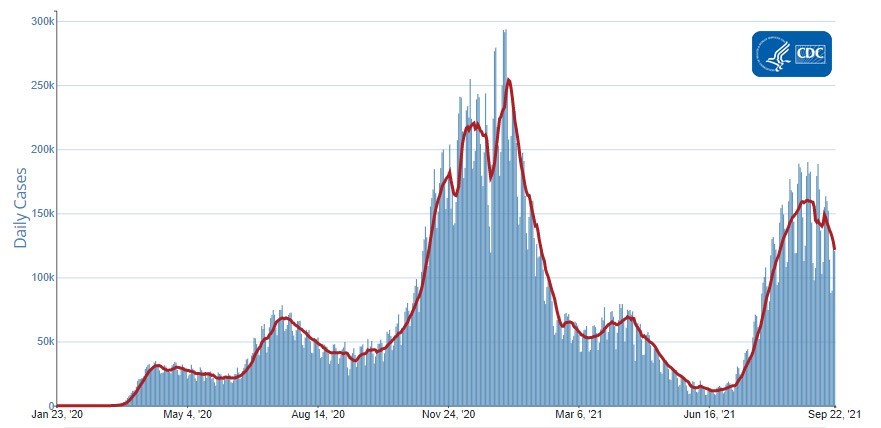

In economic news, we have seen a

nice drop in weekly COVID-19 cases (see chart below from the CDC).

COVID-19 case movements are a

critical input in consumer confidence and consumer spending. Recall

the July/August upswing in COVID-19 cases and the resulting poor reading

in the August/September consumer confidence level. Two critical

sectors, retail sales and auto sales saw

softness in

early September. With cases dropping, headwinds

become tailwinds as consumer confidence and resultant consumer

spending increase, especially heading into the holiday selling season. Further,

as COVID-related extended employment benefits end, watch for a pickup in job

growth, continued

increases in wage gains, and consumers with excess savings looking for ways to

spend. Some persistent headwinds remain,

included increasing energy prices as we near fall/winter, limited inventory of

autos and

microchips and nagging supply chain disruptions.

We are always impressed by the

market’s

ability to keep things in balance, much better so than

an impressionable and impatient investor. Global

concerns always exist whether political turmoil or bankruptcy-type risks among

foreign banks and corporations. The stability and

strength of the U.S. Federal Reserve helps to offset

global concerns by stabilizing the largest

economy in the world. Higher bond yields worry some investors,

and they whisper “Taper Tantrum” but higher

yields also indicate the

economy is well on its way to a healthy recovery. Lastly,

there’s

always sector jockeying within the stock market with growth outpacing value and

then vice versa or tech selling off but energy rallying.

The Fed is keeping monetary stimulus policy

in place well into 2022, the consumer is healthy and still eager to spend, and

corporate and bank balance sheets remain the

strongest we have seen in years. Headwinds

– tailwinds – balance.

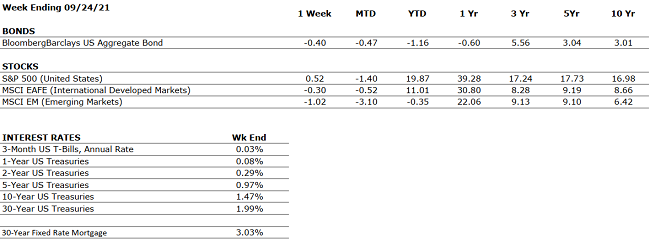

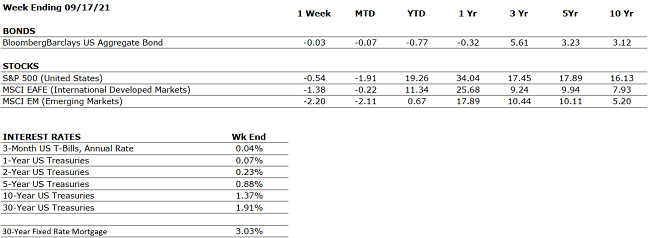

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

August retail sales surprised to the upside, increasing 0.7% month-over-month, indicating that the Delta Variant has not had a material impact on the U.S. economy.

CORPORATE EARNINGS

POSITIVE

S&P 500 Q2 sales and earnings grew an astonishing 25% and 89% respectively, when compared to the heavily depressed figures from Q2 2020.

EMPLOYMENT

POSITIVE

The unemployment rate is down to 5.2%. In August, new job creation was disappointing, but jobless claims were as low as they have been since March 2020.

INFLATION

NEUTRAL

CPI rose 5.3% year-over-year in August; CPI rose 5.4% in both June and July respectively. Fed Chairman Jay Powell is resolute that the high inflation is transitory and will decelerate as global supply chain bottlenecks resolve. Meanwhile, consumers expect CPI to be 5.2% over the next 12 months.

FISCAL POLICY

POSITIVE

The Senate passed a $1 trillion infrastructure package. The bill is expected to be voted on by The House by the end of this year.

MONETARY POLICY

POSITIVE

In recent communications, the Fed has indicated bond tapering may begin by the end of 2021 while rate hikes could commence by the end of 2022. Nonetheless, monetary policy remains relatively accommodative with rates at historical lows.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

Although the Taliban’s control in Afghanistan is concerning, it is unlikely to have a meaningful economic impact.

ECONOMIC RISKS

NEUTRAL

With multiple vaccines in distribution and accommodative fiscal and monetary policies in place, 2021 is shaping up as one of the strongest economic years on record. The primary risk at present is that of persistent inflation which begets higher interest rates.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Laurie can

address questions on the air that are submitted either in advance or during the

live show via yourfinancialchoices.com.

Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.

Team

VNFA is so pleased to be

participating again in the Community Bike Works Spin-a-thon fundraiser. Check out our VNFA Riders team

page and follow our virtual journey September 18 to October 3. https://www.pledgereg.com/3930/Team/17130

by William Henderson, Vice President / Head of Investments As predicted by the so called “market prognosticators,” September, as is typical, is shaping up to be a negative month for market returns. According to Forbes Magazine, the S&P 500 has averaged a -0.6% decline in September each year since 1945. Given how strong market returns have been thus far in 2021, a modest correction certainly seems normal and healthy for a Bull Market. Last week, the Dow Jones Industrial Average lost -0.1%, the S&P 500 Index fell by -0.5%% and the NASDAQ lost -0.5%. As noted, the small pullback last week has done little to impact the strong year-to-date gains we have had across all three major stock market indexes. Year-to-date, the Dow Jones Industrial Average has returned +16.6%, the S&P 500 Index +19.3% and the NASDAQ +17.3%. September’s typical weakness is often attributed to institutional portfolio managers locking in their strong gains in funds before year-end thereby cementing a positive performance year. Anything could be the real reason, but we have said repeatedly that in any given Bull Market, you are going to have selloffs, pullbacks, or corrections – it is what healthy markets do and how they should behave.

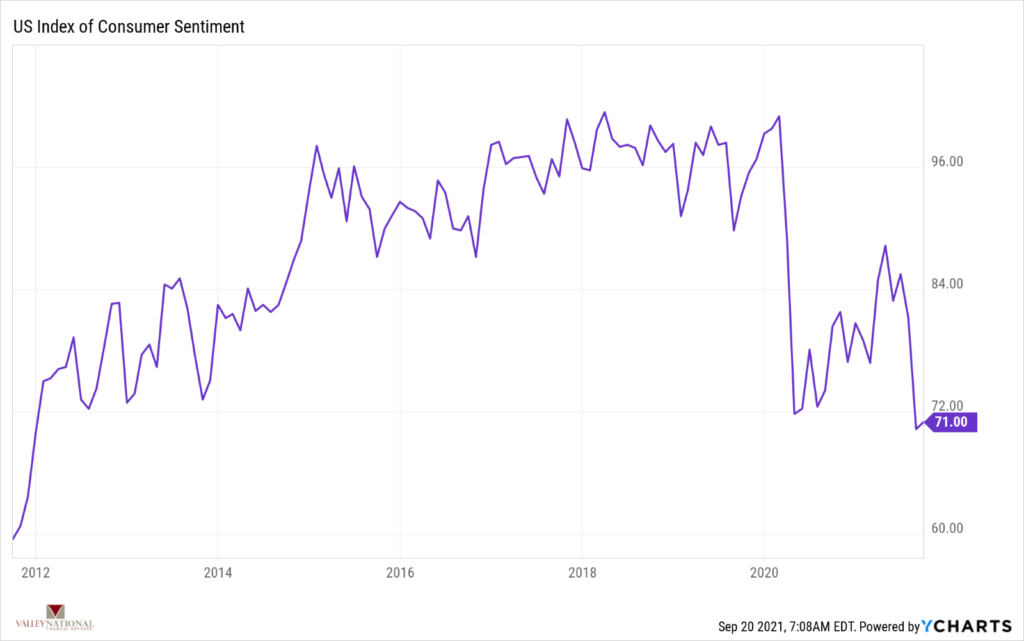

We saw some conflicting economic

data last week. While consumer sentiment has recently fallen (see

chart below from YCharts), retail sales for the month of

August rebounded sharply to +0.7% in August 2021 from

a drop of -1.8% in July 2021.

Consumer sentiment typically

predicts consumer behaviors – retail shopping – for example, so one could

assume a drop in sentiment would lead to decreases in retail

sales. Continued strong retail sales could soften economists’ expectations

for a third-quarter slowdown in economic activity. Beyond continued

concerns around COVID-19 variants and regional flare ups, crude oil,

which is a raw material used in everything from gasoline

to textiles to cosmetics, and plastics, has slowly crept higher in price

lately. U.S. prices for Brent Crude Oil rose above $70/barrel, once again

throwing inflationary concerns into in the fray. (See chart below

from YCharts).

We have a consumer with lessening

confidence but shopping more, and a Federal Reserve looking for inflation but a

consumer weary of higher prices for goods and services. Meanwhile,

despite higher prices for crude and regional labor shortages, Wal-Mart

announced they are hiring an additional 20,000 workers and Amazon

announced they are hiring 125,000 workers, both before the

holiday season. Again – conflicting data and news items.

This week, the U.S. Federal

Reserve will hold its two-day meeting to discuss monetary policy

including opinions on interest rates and whether to continue

their bond purchasing stimulus program. It has been assumed

by economists that as the economy rebounds, the Fed should begin to reduce it

bond purchases – so called “tapering.” Hence all the noise about a

“taper tantrum,” or selloff in fixed income markets when the Fed is

no longer the buyer at large. First, while the Fed is a significant buyer

of bonds, other major buyers include large financial institutions,

such as pension funds, endowments, mutual funds, insurance companies, banks, and individuals. Those additional buyers

will remain even after the Fed reduces its purchases. That said, all the

recent choppy and conflicting economic data certainly gives the Fed all

the ammunition it needs to keep interest rates low and to continue their

bond purchasing stimulus program. In fact, we expect the Fed to

remain on hold and modestly note that eventual tapering in bond

purchasing will begin before the end of 2021.

COVID-19 variants, issues with

China, supply chain disruptions and concerning crude oil prices worry us

but there is always offsetting good news. Let us keep focused on

the Fed and the healthy U.S. Consumers and U.S. Corporations, both of

which are flush and sitting on extraordinarily strong balance

sheets. These are strong forces impacting the economy and

the markets.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

August retail sales surprised to the upside, increasing 0.7% month-over-month, indicating that the Delta Variant has not had a material impact on the U.S. economy.

CORPORATE EARNINGS

POSITIVE

S&P 500 Q2 sales and earnings grew an astonishing 25% and 89%, respectively, when compared to the heavily depressed figures from Q2 2020.

EMPLOYMENT

POSITIVE

The unemployment rate is down to 5.2%. In August, new job creation was disappointing, but jobless claims were as low as they have been since March 2020.

INFLATION

NEUTRAL

CPI rose 5.3% year-over-year in August; CPI rose 5.4% in both June and July, respectively. Fed Chairman Jay Powell is resolute that the high inflation is transitory and will decelerate as global supply chain bottlenecks resolve. Meanwhile, consumers expect CPI to be 5.2% over the next 12 months.

FISCAL POLICY

POSITIVE

The Senate passed a $1 trillion infrastructure package. The bill is expected to be voted on by The House by the end of this year.

MONETARY POLICY

POSITIVE

The Federal Reserve has indicated that it does not plan to increase interest rates until 2023.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

Although the Taliban’s control in Afghanistan is concerning, it is unlikely to have a meaningful economic impact.

ECONOMIC RISKS

NEUTRAL

With multiple vaccines in distribution and accommodative fiscal and monetary policies in place, 2021 is shaping up as one of the strongest economic years on record. The primary risk at present is that of persistent inflation which begets higher interest rates.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in Wednesday, 6 PM for “Your Financial Choices” with

Laurie Siebert on WDIY 88.1FM. Laurie will discuss: Listeners’

Questions

Laurie can

address questions on the air that are submitted either in advance or during the

live show via yourfinancialchoices.com.

Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.