The name “Juneteenth” is a combination of “June” and “nineteenth,” marking the day in 1865 when Union General Gordon Granger announced the end of slavery in Galveston, Texas.

Texas was the first state to officially recognize Juneteenth as a state holiday in 1980.

Juneteenth is also known as Freedom Day, Jubilee Day, Liberation Day, and Emancipation Day.

Juneteenth is celebrated in various ways, such as parades, marches, and barbecues. Many gather for ceremonies featuring public service awards, prayers, and the raising of the Juneteenth Flag.

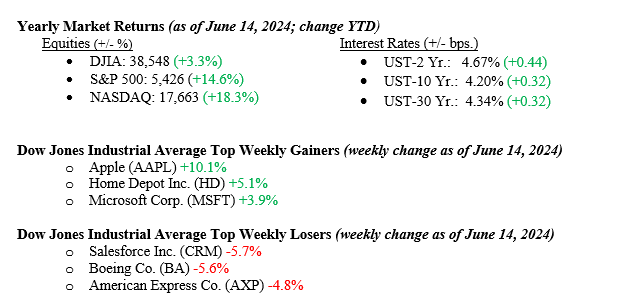

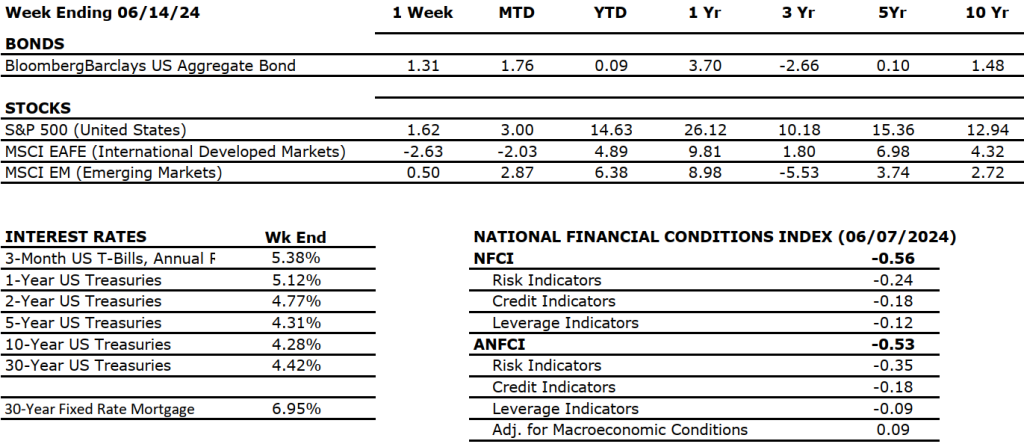

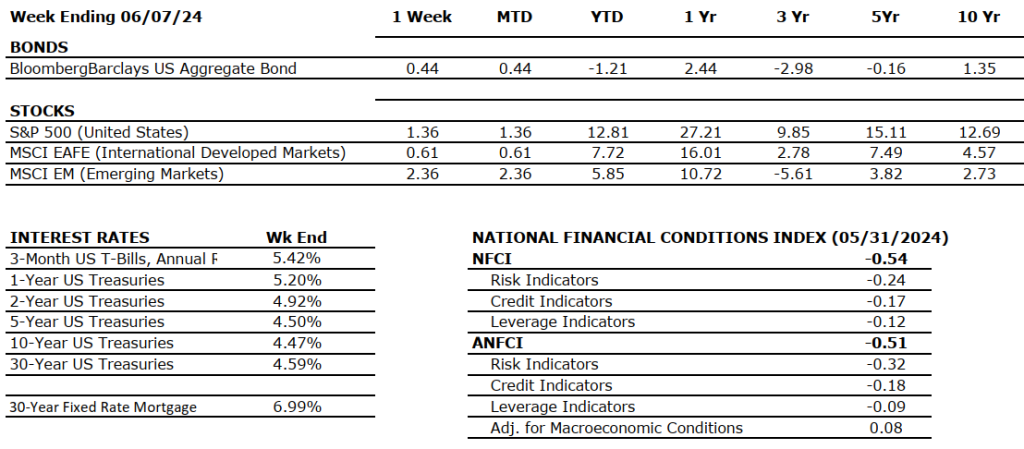

Last week, the S&P 500 and NASDAQ surged to new record highs, continuing their upward trajectory. The NASDAQ led the charge with a strong 3.3% total return, surpassing the S&P 500, which posted a 1.6% gain, while the Dow lagged with a slight decline of 0.5%. Positive U.S. inflation data and highlights from the June FOMC meeting bolstered investor confidence, driving upward market momentum. However, an equally weighted version of the S&P 500 underperformed its capitalization-weighted index by 215 basis points, indicating a more narrowly focused market. Information technology was the standout sector of the week, surging 6.4%, whereas energy and financials both experienced declines of over 2%. Last week, the markets saw 10-year U.S. Treasury closed at 4.20%, a stunning 23 basis points lower than the previous week.

U.S. & Global Economy

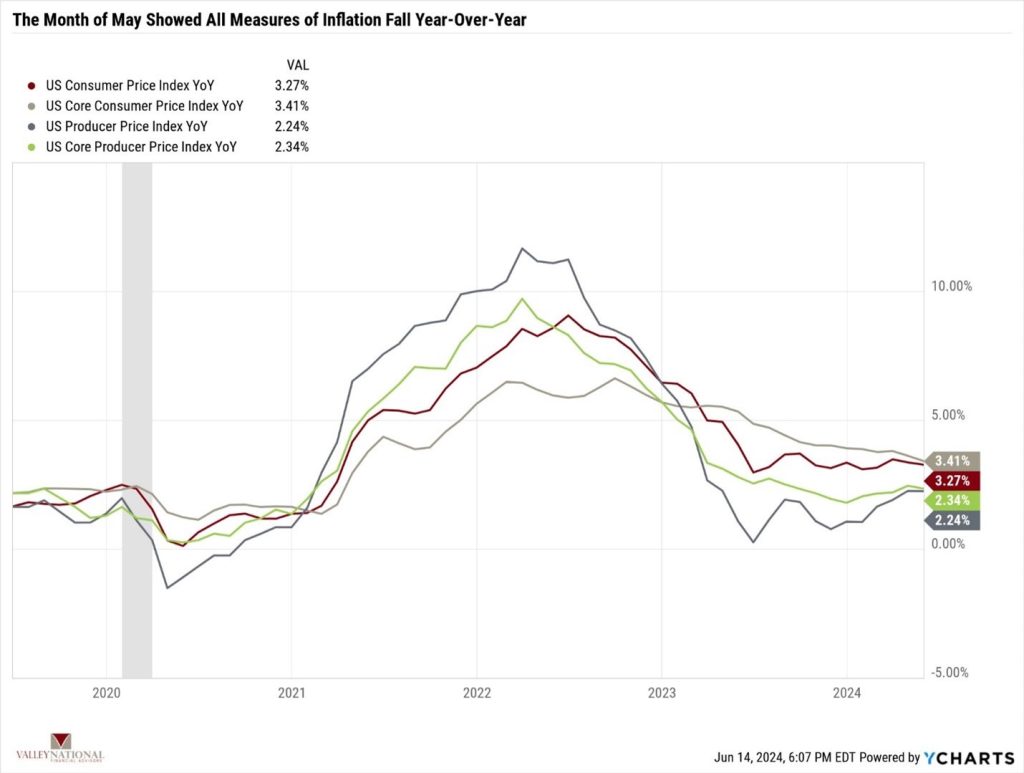

Last week, inflation data showed much-welcomed lower readings. See Chart 1 below from Valley National Financial Advisors & Y Charts. The consumer price index (CPI) remained unchanged in May, the first time in nearly two years. Core prices, excluding food and energy, increased by 0.2%, slightly below expectations and hitting a seven-month low. Year-over-year core inflation dropped to 3.4%, the lowest since April 2021.

Similarly, producer price index (PPI) inflation fell unexpectedly by 0.2% in May, halting five consecutive months of increases, and core PPI every year fell to 2.3%. Concurrently, import prices declined by 0.4%, the first drop in four months. However, concerns over economic health emerged as weekly jobless claims unexpectedly rose, with 242,000 Americans filing for unemployment, the highest in nearly a year, and continuing claims reaching 1.82 million, the third-highest level in the past year. Despite these developments, the Federal Reserve showed minimal reaction to the benign inflation data, maintaining its stance after its policy meeting and projecting a slight increase in core PCE inflation expectations for 2024. While leaving interest rates unchanged as anticipated, Fed officials revised their median forecast for the federal funds rate to 5.1% by the end of 2024, suggesting a single rate cut later in the year despite acknowledging some progress on inflation.

Policy and Politics

President Biden is behind former President Trump by approximately one percentage point in national polls and about two percentage points in Pennsylvania, a critical swing state crucial for securing the electoral vote. Prediction markets suggest an even chance between the two candidates.

On Friday, President Vladimir Putin stated that Russia would cease the war in Ukraine only if Kyiv abandoned its NATO aspirations and ceded control of four disputed provinces to Moscow. Kyiv promptly dismissed these demands as akin to surrender.

After the French far-right won a significant victory in the European elections, President Macron dissolved the lower chamber of the French Parliament and scheduled legislative elections for June 30 and July 7. This move sparked a notable sell-off, with the index that tracks large-cap European stocks dropping 2.4% for the week.

Economic Numbers to Watch This Week

U.S. Empire State manufacturing survey for June 2024, prior –15.6%.

U.S. U.S. retail sales for May 2024, prior 0.0%.

U.S. Home Builder confidence index for June 2024, prior 45.

U.S. Housing starts for May 2024, prior 1.36 million.

U.S. Philadelphia Fed manufacturing survey for June 2024, prior 4.5.

U.S. Existing home sales for May 2024, prior 4.14 million.

U.S. Leading economic indicators for May 2024, prior –0.6%.

We are looking for signs that the market’s strength is broadening beyond the dominant tech giants that have been leading the charge. We need consistent market broadening for equity indexes to continue their move higher. Anticipated rate cuts later this year are expected to ease financial pressures on smaller capitalization companies struggling with higher interest rates. We applaud the Fed for its efforts in lowering inflation thus far and appreciate its commitment to a 2% inflation target. Higher interest rates have impacted inflation, yet the economy remains comfortably strong across many sectors. It is also encouraging to see the World Bank raise its forecast for global economic growth in 2024, partly due to improving conditions in the U.S. The bottom line is that there are plenty of reasons for investors to feel optimistic. Please contact your advisor at Valley National Financial Advisors with any questions.

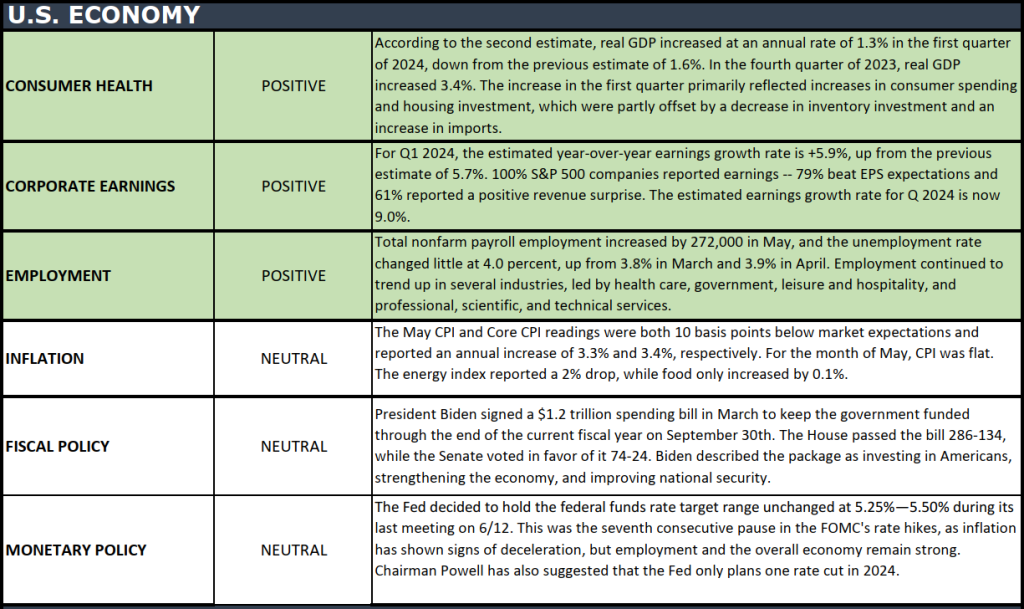

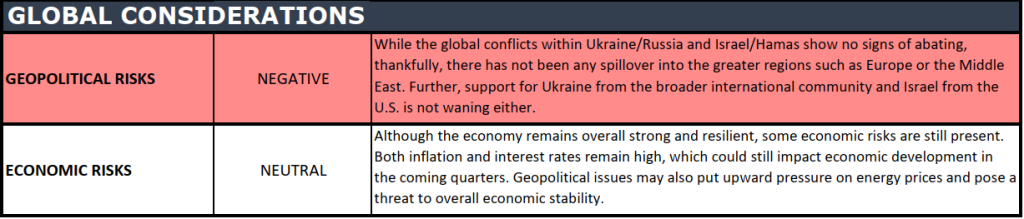

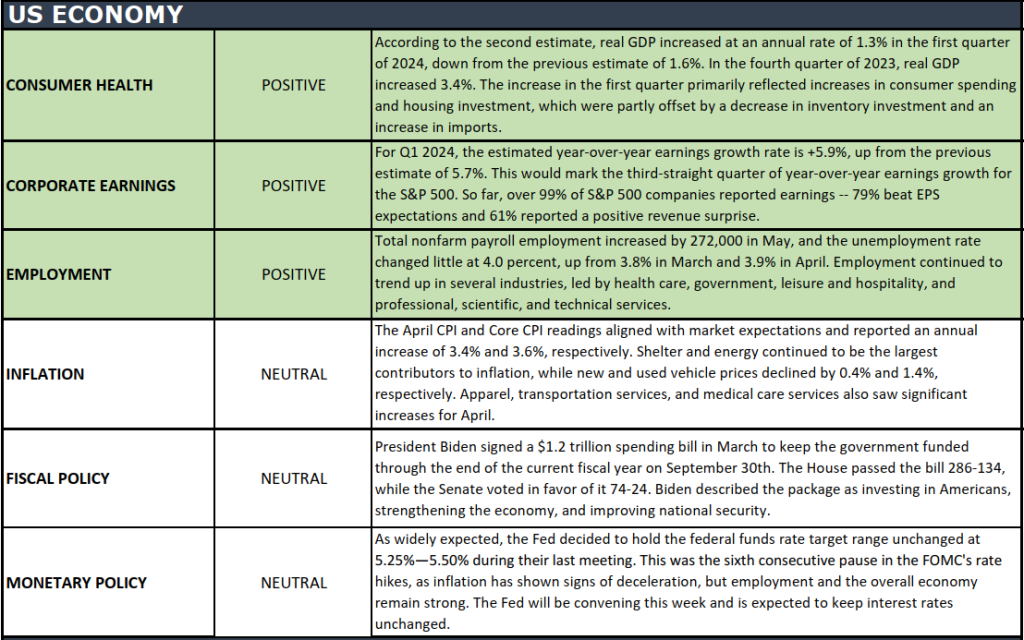

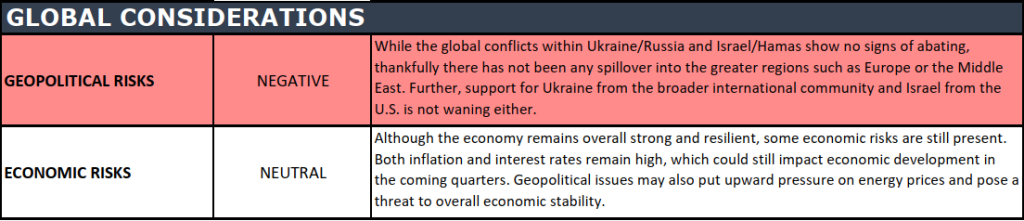

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade key economic conditions that we believe are of particular importance to investors.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in Wednesday, 6 PM, for a pre-recorded “Your Financial Choices” show on WDIY 88.1 FM. Laurie will address questions submitted online during the next live broadcast.

Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.

Did you miss the last show, Reviewing Retirement Account Options? Listen Here

#TeamVNFA was honored to present a contribution to fund 7,404 meals for Second Harvest Food Bank of Lehigh Valley and Northeast Pennsylvania. This contribution arose from a joint initiative with WDIY 88.1 FM during their Spring Membership Drive.

Thank you to all the members and donors who not only supported local public radio but also helped feed more people in our Lehigh Valley region. #WDIY #CommunityImpact #SupportLocal #HungerAdvocacy

To learn more about Second Harvest Food Bank of Lehigh Valley and Northeast Pennsylvania, visit https://shfblv.org/ .

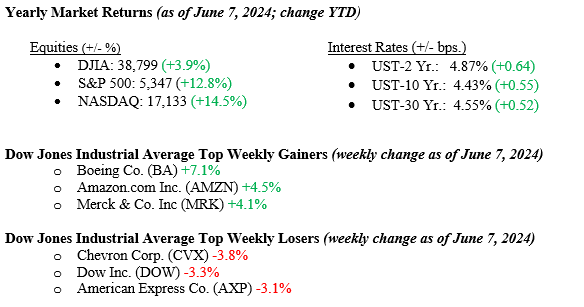

Last week, the markets saw modest rallies in all three major stock market indices. The NASDAQ led the charge, registering a 2.4% increase, while the Dow Jones Industrial Average saw a marginal rise of 0.3%, and the S&P 500 Index recorded a gain of 1.3%. Continued strength in technology, particularly those companies related to artificial intelligence such as Nvidia (NVDA), carried the week. While acknowledging the significance of market leaders such as NVDA and other AI giants, it’s essential to note that favorable returns are evident across all market sectors. This observation comes amidst the backdrop of the U.S. economy maintaining its status as a growth juggernaut. Last week’s new jobs report showed that for May 2024, the U.S. economy added 272,000 new jobs, which was well above economists’ forecasts for only 180,000 new jobs. The solid growth in new jobs and related wage growth leads us to believe that the Fed remains comfortably on the sidelines regarding rate cuts. The 10-year U.S. Treasury closed the week at 4.43%, eight basis points lower than the previous week.

U.S. & Global Economy

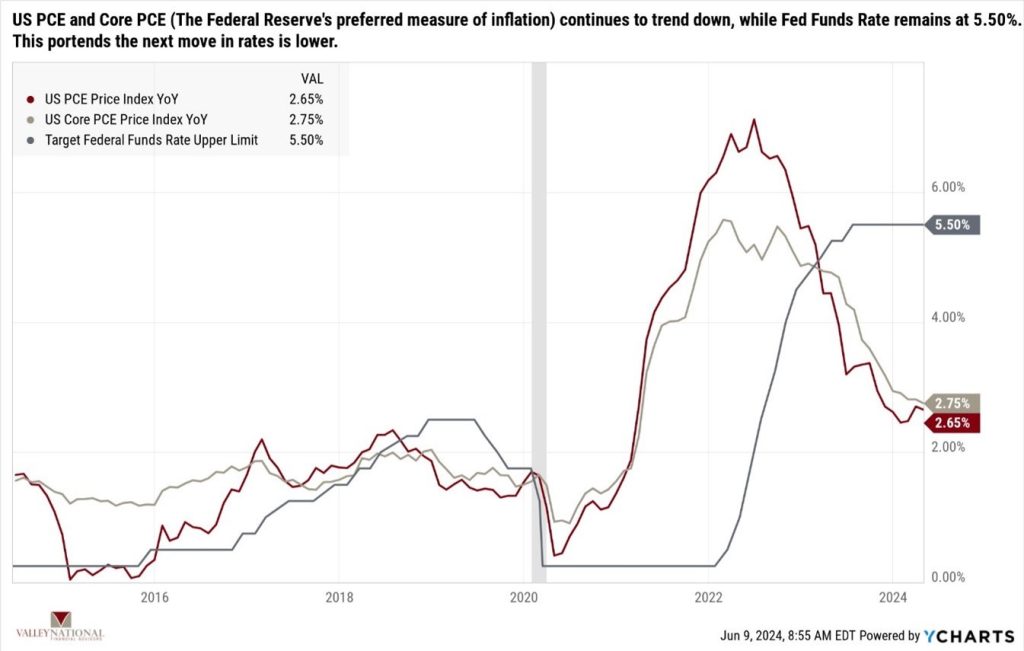

Economic data from last week suggests that the Federal Reserve, convening this week, will likely maintain its current stance on interest rates, opting to stay on the sidelines. We at Valley National Financial Advisors and all major economists agree that the next move by the FOMC will be to lower the Fed Funds Rate. However, not everyone agrees on when this will happen. Last week, we saw an explosive job number, as highlighted above. At the same time, we saw lower levels on the US PCE and Core PCE Index, which are the Federal Reserve’s preferred inflation measures. See Chart 1 below from Valley National Financial Advisors and Y Charts. The economic data released last week shows that the U.S. economy continues to grow and add jobs, and inflation continues to slowly but steadily decrease. The combined impact suggests that Fed Chairman Jay Powell is nearing completion of his goal, alluding to the elusive concept of a soft landing.

Policy and Politics

Despite ongoing global unrest, with conflicts in Ukraine and Israel persisting, there’s also notable progress in the expansion of democracies. Major leadership elections in Mexico saw Claudia Sheinbaum elected as the country’s first female president, while in India, over 652 million people voted, reaffirming their support for Prime Minister Narendra Modi. While unrest and suffering persist globally, it’s important not to overlook the positive developments. Often, these movements garner more attention from markets and worldwide economies than the prevailing negatives.

Economic Numbers to Watch This Week

U.S. Consumer Price Index YoY for May 2024, prior 3.36%.

U.S. Core Consumer Price Index YoY for May 2024, prior 3.62%.

U.S. Inflation Rate for May 2024, prior, 3.36%.

U.S. Target Fed Funds Rate as of May 2, 2024, current rate 5:50%.

U.S. Producer Price Index YoY for May 2024, prior 2.17%.

U.S. Core Producer Price Index YoY for May 2024, prior 2.37%.

U.S Index of Consumer Sentiment for June 2024, prior 69.10.

Last week, economic reports showed a growing economy (strong new job creation) with inflation retreating (PCE falling). This week, investors will get a fresh set of data, including Core CPI, the week’s FOMC meeting results, and the consumer sentiment index on Friday. Just understand and appreciate that the markets are more efficient than investors. If you look at where all the major stock market indexes have gone in the past year (hint: higher), you will see why investors should pay attention to long-term trends and only invest for the long term. Please contact your advisor at Valley National Financial Advisors with any questions.

Questions can be submitted to yourfinancialchoices.com before the live show. Recordings of past shows are available to listen to or download at yourfinancialchoices.com and wdiy.org.

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade key economic conditions that we believe are of particular importance to investors.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.