THE NUMBERS

THE NUMBERS

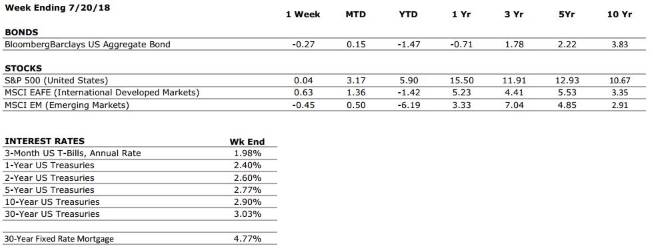

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

US ECONOMIC HEAT MAP

The health of the US economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

|

CONSUMER SPENDING |

A+ |

Consumer spending is expected to remain healthy as individuals with lower tax rates spend their windfalls. |

|

FED POLICIES |

C- |

Following its June meeting, the Federal Reserve implemented the second rate hike of 2018, and suggested that two more hikes should be expected before year-end. Rising interest rates tend to reduce economic growth potential and can lead to repricing of income producing assets. |

|

BUSINESS PROFITABILITY |

A |

Q2 Earnings season is now underway and analysts are expecting an 8th consecutive quarter of positive earnings per share growth for the S&P 500. |

|

EMPLOYMENT |

A+ |

The US economy added 213,000 new jobs in June, and the labor force participation rate is now on the rise. Jobs are available for those who want them. |

|

INFLATION |

B |

Inflation is often a sign of “tightening” in the economy, and can be a signal that growth is peaking. The inflation rate remains benign at this time, but we see the potential for an increase moving forward. This metric deserves our attention. |

|

OTHER CONCERNS |

||

|

INTERNATIONAL RISKS |

5 |

The above ratings assume no international crisis. On a scale of 1 to 10 with 10 being the highest level of crisis, we rate these international risks collectively as a 5. These risks deserve our ongoing attention. |

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

In case you missed it, the July 11 “Your Financial Choices” radio show featured three professionals from our team!

In case you missed it, the July 11 “Your Financial Choices” radio show featured three professionals from our team! The show airs on WDIY Wednesday evenings, from 6-7 p.m. The show is hosted by Valley National’s Laurie Siebert CPA, CFP®, AEP®. On this week’s show – July 25 – guest hosts Rodman Young, CPA/PFS, CFP® and Jaclyn Cornelius, CFP®, EA from Valley National Financial Advisors, will discuss: “Company transitions and your job.”

The show airs on WDIY Wednesday evenings, from 6-7 p.m. The show is hosted by Valley National’s Laurie Siebert CPA, CFP®, AEP®. On this week’s show – July 25 – guest hosts Rodman Young, CPA/PFS, CFP® and Jaclyn Cornelius, CFP®, EA from Valley National Financial Advisors, will discuss: “Company transitions and your job.”