Valley National is pleased to again partner with WDIY and Second Harvest Food Bank to help feed those in need throughout the Lehigh Valley.

During the WDIY Fall Pledge Drive – which kicks off on October 8 – every $100 donated to support WDIY will trigger an automatic contribution by VNFA directly to Second Harvest to pay for 21 meals. Last year, this partnership resulted in a donation to fund 12,000 meals!

Listen in at WDIY 88.1 FM on Thursday, October 11 at 6 p.m. to hear our CEO Matt Petrozelli discuss the partnership on a special edition of Lehigh Valley Discourse.

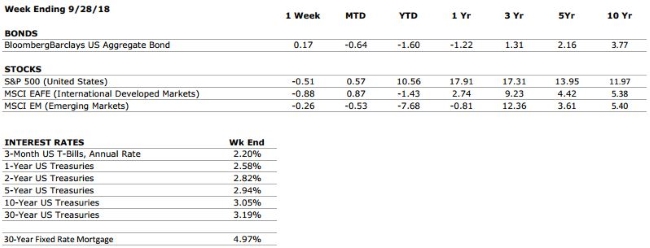

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

US ECONOMIC HEAT MAP

The health of the US economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

CONSUMER SPENDING

A+

Consumer spending is expected to remain healthy as individuals with lower tax rates spend their windfalls.

FED POLICIES

C-

Last week, the Federal Reserve raised interest rates for the third time this year. Rising interest rates tend to reduce economic growth potential and can lead to repricing of income producing assets.

BUSINESS PROFITABILITY

A

Factset is reporting a blended earnings growth rate of 20% YoY for the 2nd quarter of 2018. Tax reform has played a major role, but the strength of the US consumer is boosting corporate profits as well. We will get our first glimpse of Q3 earnings in just a couple short weeks.

EMPLOYMENT

A+

The US economy added 201,000 new jobs in August and the unemployment rate remained below 4%. Additionally, weekly jobless claims fell to their lowest level in over 50 years last week. The job market remains very healthy.

INFLATION

B

Inflation is often a sign of “tightening” in the economy, and can be a signal that growth is peaking. The inflation rate remains benign at this time, but we see the potential for an increase moving forward. This metric deserves our attention.

OTHER CONCERNS

INTERNATIONAL RISKS

5

The above ratings assume no international crisis. On a scale of 1 to 10 with 10 being the highest level of crisis, we rate these international risks collectively as a 5. These risks deserve our ongoing attention.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

If you have not reached full retirement age and you are within 12 months of when your benefits started, you can submit the Social Security Form SSA-521 explaining why you want to withdraw your application. Keep in mind, if your request is approved you will be required to pay back all the benefits you and your family received to that point. Be aware that you are limited to one withdrawal per lifetime.

If you have reached full retirement age, but are not yet age 70, you can request to have your retirement benefit payments suspended. This will allow the benefits to accumulate 8% annual delayed credits, albeit on the reduced amount. This type of request does not require an official form – you can make it orally or in writing. Carefully consider some rules the SSA outlines as well, made effective in 2016.

It is important that you consult with your financial advisor before making these types of decisions to be sure that you understand all the ramifications of your financial choices. You can read more about these options on the Social Security Administration website at ssa.gov.

“Retirement is like a long vacation in Las Vegas. The goal is to enjoy it to the fullest, but not so fully that you run out of money.” – Jonathan Clements

US equities continued to push higher during the third quarter, fueled by strong earnings growth and an improving economic backdrop. Barring a significant pullback in Q4, the US equity market is on pace to outperform its international counterparts for the seventh time in the past ten years. The fundamental strength in the US economy has helped US stocks shrug off the questions raised by the ongoing global trade saga, but international stocks, without the luxury of corporate tax reform boosting earnings and growth, have been unable to elude the risks of shifting global trade patterns and weakening currencies. Emerging markets have had a difficult year, and though there was a marked improvement over the volatility observed during Q2, risks in Turkey and Argentina have threatened to spill over into other markets and have made investors weary.

Bonds:

Bond returns have been flat to slightly negative in 2018, and we expect the headwinds posed by rising interest rates to continue until monetary tightening is paused, which doesn’t appear to be anytime in the immediate future. Federal Reserve Chairman Jerome Powell suggested at the end of September that the Fed anticipates rate hikes could continue into 2020, which would put the Fed Funds rate at about 3% by that time; just 0.25% below the current yield on a 30 Year Treasury. President Trump has made it clear that he is displeased with the Fed’s decision to continue hiking rates, but it is important to remember that the Fed is an independent body designed to operate free of political interference, and we do not expect the president’s comments to be an influencing factor in future monetary policy decisions.

Outlook:

The fourth quarter will bring with it some intriguing potential catalysts for markets, and there are a few key things that we are watching moving forward:

1. The Shape of the US Yield Curve

One of the most consistent themes of the past several years has been the flattening of the US yield curve (short term interest rates have risen faster than long term interest rates). Historically, a flattening yield curve has been a bearish signal for markets and the economy, prompting many to wonder if the bull market was finaly winding down. However, we saw a small but meaningful break from this pattern at the end of the third quarter, and one reason for this may have been an increase in inflation expectations.

2. US Inflation

Throughout this prolonged economic recovery, inflationary pressure has been conspicuously absent. But with tightening labor conditions and rising oil prices, it would not be surprising to see inflation finally become a factor for the Fed to ponder when it considers its next policy move. Higher inflation would likely force the Fed to keep its policy of increasing interest rates intact for longer.

3. Mid Term Elections

It is no secret that the Trump Administration has made it a key policy initiative to focus on US trade policy, and the negotiating tactics that have been utilized have caused some disruption in global markets.

Depending on the impact that the mid term elections have the President’s political capital, he may be forced to take a more passive stance. If that happens, international equities (and emerging markets in particular) may find their footing as some of the uncertainty created by trade rhetoric fades to the backdrop.

VIDEO: Q3 Market Commentary – Connor Darrell, Head of Investments, shares Valley National Financial Advisors’ review of the third quarter, and a fourth quarter outlook. WATCH NOW

by Connor Darrell, Head of Investments As was anticipated by markets, the Federal Reserve increased interest rates last week and officially removed the word “accommodative” from its description of current monetary policy. While parsing words can be trivial, the Fed selects its language very carefully when crafting its statements, and the change represents a symbolic shift in how the Fed views the current rate environment. The days of “easy money” policies are now officially behind us.

Global equity markets were slightly negative in the final week of the third quarter, with U.S. markets pulling back slightly from the all-time highs achieved the week prior. Investors’ attention will now turn to Q3 earnings season, which officially kicks off next week. Factset is currently predicting Q3 earnings growth of 19.3% for S&P 500 companies, which would mark the third highest growth rate since the first quarter of 2011.

The show airs on WDIY Wednesday evenings, from 6-7 p.m. The show is hosted by Valley National’s Laurie Siebert CPA, CFP®, AEP®. This week Laurie will discuss: “Considerations in the transition from working to retirement.”

Laurie will take your calls on this or other topics at 610-758-8810 during the live show, or via yourfinancialchoices.com. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.

VIDEO: Spend 5 minutes with Laurie to review her top takeaways from September and a preview of this month’s show topics lined up for Your Financial Choices. WATCH NOW

Valley National is pleased to again partner with WDIY and Second Harvest Food Bank to help feed those in need throughout the Lehigh Valley.

Valley National is pleased to again partner with WDIY and Second Harvest Food Bank to help feed those in need throughout the Lehigh Valley.