by Connor Darrell CFA, Assistant Vice President – Head of Investments

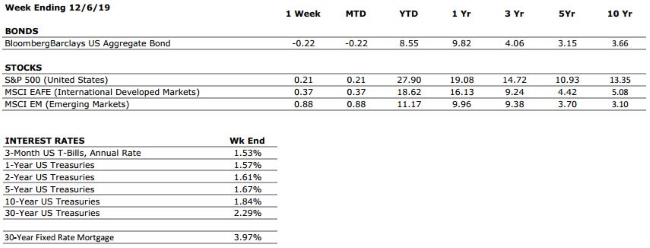

Global equity markets ended the week higher as Friday’s very strong U.S. employment report helped erase losses from earlier in the week. Of particular note was that the report showed evidence of strong growth in the manufacturing sector, an area which has been a source of concern due to the uncertainty of global trade. From almost every angle, the report provided reason for optimism. The unemployment rate ticked back down to match its 50-year low of 3.5% and wage growth was over 3%; well above the current inflation rate. The data continues to suggest that the strength of the U.S. consumer is helping the economy to weather the impact of the ongoing U.S.-China trade war.

The Impact of E-Commerce on U.S. Employment

No matter how the data is sliced and diced, Friday’s jobs report was a blockbuster. But it’s interesting to note some trends that have emerged with respect to employment patterns during the holiday season. It’s no secret that over the past several years, holiday shoppers have begun to favor making purchases from the comfort of their own homes rather than braving the elements and long lines at brick and mortar retailers. As a result, there’s been a shift in hiring practices for seasonal employees in the jobs data. Last week’s employment report showed a 6% decline in retail employment gains compared to just one year ago, but that loss was more than made up for in other areas such as wholesale (likely a result of more hiring at warehouses and fulfillment centers supporting online shopping). It’s still debatable whether the methodology used to track retail sales data does enough to capture the massive shift in consumer preferences toward online shopping, but this week’s round of retail sales data should help lend further support to the idea that the U.S. consumer can continue to carry the expansion forward.