by Connor Darrell CFA, Assistant Vice President – Head of Investments NOTE: Last week, we reported an incorrect number for the December jobs report, which was not released until 1/10. Refer to the “Heat Map” for more details on the most recent employment data.

The U.S. equity market extended its

gains last week as tensions between the U.S. and Iran showed signs of easing. Markets

seem to no longer anticipate an escalation in the conflict between the U.S. and

Iran following what has been seen as a largely unprovocative response to the

killing of Qassem Soleimani on the part of the Iranians. With geopolitical

risks at a heightened level, there remains the risk for additional unsettling

headlines that could spark volatility, but it is unlikely that any such

headlines would have a material impact on global markets.

Here in the U.S., the December jobs

report came in weaker than anticipated, though the unemployment rate remained

at its 50-year low of 3.5%. Wage growth, which had shown signs of picking up

during the latter half of 2019, also came in weaker than expected. The 2.9%

annual rate of increase was the lowest reading since July of 2018. Month-to-month

jobs data tends to be somewhat unpredictable, and we continue to view the

employment situation, and tangentially the U.S. consumer, as the strongest

component of the U.S. economy. In the coming weeks, we will be watching the

beginning of Q4 earnings season for further insights into consumer spending

during the holiday season.

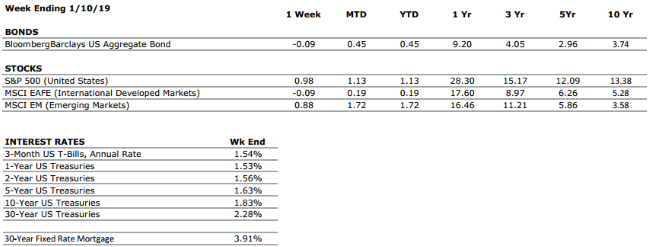

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

U.S. ECONOMIC HEAT MAP

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

CONSUMER SPENDING

A

Our consumer spending grade remains an A despite recent softening in retail sales numbers. US consumer confidence remains high, and we anticipate a strong holiday shopping season. The consumer has been the bedrock of the US economy through much of the current expansion.

FED POLICIES

B+

With the Federal Reserve expected to refrain from any further adjustments to interest rates without a material change in the economic outlook, we have downgraded our Fed Policies grade to a B+. The low level of interest rates remains a positive for markets, but sentiment will likely no longer be aided by anticipated rate cuts.

BUSINESS PROFITABILITY

B-

As was largely expected by markets, corporate earnings growth was weak during Q3 as a result of the global slowdown and trade policy uncertainty. However, according to Factset, 75% of S&P 500 companies reported a positive earnings surprise, meaning things were not quite as weak as many had feared.

EMPLOYMENT

A

December’s headline jobs growth number of 145,000 missed consensus expectations, though the unemployment rate remained stable at 3.5%; a 50-year low. Despite the softer than anticipated results in December 2019 was an incredibly strong year for the labor market, and it remains the healthiest area of the economy.

INFLATION

A

Inflation is often a sign of “tightening” in the economy and can be a signal that growth is peaking. Recent inflationary data has increased slightly, but inflation remains benign at this time, which bodes well for the extension of the economic cycle.

OTHER CONCERNS

INTERNATIONAL RISKS

7

We have raised our International Risks metric to a 7 following the US airstrike which killed Iranian General Qassem Soleimani. We expect heightened volatility in markets as a result of the further escalation of tensions that this action represents. However, we stress that volatility stemming from geopolitical events tends to be short-term.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Form 1099-MISC Filing Requirements As a general rule, you must issue a Form 1099-MISC to each individual, partnership, Limited Liability Company (“LLC”), Limited Partnership (“LP”), or Estate you have paid at least $600 during the calendar year in services, rents, or legal fees. Note that personal payments are not reportable.

Form 1099-MISC is also required if you withheld any federal

income tax under the backup withholding rules regardless of the amount of the

payment.

Some payments do not have to be reported on Form 1099-MISC,

although they may be taxable to the recipient. The most common exceptions are

payments to a corporation (including an LLC that is treated as a C or S

corporation), payments of rent to real estate agents or property managers, and

payments made with a credit card or payment card and certain other types of

payments, including third-party network transactions.

Form 1099-MISC are due by January 31, 2020. You can submit

Form 1099-MISC to the IRS by mail or online, using the Filing Information

Returns Electronically (FIRE) system. Please note that if you issue more than

250 information returns, you are required to file electronically and may be

penalized if you fail to do so.

The IRS operates a

centralized call site to answer questions about reporting on Form 1099 and

other information returns. If you have questions related to reporting on

information returns, the IRS centralized call site can be reached at (866)

455-7438.

The show airs on WDIY Wednesday

evenings, from 6-7 p.m. The show is hosted by Valley National’s Laurie Siebert

CPA, CFP®, AEP®.

This week, Laurie and her guest, Nicholas Nanovic, Esq., LL.M., AEP®

from Gross McGinley, LLP, will discuss: “Trusts – general estate planning,

minor trusts, A/B trusts and more.”