We welcome Lorin Ross to the VNFA

Team! Lorin joined us in the full-time position of Finance Associate. She has seven years of experience in

operational and technical accounting.

Lorin will work out of VNFA’s Bethlehem headquarters as part of the internal finance and accounting department under the supervision of Elizabeth Wilson, CPA who has been promoted to Chief Financial Officer. She will manage all aspects of wealth management fee billing and commissions, as well as help maintain accurate and reliable financial records. Lorin has a Master of Business Administration in Accounting from St. Josephs College and has spent the last three years working as a Senior Accountant in Long Island, NY.

Lorin is also a certified Emergency

Medical Technician (EMT) and has a Property & Casualty Insurance license. “I’m

very excited about joining Valley National and I look forward to using my

skills and background to help VNFA grow,” she said. Lorin loves spending time

with her family. She lives with her husband of eight years and her

seven-year-old daughter, as well as four dogs and some chickens.

A fresh look for valleynationalgroup.com! We have been working with a talented team at Weidenhammer to update our website, and we are pleased to be unveiling the new valleynationalgroup.com this week. We can’t wait to hear what you think about the refresh.

by Connor Darrell CFA, Assistant Vice President – Head of Investments Global equity markets retreated from their previous highs last week as evidence emerged that the new coronavirus continued to spread outside of mainland China. About a dozen Chinese cities, including Wuhan at the center of the outbreak, are on lockdown as China’s Lunar New Year celebrations begin. Many public celebrations have been canceled and travel restrictions have been imposed during what is one of China’s busiest holiday seasons. Markets are reflecting concerns over the potential impacts of the virus on the global economy, and we have begun to observe a rotation out of risk assets such as stocks and toward the relative safety of fixed income investments. As a result of this rotation, yields moved lower across most of the yield curve last week, generating positive returns for bonds.

The true economic impact of the

coronavirus will not be measurable until after the outbreak has been contained,

but many have looked to the SARS outbreak of late 2002 and 2003 for a point of

reference. A report issued in 2004 estimated that the SARS outbreak cost the

world economy over $40 billion dollars, but the overall market impact proved to

be somewhat limited. The major risk to markets at this point in time still

stems from the “fear factor” that the new virus is creating, which may

ultimately pose a risk to consumer spending and travel expenditures. Adding to

the uncertainty is the fact that the virus has an unusually long incubation

period of up to two weeks, which makes it likely that current reports are

underestimating the number of infected people. However, it is important to note

that even if the disease continues to spread, its impacts may still be

significantly lower than that of the seasonal flu, which kills an estimated

50,000 people every year. The heightened level of concern surrounding the new

coronavirus is likely at least in part due to the simple fact that it is new

and foreign. It is human nature for us to have a heightened sense of fear of

something that we do not understand and are unfamiliar with.

We have adjusted our assessment of

“geopolitical risks” in our heat map to a negative at this point in time to

reflect the heightened concerns surrounding the novel virus, but do not believe

that the effects will be long-lasting. We will continue to monitor the

disease’s impact on the global economy and markets moving forward and will

provide additional updates in future commentary.

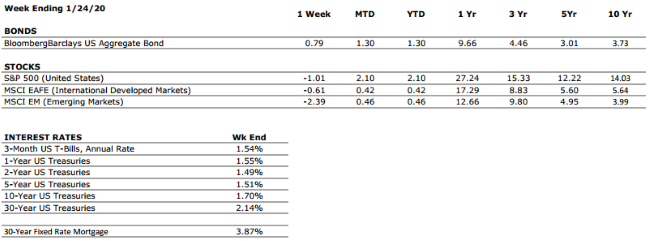

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

U.S. ECONOMIC HEAT MAP

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

VERY POSITIVE

The consumer has been the bedrock of the US economy through much of the current expansion and we have seen little to suggest that this cannot continue.

CORPORATE EARNINGS

NEUTRAL

Corporate earnings growth was weak throughout 2019 as a result of slowing in the global economy and trade policy uncertainty. However, analysts are expecting mid to high single digit earnings growth in 2020, which will be important to sustaining recent levels of equity returns.

EMPLOYMENT

VERY POSITIVE

December’s headline jobs growth number of 145,000 missed consensus expectations, though the unemployment rate remained stable at 3.5%; a 50-year low. Despite the softer than anticipated results in December 2019 was an incredibly strong year for the labor market, and it remains the healthiest area of the economy.

INFLATION

POSITIVE

Inflation is often a sign of “tightening” in the economy and can be a signal that growth is peaking. Recent inflationary data has increased slightly, but inflation remains benign at this time, which bodes well for the extension of the economic cycle.

FISCAL POLICY

POSITIVE

The Tax Cuts and Jobs Act of 2017 lowered the effective tax rates for many individuals and corporations. We view the cuts as a tailwind for economic activity over the next several years.

MONETARY POLICY

POSITIVE

With the Federal Reserve expected to refrain from any further adjustments to interest rates without a material change in the economic outlook, it is unlikely that changes in Fed Policy will disrupt the economic cycle in the near future. Furthermore, the low absolute level of interest rates remains a positive for markets.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEGATIVE

We have adjusted our assessment of Geopolitical Risks to NEGATIVE as a result of the continued spread of the coronavirus outside of mainland China. The virus poses a threat to economic growth consumer spending in affected regions as a result of the “fear factor” it induces.

ECONOMIC RISKS

NEUTRAL

Due to low inflation and weak economic activity, central banks around the world remain in a very accommodative stance. We have seen some recent evidence of modest recovery in places like Germany, but we expect global economic growth to remain modest overall.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

“Patience is power. Patience is not an absence of action; rather it is ‘timing’ it waits on the right time to act, for the right principles and in the right way.”– Fulton J. Sheen