by Connor Darrell CFA, Assistant Vice President – Head of Investments Global equities recorded healthy gains last week as optimism rose that the economy could remain resilient in the face of the new coronavirus outbreak. At this point, the total impact on economic activity remains impossible to quantify, and investors can expect markets to remain jittery until the virus is eventually contained. We have seen little over the last week that would help us to update our current assessments of contagion and severity. The death rate among those infected still sits at around 2%, and while the rate of contagion has also remained somewhat stable, a recent Chinese research report suggests that the virus can spread in multiple ways. Both of these metrics deserve our ongoing attention, as they can help us to assess the potential magnitude of the disease’s impact on the economy, as well as whether the economic effects will largely remain confined to mainland China.

At present, the most impacted areas

of the market outside of Chinese equities have been at the sector level. The

travel and industrial sectors, as well as some commodity markets have seen more

volatility than most other assets as a result of the immediate impacts of quarantines

and reduced global travel demand. The technology sector is one that has

continued to perform well but could come under pressure if recent containment

efforts in China fall short and the virus is able to spread beyond the Hubei

Province. One of the biggest differences between the SARS outbreak of 2003 and

the current situation is that China is now a much larger component of the

global economy, particularly in the technology supply chain. While Hubei

province itself is not a major technology hub within China, there are multiple

neighboring provinces which contain key production centers for many key inputs

in the production of smart phones, TVs, and semiconductors.

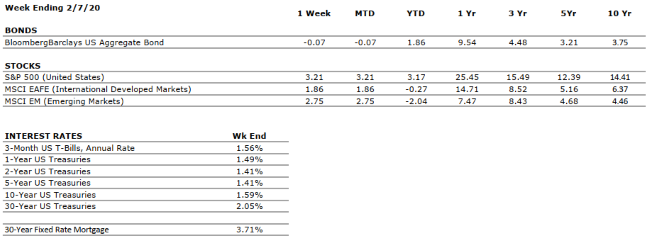

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

U.S. ECONOMIC HEAT MAP

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

VERY POSITIVE

The consumer has been the bedrock of the US economy through much of the current expansion and we have seen little to suggest that this cannot continue.

CORPORATE EARNINGS

NEUTRAL

Corporate earnings growth was weak throughout 2019 as a result of slowing in the global economy and trade policy uncertainty. However, analysts are expecting mid to high single digit earnings growth in 2020, which will be important to sustaining recent levels of equity returns.

EMPLOYMENT

VERY POSITIVE

The economy added 225,000 new jobs in January, exceeding consensus expectations. The report also indicated that the unemployment rate ticked up to 3.6% as a result of more people looking for jobs. The expansion of the labor force should be taken as an additional sign of the confidence

Americans have in the health of the labor market.

INFLATION

POSITIVE

Inflation is often a sign of “tightening” in the economy and can be a signal that growth is peaking. Recent inflationary data has increased slightly, but inflation remains benign at this time, which bodes well for the extension of the economic cycle.

FISCAL POLICY

POSITIVE

The Tax Cuts and Jobs Act of 2017 lowered the effective tax rates for many individuals and corporations. We view the cuts as a tailwind for economic activity over the next several years.

MONETARY POLICY

POSITIVE

With the Federal Reserve expected to refrain from any further adjustments to interest rates without a material change in the economic outlook, it is unlikely that changes in Fed Policy will disrupt the economic cycle in the near future. Furthermore, the low absolute level of interest rates remain a positive for markets.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEGATIVE

Our assessment of Geopolitical Risks is NEGATIVE at this time as a result of the continued spread of the coronavirus outside of mainland China. The virus poses a threat to economic growth and consumer spending in affected regions as a result of the “fear factor” it induces.

ECONOMIC RISKS

NEUTRAL

Due to low inflation and weak economic activity, central banks around the world remain in a very accommodative stance. We have seen some recent evidence of modest recovery in places like Germany, but overall, we expect global economic growth to remain modest.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Mid-February Tax Reminders We need each of our tax clients to complete a questionnaire every year as part of our return preparation process. Our team has either sent you a paper copy or a link. Please make sure you complete this and deliver it to us, in addition to your tax documents. Click here to access the online questionnaire.

S Corporation and Partnership

returns with a December 31 year-end are due March 16! Send us your information

as soon as you have all or most of it together so that we can get ahead of this

deadline.