In light of the announcements yesterday by

the CDC and our government to avoid gatherings of more than 10 people, we are

closing our physical office locations as of 4 p.m. today (March 17) until

further notice.

Our VNFA Team is asking that

you stay safe and stay home. Our team is set up to be able to continue our

service remotely. We will remain accessible via phone and through our digital

access points. Please

note the following resources for you to maintain immediate contact with your

VNFA Team:

Please continue to call our main

number 610-868-9000 or email us at FromOurTeam@valleynationalgroup.com. We will help get you to the right

employee, even if they are remote. We will have designated staff available

for trades, money movement, and general service.

Follow us on social media, Facebook (@ValleyNationalFinancialAdvisors), Twitter (@VNFAsince1985), and LinkedIn (Valley National Financial Advisors).

Additionally, all important announcements will be posted on our website.

The tax deadline is rapidly approaching.

Please understand that the tax preparation process may be impacted. Our

team is already anticipating filing a larger amount of extensions. We will

stay in regular communication with you to make sure that you know what to

expect moving forward.

In the interest of healthy best practices

at this time, we remind you that our secure eVault Client

Portal is a solution for

document exchange. If you do not have a portal or you are unsure about how

to use it to post, view and download documents, please contact your

service team.

These

times will pass. In the meantime, we plan to continue to serve you and your

families as we have for the past 35 years. If you have any questions, please

contact us. It is important that you feel supported and secure as we move

together through these challenges.

by Connor Darrell CFA, Assistant Vice President – Head of Investments As the threat of COVID-19, the disease caused by the novel coronavirus, has continued to escalate over the past few weeks, fear and panic have gripped financial markets and society at large. The risks emanating from the fallout of the virus’ spread have wreaked havoc on financial markets and pushed equities well into bear market territory. Since it first became apparent that containment of the virus was no longer reasonably achievable, we have spent a great deal of time trying to assess the long-term economic risks that the virus poses. The unpredictability and fluidity of the situation makes any economic forecasting extremely difficult, and that is part of the reason that markets have reacted the way they have. But in times of stress, it’s imperative that investors maintain perspective. With this edition of The Weekly Commentary, we aim to summarize some of the key facts that we have learned over the past few weeks, share our latest assessment on the economy and markets, and offer perspective on how to look forward rather than backward.

COVID-19: What Do We Know? As the scientific community has scrambled to ramp up research efforts and gain a better understanding of this novel disease, there has been no shortage of information being shared via news publications, scientific journals, and word of mouth. Despite the amount of resources being dedicated to research, the fact of the matter is that these analyses take time, and much is still unknown about how the virus operates. We do know that based on the data it has available, the World Health Organization recently made the decision to officially declare the current situation a global pandemic; a decision that many believe should have been made much earlier. We also know that scientists are finally beginning to get a handle on exactly how the disease spreads and how it compares to prior pandemic diseases.

A comparison to

prior pandemic diseases is one of the simplest ways to assess the potential

impacts of COVID-19, but it is important to note that each pandemic is unique

by nature. Coronavirus pandemics are a relatively new phenomenon (many other

pandemics throughout history have been flu viruses), so there are fewer points

of reference for the current situation, but when compared to the virus that

caused the SARS outbreak in 2002, the strain of coronavirus causing COVID-19

appears to be less lethal and have a lower rate of transmission. However, this

disease has been much more difficult to contain because patients are contagious

for a much longer period of time and often while exhibiting no symptoms at all.

As a result, modest containment measures that respond only to confirmed cases

where patients are exhibiting symptoms have been rendered ineffective.

The general

expectation among experts is that the virus will continue to spread through

community transmission, eventually reaching peak levels at some point over the

next 6-8 weeks. Faced with that reality, we anticipate widespread school

closures and recommended telecommuting by employers. We also expect economic

stimulus in the form of both monetary and fiscal policy initiatives aimed at

providing stability to markets and assurances for impacted families and

businesses. President Trump addressed the nation on Wednesday evening, offering

some preliminary measures that did not appear to appease markets, leading to

further large-scale losses during Thursday’s trading session. However, we

anticipate additional measures will be discussed and eventually passed through

Congress.

The Current State of Markets and the Economy The swift and violent nature with which markets have responded to the threat of COVID-19 has been a result of a variety of factors. First, market sentiment was extremely positive coming into the year as a result of improving economic fundamentals and anticipation for accelerating earnings growth. Those lofty expectations led to lofty asset prices, which meant stocks had further to fall once the full threat of COVID-19 became appreciated. Secondly, the exogenous shock to the economy that COVID-19 represents is not something that can be easily addressed through traditional economic policy initiatives. Lower interest rates and tax relief will not stop the spread of the virus, adding to the uncertainty of the situation. Lastly, the immediate reduction in demand for oil resulting from the spread of COVID-19 has coincided with a political struggle between Russia and Saudi Arabia with respect to oil production capacity. Both nations are looking to exert pressure on other oil producers in order to gain market share, and this has led to a sharp decline in the price of oil. Oil’s decline has resulted in a rush of “risk-off” sentiment in corporate credit markets, of which energy producing companies make up a large share of borrowers. It’s important to note however, that lower oil prices will be a net positive for consumers once the spread of the virus subsides and consumer behavior normalizes.

As might be

inferred from reading the paragraph above, the variety of threats that have

surfaced in recent weeks represent a material risk to economic activity over

the next several months. It is not out of the realm of possibility that the global

economy falls into a technical recession (defined by two consecutive quarters

of negative economic growth rates), but we believe there are a number of

reasons for investors to remain optimistic about the ensuing recovery.

First, we know

that the U.S. economy is addressing these threats from a position of strength.

As a result of significant reforms enacted following the global financial

crisis, U.S. banks are extremely well capitalized and are well positioned to

deal with potential stress. Secondly, the risks that the economy faces are

quite different from those of a “traditional” recession. Typical recessions

result from internal shocks such as an asset bubble, monetary policy missteps,

or weaknesses in the financial system. These types of recessions often lead to

structural issues within labor markets that force the reallocation of labor and

resources to different industries. For example, the housing crash and financial

meltdown in 2008 led to a substantial reallocation of resources away from construction

and real estate, and many jobs that were lost were permanently eliminated. By

contrast, as the economy emerges from the impacts of COVID-19, workers are more

likely to be able to simply return to their previous jobs and resume economic

output. At the very least, the friction we have seen in prior recessions which

has slowed the recovery in labor markets is likely to be significantly less

prevalent. As such, we believe it is reasonable to anticipate that confidence

would rebound more quickly than analyses of prior periods of economic stress

might suggest.

Lastly, given

the market’s disappointment in the President’s remarks on Wednesday, we

anticipate that the federal government will continue to look at more aggressive

policy action moving forward. In fact, we have already seen progress on this

front, as the House of Representatives passed a bipartisan legislative package

over the weekend which the Senate is expected to vote on this week. This

package will be aimed at providing assistance to impacted families and

businesses, and there are already discussions in place for further measures to

be taken as needed. We believe that the timing of additional fiscal responses

will be important, with measures focused on boosting demand being enacted after

the disease reaches its inflection point in order to maximize their impact.

Looking Forward At this point in time, equity markets are about 28% off of their previous highs. Given our assessment of the economic picture and the prospects for a relatively swift recovery (though the timing remains uncertain), we believe that the vulnerability of the human psyche has exacerbated market declines, and that market prices have begun to separate from what might be considered rational. Furthermore, the size of the selloff in equities has likely led to significant portfolio drift in many instances. And while we would never seek to “call the bottom” (and consistently advise our clients against attempting to do so), we have long preached that disciplined investors should seek to rebalance to long-term target allocations whenever portfolio drift becomes significant. This principle is true in both up and down markets. As such, rather than falling victim to the fear and panic which have gripped markets and society, we believe investors should begin looking for opportunities to rebalance portfolios. While it can often be emotionally difficult, this process involves purchasing assets such as equities which have significantly depreciated over the past few weeks. Rebalancing does not necessarily need to be achieved in one trade, but it is an important tool for keeping portfolios aligned with what is required to achieve long-term goals.

The rapidity of

the market’s reaction to the spread of COVID-19 has been historic. But as

discussed above, our assessment at this point in time is that panic has played

a significant role in what we have seen from markets, especially over the past

week. When markets are being driven by panic, a disciplined and objective

approach to portfolio management is of the utmost importance. As such, it is

important for us to focus on what we can control rather than what we cannot.

This does not only include details related to our investment portfolios

(maintaining an asset allocation that is appropriately aligned with our

investment goals), but in the wake of the mounting threat we face as a society,

it also includes simple things like proper hand hygiene, taking necessary

precautions as recommended by authorities, and working together to protect ourselves

and our communities. We do not know when the market will find its bottom or how

long it will take for our lives to return to normal, but we do know (because we

have seen it in China and in South Korea) that we will emerge on the other side.

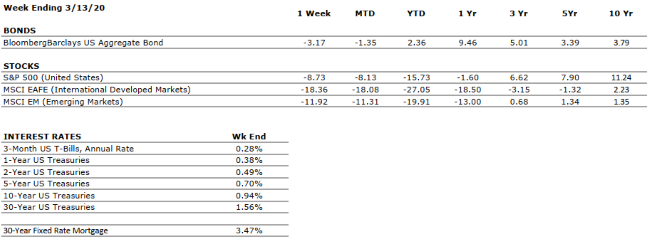

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

The consumer has been the bedrock of the US economy through much of the current expansion, and remains in a strong position. However, we have further reduced our grade to NEUTRAL as a result of the unprecedented social distancing and quarantining efforts currently being employed to fight the spread of COVID-19.

CORPORATE EARNINGS

NEUTRAL

Coming into the year, analysts were expecting mid to single digit earnings growth, but the spread of COVID-19 is likely to have a substantial impact on near-term earnings forecasts. However, earnings could bounce back quickly once the pandemic has run its course.

EMPLOYMENT

POSITIVE

The February jobs report once again exceeded consensus expectations. The spread of COVID-19 will likely stunt job growth in the near-term, but we still view the potential for permanent job losses as a result of the pandemic as very low.

INFLATION

POSITIVE

Inflation is often a sign of “tightening” in the economy, and can be a signal that growth is peaking. The deflationary environment created by COVID-19 should provide additional room for robust stimulus from both fiscal and monetary policy initiatives.

FISCAL POLICY

POSITIVE

We anticipate a significant fiscal response to the COVID-19 outbreak, and expect that the government will make a concerted effort to provide economic relief to industries and families who are most impacted by the economic fallout of the pandemic.

MONETARY POLICY

VERY POSITIVE

In response to the threat of COVID-19, the Federal Reserve has implemented two emergency rate cuts and has moved its target interest rate back to zero. Additionally, it has announced its intention to conduct further asset purchases to support markets. We believe that the Fed is doing all it can to support the economy and markets.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

VERY NEGATIVE

With COVID-19 being declared a global pandemic, our geopolitical risks rating is VERY NEGATIVE. However, we think it is important for investors to disentangle the public health concerns over the near-term from the expectations for markets over the long-term. The pandemic remains a near-term issue at this time.

ECONOMIC RISKS

VERY NEGATIVE

As discussed in our commentary, COVID-19 represents a real threat to economic activity globally. However, we do expect that the eventual economic recovery will occur more swiftly than from previous economic shocks.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Defending Against COVID-19 Cyber Scams The Cybersecurity and Infrastructure Security Agency (CISA) warns individuals to remain vigilant for scams related to Coronavirus Disease 2019 (COVID-19). Read more from the U.S. Department of Homeland Security.