The CARES (Coronavirus Aid, Relief, and

Economic Security) Act There

is and will continue to be a lot of information available about the details of

this 800+ page bill that was signed into law on March 27th. As your

trusted team, we are analyzing how any relief items in the bill may apply to

our individual clients and their financial planning moving forward. Here is a

quick list of the most asked topics so far. Consult your advisor to learn more.

Individual Recovery Payments The eligibility for and amount of payments being given to individuals is based on Adjusted Gross Income (AGI) reported on the latest tax return on file with the IRS – 2019 if that return has been filed, if not your 2018 AGI will be used. The one-time payments will be given based on the following thresholds: Married Filing Joint: $150,000; Head of Household: $112,500; All Other Filers: $75,000.

Required Minimum Distributions Waived For 2020, all RMDs are suspended, including those for inherited IRAs as well as traditional IRAs of those over age 70½. For RMDs already taken in 2020, you have up to 60 days to return a distribution to an IRA or deposit it in another qualified retirement account.

Penalty for Early Retirement Distributions Waived The 10% penalty for taking early distributions from qualified retirement plans, including IRAs and 401(k)s, is waived. The waiver applies to distributions taken between January 1, 2020 and December 31, 2020. Up to $100,000 of distributions can avoid the penalty.

Retirement Plan Loan Rules Modified For those impacted by coronavirus allowed loan amounts are doubled to $100,000. The modifications include an increase to allow use of up to 100% of the vested balance, and loan payment may be deferred up to one year.

For individuals with Federal student

loans, payments may be deferred until September 30, 2020. For small businesses,

including self-employed, the CARES Act includes payroll tax deferrals in

addition other available credits, loans and assistance.

Here are some of our top picks for

articles to help you understand the basics of the CARES Act.

by Connor Darrell CFA, Assistant Vice President – Head of Investment Last week brought another series of large swings in equity markets as investors had to balance the still uncertain (though expectedly profound) impacts of government quarantining efforts relating to COVID-19 with historically strong economic policy responses. Markets managed to push meaningfully off of their lows, largely buoyed by optimism surrounding economic policy support. On Monday, the Federal Reserve announced that it would uncap the amount of capital it could pump into financial markets and established other means of providing liquidity to the system. This aggressive action was followed just days later with the passage of a $2.2 trillion fiscal response (known as the CARES Act) aimed at providing aid to troubled workers and businesses. Also hidden in the week’s news flow was a massive increase in claims for unemployment benefits, which skyrocketed to 3.3 million, smashing the previous record of 695,000. Additional data revealed that euro zone and Japanese manufacturing was in the midst of a sharp contraction. We expect the economic data to continue to worsen before getting better but remind investors that much of the negative data likely to come is already expected by markets, which are forward-looking by nature.

Behavioral Finance:A Primer Much

of our previous communication has been focused on providing our interpretation

of the data related to the pandemic, as well as frequent reminders of the

importance of discipline. But for many investors who are facing an

unprecedented amount of volatility in markets, remaining disciplined is much

easier said than done. As human beings,

our brains are wired to address risks and evaluate decisions in certain ways,

and in many instances, the mechanics of our cognitive functions can lead us to

make investment decisions that may prove to be contrary to our best financial

interests.

Interestingly, there is an entire field of

finance that is devoted to studying the psychology of investing. Advancements

in our understanding of the human decision-making process

have provided practitioners of “Behavioral Finance” with lots to offer in terms

of understanding the behavior of investors. In our view, one of the most

important benefits of understanding behavioral finance is that we can use our

understanding of our own psychology to help improve our investment decision

making. Below, we provide a summary of some of the most significant

psychological pitfalls and how they may negatively impact us over the

long-term:

1. Loss Aversion

All investors hate losing money, but the

concept of loss aversion goes beyond this simple notion and suggests that human

beings’ aversion to paper losses can greatly impact investment decisions.

Specifically, study after study has shown that the “pain” associated with

losing money on an investment is more powerful than the “pleasure” derived from

earning it. In the midst of a volatile market, this can cause us to feel the

urge to take action in an effort to protect ourselves from realizing further

losses, even if such action would not be in concert with our long-term

investment objectives. In order to combat this desire, it is essential for us

to focus on our goals and objectives in an effort to focus on the things we

have direct control of over time. This might include

making temporary adjustments to our savings and consumption rates or taking

advantage of cost-saving

opportunities such as lower interest rates, rather than making drastic

adjustments to our portfolios.

2. Confirmation Bias

Another flaw in the way we digest

information is confirmation bias. Confirmation bias occurs when we

inadvertently place higher emphasis on data or information that supports what

we already believe, rather than taking it into consideration at face value. For

example, if we believe strongly in the resiliency of the U.S. economy, we may

overemphasize positive information about U.S. stocks and discount whatever negative views we may

encounter that do not support

this belief. For many of us, this bias

may lead to us rushing to sell positions that have underperformed on a relative

basis and flock to those that have performed better. Giving in to these types

of biases can cause us to sacrifice proper diversification in our portfolios at

the precise time that diversification takes on heightened importance.

3. Herding

Herding is the behavior that leads to our

desire to “follow the crowd.” This is often driven by fear of regret or of

“missing out” (also known as FOMO). Throughout history, there are a plethora of

examples of points in time where market sentiment reached levels that were far

too extreme (this includes periods that fall in both bull and bear markets). In

these instances, those who were able to refrain from following the popular

decision (whether that be to buy more when stocks were expensive, or to sell

when markets were in peril) have often come out ahead. Given the volatility we

are experiencing now, it is important for us to take a step back and develop

our own conclusions rather than simply following the trend.

4. Illusion of Control

Illusion of control bias is a bias in

which people tend to believe that they can control or influence outcomes when,

in fact, they cannot. One example of this bias in a practical study occurred

when a social experiment conducted in the 1980’s found that people permitted to

select their own numbers in a hypothetical lottery game were willing to pay a

higher price per ticket than subjects gambling on randomly assigned numbers.

The belief that we have more control than we really do on the outcome of our

investment returns can lead us to take inappropriate action within our

portfolios. To combat this, it is important to think of investing as a

probabilistic activity, and that the probability of different outcomes is

beyond our control. During periods of market stress, it can be easy to lose sight

of the fact that long-term returns are driven largely by circumstances beyond

our control, and that the probability of experiencing positive returns

increases with an investor’s time horizon.

5. Representativeness

Representativeness is a type of selective memory

that causes us to place too much weight on recent evidence rather than taking a

more holistic approach to decision making. This can cause investors to focus

too much on short-term performance without considering the evidence that may be

found in the more distant past. With markets having fallen so quickly from

their highs, there are likely to be many high-quality

stocks out there which still have very promising long-term prospects but may have fallen considerably off of their

previous prices. If we become too concentrated on the recent past, or even on

the fact that these businesses may operate in industries that could be

particularly troubled in the current environment (i.e., energy or

consumer discretionary), we may be more likely to lose sight of the business’

strengths.

All of the above

biases are particularly important to consider in the current investing climate,

because they can lead us to make suboptimal decisions during a time of stress.

Behavioral economists have found that we can help to reduce the negative

impacts that our cognitive biases may have on our decision-making process just by simply acknowledging that

they exist. This can help us to remain more objective and less emotional when

considering what (if anything) should be done to adjust our portfolios in this

time of uncertainty.

How to I reach my Financial Advisor and support team? The best way to reach your Financial Advisor or a Support Staff member is via e-mail while they are working remotely from their individual home offices. However, you can call our main phone at 610-868-9000 and leave a voice mail message. All voice mail messages are converted to recordings and immediately sent via email to the recipient. Please leave a detailed message, including the best number to return the call, and someone from your team will get back to you as soon as possible. If you don’t know the direct e-mail or phone number you are trying to reach, you can send us a note at FromOurTeam@valleynationalgroup.com and your message will be routed to the appropriate person on your behalf.

What is the status of my tax return? Our team will continue to work on tax preparation over the next couple of months with the new July 15 deadline in mind. If your return is in process and you wish to check the status, e-mail us at tax@valleynationalgroup.com.

If you still need to get us your documents, please upload digital copies to your secure eVault Client Portal. If you need to set up a personal portal, please contact us and your service team will help you. If you are unable to submit documents digitally, please hold them at home – do not mail to us. If you already have documents on the way, we have made arrangements to procure that mail for safe keeping until we can revisit normal physical operations.

How do I get paper documents/checks to VNFA if you’re closed? Currently, VNFA is receiving all regular and overnight mail deliveries. However, due to a possible lag in delivery time, it is better to send documents electronically (ideally via your secure eVault Client Portal – alternatively by fax and e-mail for documents that do not contain sensitive personal data).

We encourage you to use electronic

transfers such as an existing moneylink, but checks can be received via regular

or overnight mail delivery. If you are unsure of the best method in your

particular situation, please give us a call so that we can guide you to a

solution.

Will normal business hours continue or be adjusted? Our team will continue to be at your service Monday through Friday from 8 a.m. to 4 p.m., as usual. Please understand that there may be a slight delay in the delivery and return of your messages as working remotely with our team and our service providers sometimes requires a few extra steps to ensure clarity and security.

Where do I find the latest news and insights available from VNFA in between The Weekly Commentary e-mails? We have established a special landing page to collect our resources related to our clients’ interests and needs during the COVID-19 pandemic. The page is available from the banner on our home page or directly at valleynationalgroup.com/COVID-19-resources If you have a question or a specific topic you would like us to address, please submit your inquiry to us at FromOurTeam@valleynationalgroup.com.

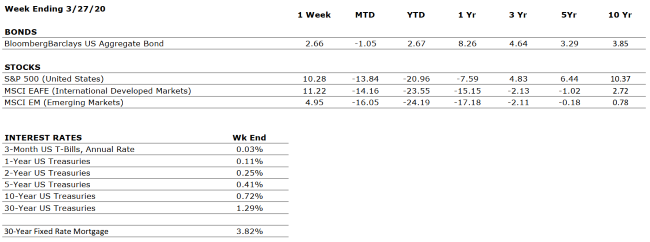

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEGATIVE

The consumer has been the bedrock of the US economy through much of the current expansion, and remains in a strong position. However, we have further reduced our grade to NEGATIVE as a result of the unprecedented social distancing and quarantining efforts currently being employed to fight the spread of COVID-19.

CORPORATE EARNINGS

NEGATIVE

Coming into the year, analysts were expecting mid to single digit earnings growth, but the spread of COVID-19 is likely to have a substantial impact on near-term earnings forecasts. However, earnings could bounce back quickly once the pandemic has run its course.

EMPLOYMENT

NEGATIVE

We have downgraded our employment grade another level as we expect the next few weeks will reveal significant job losses due to the suspension of economic activity in the services industry to combat the spread of COVID-19.

INFLATION

POSITIVE

Inflation is often a sign of “tightening” in the economy and can be a signal that growth is peaking. The deflationary environment created by COVID-19 should provide additional room for robust stimulus from both fiscal and monetary policy initiatives.

FISCAL POLICY

VERY POSITIVE

The CARES Act provides approximately $2.2 trillion of support for businesses and families that are impacted by the economic fallout of the COVID-19 pandemic. This is by far the largest fiscal stimulus package ever passed, and we anticipate the possibility of additional support once we emerge on the other side of the “curve”.

MONETARY POLICY

VERY POSITIVE

In response to the threat of COVID-19, the Federal Reserve has implemented two emergency rate cuts and has moved its target interest rate back to zero. Additionally, it has announced its intention to conduct further asset purchases to support markets. We believe that the Fed is doing all it can to support the economy and markets.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

VERY NEGATIVE

With COVID-19 being declared a global pandemic, our geopolitical risks rating is VERY NEGATIVE. However, we think it is important for investors to disentangle the public health concerns over the near-term from the expectations for markets over the long-term. The pandemic remains a near-term issue at this time.

ECONOMIC RISKS

VERY NEGATIVE

As discussed in our commentary, COVID-19 represents a real threat to economic activity globally. However, we do expect that the eventual economic recovery will occur more swiftly than from previous economic shocks.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Laurie will be collecting questions to address at a future date – stay tuned for more information in April.

Live episodes of “Your Financial Choices” are postponed until further notice as Laurie and her guests are working from home in response to guidance around the COVID-19 pandemic.

WDIY will continue to broadcast

prerecorded local shows as well as available NPR programming. Please continue

to support local radio!