by Connor Darrell CFA, Assistant Vice President – Head of Investments

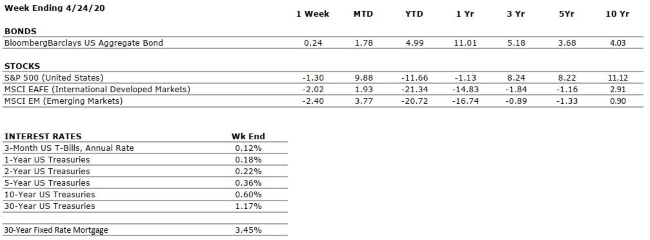

Most global equity markets moved modestly lower last week as updated manufacturing data came in at record low levels and an additional 4.4 million Americans filed for unemployment insurance. In the past five weeks, over 26 million people have filed for unemployment benefits, which represents about 16% of the U.S. labor force. Furthermore, the supply and demand imbalances that the global shutdown has created in the economy have been enormous, particularly in some commodity markets. Global stay-at-home orders have evaporated the demand for oil, and storage facilities are nearing full capacity. On Monday afternoon, oil prices turned negative for the first time in history as traders were forced to pay counterparties to take barrels off their hands as storage costs skyrocketed. Prices stabilized a bit as the week progressed, but many investors have understandably been asking how such price fluctuations could be possible. The intricacies of the oil markets are quite complex, but the core of the issue is the imbalance between supply and demand, combined with only limited storage capacity in the supply chain. As oil has continued to be pulled from the ground despite limited demand for the final product, storage facilities have approached full capacity. Oil contracts between buyers and sellers settle with physical delivery of the product, and buyers must pay for the storage. But with storage facilities at full capacity, these costs have skyrocketed.

Despite the eye-catching economic data and significant dislocations in commodities prices, equity markets have recovered strongly from their March lows as a result of rising optimism surrounding the reopening of global economies. However, any such reopening must be implemented carefully and in multiple stages. We expect this to be a long process, with additional bouts of market volatility along the way. The resumption of “normalized” economic activity will not occur at the “flip of a switch,” as it will also require a recovery of confidence within society, which will take time. Thus, the ultimate economic recovery will likely not be fully achievable without a solution from the medical community (via vaccine or effective therapeutic). Most credible sources seem to suggest that such a solution is more likely to arrive in 2021 than in 2020, setting the stage for a potentially longer event than some optimists seem to anticipate. However, we continue to remind investors that while its effects may be with us for another year or more, the COVID-19 pandemic will be transitory in nature. As long-term investors, it is important to remain focused on the temporary nature of these challenges and remember that the long-term earnings power of markets will remain intact.