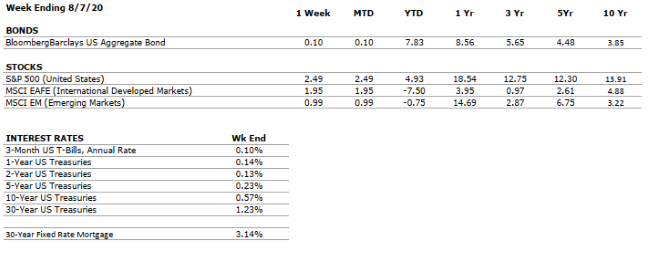

by Maurice (Mo) Spolan, Investment Research Analyst U.S., international and emerging market equities were all up between 1% and 3% last week. Fixed income indices, such as the widely followed Barclay’s Aggregate, have provided returns only slightly above zero over the last month, a result of the historically low rate environment in which investors are participating.

The U.S. added about 1.2 million jobs in July, a considerable deceleration from the 4.8 million added during June. While employment gains are certainly welcomed amidst a global pandemic, the slowdown may indicate the unfortunate possibility that new job growth is plateauing. This is troublesome because the unemployment rate remains very high, at 10.2%.

With Q2 corporate earnings almost complete, S&P 500 constituents have experienced an aggregate decline in earnings of 33%, the greatest year-over-year stumble since 2008. With that said, analysts expected earnings to erode by 40%, so companies have beaten expectations.

As Democrats and Republicans remain distant in their proposed stimulus packages, President Trump signed an executive order over the weekend to provide fiscal support. Whether the order will actually come into effect, however, is uncertain, as several legal analysts believe that it is unconstitutional for the president to supersede congressional spending authority.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEGATIVE

GDP declined at an annualized rate of 32.9% in Q2, the fourth-largest fall in the last 100 years. Although the figure is staggering, it was in-line with economists’ expectations.

CORPORATE EARNINGS

VERY NEGATIVE

S&P 500 earnings have fallen by around 33% in Q2, the sharpest year-over-year decline since 2008.

EMPLOYMENT

VERY NEGATIVE

1.8 million jobs were added in the U.S. during July. While gains, rather than losses, are welcomed, the figure represents a considerable deceleration from the 4.8 million jobs added in June. Unemployment remains very high at 10.2%.

INFLATION

POSITIVE

The deflationary environment created by COVID-19 should provide additional room for robust stimulus from both fiscal and monetary policy initiatives. However, we will be watching closely in the intermediate term for second and third order effects leading to a return of inflationary pressure.

FISCAL POLICY

VERY POSITIVE

In light of the expiration of federally granted, weekly unemployment support, and an absence of congressional progress towards the next round of stimulus, President Trump signed an executive order over the weekend provisioning fiscal support. However, the legality of the order, and whether it will actually come into effect, are in question.

MONETARY POLICY

VERY POSITIVE

The Federal Reserve has supported asset markets with unprecedented speed and magnitude in response to COVID-19.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

VERY NEGATIVE

The relationship between the US and China, the world’s two largest economies, was already weakened by the trade war but has deteriorated further as a result of COVID-19.

ECONOMIC RISKS

VERY NEGATIVE

The impacts from COVID-19 were as swift and pronounced as any shock in modern times. Robust monetary and fiscal stimulus stabilized the system, and several measures of the economy improved in May and June. However, economic activity remains well-below that in 2019, and uncertainty remains very high.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

REMINDER – The Internal Revenue Service is allowing taxpayers who have taken a

2020 Required Minimum Distribution (RMD,) which includes beneficiaries, to

repay that amount back to their retirement account(s) by August 31. For

taxpayers who took more than the RMD, only the RMD portion would be allowed to

be repaid unless a 60-day rollover would otherwise be available. If you

took an RMD and wish to return some or all of it, please contact your financial

advisor.

Laurie will be joined by Carrie Ward, Realtor,CIPS, TRC, MRP, RENE with Howard Hanna The Frederick Group to discuss real estate in the valley – overview and tips.

They can take your questions live on the air at 610-758-8810, or address those submitted via yourfinancialchoices.com.