Please join us this evening at 5 p.m. for the Virtual Volunteer Challenge celebration. The free, live event is the capstone to the 2020 Volunteer Challenge and a fundraiser for the Volunteer Center of the Lehigh Valley. Registration is still available: https://www.volunteerlv.org/volunteer-challenge

Team VNFA is in the running to win

one of the top-voted projects for our work with Northeast Community Center. We

thank you for your support throughout the project to help us make a difference

in our community.

Voting will close before the end of the virtual event today: https://www.volunteerlv.org/poll-organizations

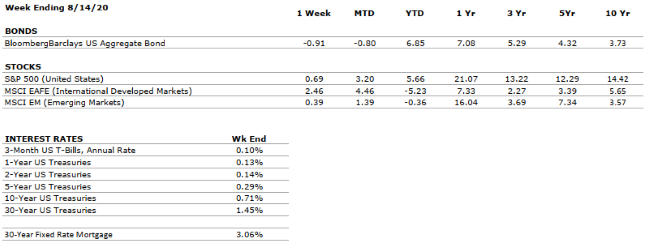

by Maurice (Mo) Spolan, Investment Research Analyst The S&P 500 was up 0.7% last week, as the index now rests less than 1% below its February all-time highs. The Barclay’s Aggregate Bond Index, by contrast, was down 0.9% as interest rates rose (bond prices decline when rates increase).

The headline economic figures of the week

pertained to consumer spending, jobs and inflation. Retail sales increased 1.2%

in July, a sharp deceleration from June’s 7.5% gain, but still a healthy figure

in the midst of a pandemic. On the jobs front, unemployment claims fell below 1

million for the first time since March, an indication that Americans are

returning to work. Last, inflation jumped 0.6%, the largest one-month increase

since 1991. However, CPI is running at a moderate annualized pace of 1.6%,

below the Fed’s 2% target, and more sustained hints of inflation will be

required before the central bank adjusts its highly-stimulative stance.

As the presidential election looms less

than three months away, Joe Biden made news by selecting Kamala Harris as his

running mate. The Wall Street Journal reports that traders are bracing for a

choppy finish to the year, as market volatility has historically been above

average during election seasons. Also, in the political sphere, Congress broke

for summer recess without passing another round of stimulus. While President

Trump hopes to provide support by way of executive order, the constitutionality

of his plan remains in question. The economy, particularly the consumer, is

likely to suffer if no further fiscal stimulus is delivered.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEGATIVE

GDP declined at an annualized rate of 32.9% in Q2, the fourth-largest fall in the last 100 years. Although the figure is staggering, it was in-line with economists’ expectations. Retail sales increased 1.2% in July; a healthy mid-pandemic result, but sharply below June’s 7.5% rise.

CORPORATE EARNINGS

VERY NEGATIVE

S&P 500 earnings have fallen by around 33% in Q2, the sharpest year-over-year decline since 2008.

EMPLOYMENT

VERY NEGATIVE

1.8 million jobs were added in the U.S. during July. While gains, rather than losses, are welcomed, the figure represents a considerable deceleration from the 4.8 million jobs added in June. Unemployment remains very high at 10.2%.

INFLATION

POSITIVE

Core inflation increased 0.6% in July, the largest one-month jump since 1991. However, on an annualized basis, CPI is running at a moderate 1.6%, below the Fed’s 2% target. More sustained indications of inflation will be necessary before the central bank curbs its uber-stimulative policies.

FISCAL POLICY

VERY POSITIVE

In light of the expiration of federally granted, weekly unemployment support, and an absence of congressional progress towards the next round of stimulus, President Trump signed an executive order provisioning fiscal support. However, the legality of the order, and whether it will actually come into effect, are in question.

MONETARY POLICY

VERY POSITIVE

The Federal Reserve has supported asset markets with unprecedented speed and magnitude in response to COVID-19.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

VERY NEGATIVE

The relationship between the US and China, the world’s two largest economies, was already weakened by the trade war but has deteriorated further as a result of COVID-19.

ECONOMIC RISKS

VERY NEGATIVE

The impacts from COVID-19 were as swift and pronounced as any shock in modern times. Robust monetary and fiscal stimulus stabilized the system, however, economic activity remains well-below that in 2019, and uncertainty remains very high.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Important reminder regarding estimated income tax payments: Many taxpayers benefited from the delay in filing due dates for 2019 tax payments and 2020 estimated tax payments. For those who received their tax returns and estimate vouchers prior to the payment extension, please review your records to make sure that you made any first and second quarter payments by the July 15 extended payment date. (Some states had earlier due dates.) The remaining estimates are still due at the normally scheduled dates of September 15, 2020 and January 15, 2021.