You

will be receiving an initial e-mail or mailed packet this week with

instructions to complete our 2020 Tax Questionnaire and other related forms, as

needed for your specific situation. Please complete these steps at your

earliest convenience and send us your supporting tax-related documents once you

have all or most of what you expect collected.

For

the safety of our employees and our clients, our team continues to work

remotely, so please call ahead to schedule an appointment if you have a need to

visit our office to drop off or pick up documents.

If

you have questions at any time, you may ask to speak with our Tax Department at

610-868-9000 or e-mail the team directly at tax@valleynationalgroup.com.

1099 Tax Reminders Once again, it is the time of year to think about your filing requirements as a small business owner, self-employed individual, or owner of rental property. If you operate for gain or profit, the IRS considers you to be engaged in a trade or business and therefore required to file certain information returns. Information related specifically to the Form 1099-MISC, Miscellaneous Income, and the newly re-introduced Form 1099-NEC, Nonemployee Compensation, can be found at irs.gov/instructions/i1099msc.

Form

1099-NEC is due on or before February 1, 2021, using either paper or electronic

filing procedures.

File

Form 1099-MISC by March 1, 2021, if you file on paper, or March 31, 2021, if

you file electronically.

The IRS operates a centralized call site to answer questions about reporting on Form 1099 and other information returns. If you have questions related to reporting on information returns, the IRS centralized call site can be reached at 866-455-7438. In addition, please feel free to contact our VNFA Tax Department at tax@valleynationalgroup.com or 610-868-9000.

View/Download PDF version of Q4 Commentary (or read text below) Equities In an eventful Q4, the stock market performed very well, as the S&P 500, Nasdaq 100, and Dow Jones Industrial Average were up 12.15%, 13.09%, and 10.73%, respectively. News was largely supportive of stocks this quarter, as a clear Presidential winner was announced, multiple vaccines entered distribution and a second fiscal relief bill was passed. On a full-year basis, the Nasdaq 100, which is populated mostly by technology companies, delivered a nearly 49% return, its best year since 2009, while the bellwether S&P 500 Index gained 18.4% and the “seasoned economy” Dow increased almost 10%. International and Emerging Market stocks also had strongly positive performance this year.

2020 was astonishing in that both the stock market and the economy (as measured by GDP) experienced their most rapid declines and corresponding recoveries in history. In response to lockdowns – which portended a nearly totally dormant nation – the Federal Reserve acted swiftly and vociferously by lowering interest rates and buying treasury bonds, thereby injecting much needed liquidity into a frightened financial market. Also buoyed by a large fiscal stimulus bill in March, the markets recovered as it became clear that COVID’s negative economic impacts would be mostly transient.

Fixed Income Interest rates collapsed to nearly zero in 2020 as a result of central bank action and investor flight to safe haven assets. Indeed, the 10-year treasury bond touched a historical nadir of 0.52% on August 4, down from 1.88% at the start of 2020. The 10-year treasury – a good proxy for the holistic interest rate environment – spent much of the year close to 0.70% and sits today just above 0.90%. Bond prices rise when interest rates fall, so investors experienced capital gains in their fixed income holdings. However, likely the most important impact that the rate decline had was on stocks, as investors passed on paltry bond yields in favor of equity investments.

Outlook The economic fundamentals heading into 2021 are firmly optimistic: several vaccines are entering distribution, a second fiscal bill will have positive impacts, and yet, interest rates remain in the basement (which is both stimulative to the real economy and to stocks). The question, however, is to what extent such fundamentals are already reflected in asset prices after such a robust market recovery beginning on March 23. Another salient question on the mind of investors is to what degree trends which strengthened during the pandemic – such as e-commerce, food delivery and teleconferencing – will persist, or give way to “the old way” of doing things. We expect healthy economic performance as the American population gets inoculated through the year and, as always, will be following the markets closely and adjusting our views as fit.

by William Henderson, Vice President / Head of Investments

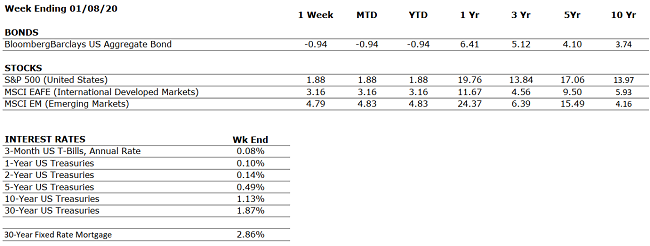

The first week of trading in 2021 continued the market rally we

saw for a good portion of 2020. For the week, the Dow Jones Industrial

Average returned +1.61%, the S&P 500 Index +1.83% and the NASDAQ +

2.43%. Technology and “green” stocks continued to do very well as the

realization that a Biden administration bolstered by a Democrat-controlled U.S.

Congress will push green energy, improved technology, and eventually infrastructure.

Last week saw events in Washington DC that sadly shocked the

world. Protesters stormed the U.S. Capitol building and temporarily shut

down the activities of Congress. Perhaps Americans wrongly assumed that

protests, riots, and general unrest was over with the U.S. Presidential

Election finally behind us, but this was not the case. Political

uncertainly continues to pose risks to the markets and is difficult to predict

and quantify. For example, as noted above, the technology sector is poised

to grow much stronger than the overall economy, but we are seeing politics

impact social media companies like Twitter, Facebook and Parler as some sites

banned President Trump from use. What will the outcome and impact be on those

companies is yet to be played out, but it creates, and unknown risk and markets

hate unknown risks. Arguments will abound about whether social media

companies are broadcast companies, news outlets, utilities or just fun pastimes

and what, if any, regulations should be imposed on their actions. The

argument that social media companies are utilities is specious at best, as you

can live without Twitter but not without water, electricity or even a

phone. But our U.S. Congress has reign to do many things, all of which create

risks and unknowns.

The U.S. Federal Reserve continues to be the one core bedrock of

the economic recovery with a firm position by Fed Chair Jerome Powell to keep

interest rates low for as long as necessary. The Fed Funds Rate, the interest

rate that banks charge other banks for lending excess cash, remains near zero,

while the 10-year U.S. Treasury Note moved a few basis points higher last week

and now stands at 1.11%. Finally, there is steepness in the yield

curve. Banks make money when the yield curve is steep – they borrow low

and lend high. This week, we will see the first of the large banks

reporting fourth quarter earnings – JP Morgan Chase, PNC Bank and Wells Fargo,

among others, are all slated to report by week’s end.

Headwinds exist today from the COVID-19 pandemic and serious

political unrest. Tailwinds also exist with investments in technology, green

energy and infrastructure and a willing Fed to keep the pump primed for

economic expansion. Lastly, a pent-up consumer is sitting on the sidelines

waiting for a vaccine and an “all clear” sign for leisure activities to open up

again.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

GDP increased at a 33.1% annualized pace in Q3. The U.S. economy has now recovered about 2/3 of its output lost to the COVID-19 pandemic.

CORPORATE EARNINGS

NEUTRAL

In Q3, S&P 500 earnings were down 7-8% from the year-ago period. This compares to Q2 2020, in which S&P 500 earnings were down by 1/3 from the comparable 2019 quarter. Companies will begin reporting Q4 earnings in the coming weeks.

EMPLOYMENT

NEGATIVE

The unemployment rate was stagnant in December at 6.7%. This is the first month since April in which the unemployment rate did not improve.

INFLATION

POSITIVE

The Fed plans to allow inflation to temporarily overshoot its 2% target such that the long-term average is 2%. Inflation has been tame since the Great Financial Crisis, less than 2%.

FISCAL POLICY

POSITIVE

Congress passed its second major fiscal relief package of 2020, the most recent one amounting to $900 billion in stimulus. The bill currently provides for $600 in cash payments to American citizens, however, Congress is in negotiation to deliver an additional check for up to $2,000, as President Trump has requested.

MONETARY POLICY

VERY POSITIVE

The Federal Reserve supported asset markets with unprecedented speed and magnitude in response to COVID-19.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

There are few, if any, looming geopolitical risks that could upset the economic recovery.

ECONOMIC RISKS

NEUTRAL

Although economic activity mostly remains below 2019’s levels, improvement has occurred across nearly every measure since the April nadir. With multiple vaccines in distribution, a second fiscal package in place, and interest rates low, 2021 is positioning to be a strong economic year.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in Wednesday, 6 PM for “Your Financial Choices” show on WDIY 88.1FM: Laurie Siebert, CPA, CFP®, AEP® and her guests from Valley National Financial Advisors, Timothy G. Roof, CFP and William Henderson, Head of Investments, will discuss:A market recap of 2020 and 2021 expectations.

This show was postponed from last week due to the urgent live news being broadcast by NPR on 1/6/21.

Laurie and her guests can take your questions live on the air at 610-758-8810, or address those submitted via yourfinancialchoices.com. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.