Our team will be working normal hours this Friday, April 2. Happy Easter to all who celebrate this weekend.

Daily Archives: March 30, 2021

Current Market Observations

by Maurice (Mo) Spolan, Investment Research Analyst

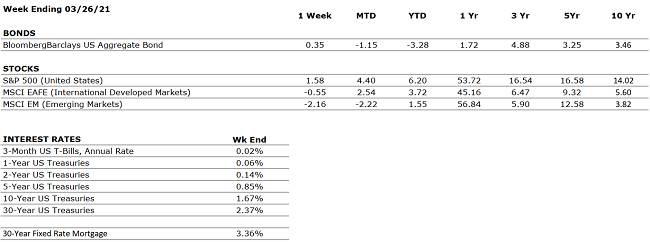

The S&P 500 and Dow Jones Industrial Average were both up modestly last week, 1.6% and 1.4% respectively, while the tech-heavy Nasdaq 100 was flat and International and Emerging Market equities trended lower. Bond prices rose as interest rates declined slightly; interest rates have risen quite a bit in 2021 but remain very low from a historical perspective. The 10-year U.S. Treasury note ended the week at 1.66%.

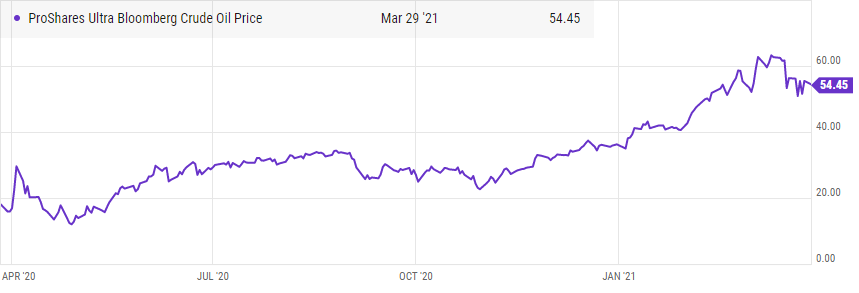

The blockage in the Suez Canal is disrupting as much as 12% of global trade. This supply constraint has also facilitated a rise in the price of oil, which is now above $61. Oil prices have recovered considerably since the pandemic’s outset and may settle at this higher level as demand for travel accelerates upon reopening throughout 2021. The giant container ship bocking the Suez Canal seems to have finally been cleared but the impact to the global supply chain is unclear.

President Biden is increasing his vaccination target, up to 200 million doses administered in his first 100 days in office, from an initial goal of 100 million. Estimates show that 14% of Americans are fully inoculated and 26% of residents have received at least one dose.

The economic outlook remains extremely favorable as both monetary and fiscal stimulus are highly accommodative, and the vaccine roll-out accelerates. As pent-up demand is unleashed, 2021 may end up being one of the most lucrative years in American economic history.

The Numbers & “Heat Map”

THE NUMBERS

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

|

US ECONOMY |

||

|

CONSUMER HEALTH |

POSITIVE |

The FOMC forecasts the U.S. economy will grow by 6.5% in 2021, while the unemployment rate will retreat to 4.5% by year’s end. |

|

CORPORATE EARNINGS |

POSITIVE |

S&P 500 Q4 profits grew 3.8% year-over-year, well in excess of analyst expectations, which figured that earnings would fall by 7%. Earnings in 2021 are set to look strong as they lap Q2-Q3 2020. |

|

EMPLOYMENT |

NEUTRAL |

The unemployment rate declined to 6.2% in February from 6.4% in January. Most of the added jobs last month were concentrated in the Leisure & Travel sector. Total employment remains 9.5 million jobs below the pre-pandemic peak. |

|

INFLATION |

POSITIVE |

The Fed plans to allow inflation to temporarily overshoot its 2% target such that the long-term average is 2%. Inflation has been tame since the Great Financial Crisis, less than 2%. |

|

FISCAL POLICY |

POSITIVE |

President Biden signed a $1.9 trillion fiscal bill last week. The U.S. economy has received a total of approximately $4 trillion in stimulus during the COVID-19 pandemic. |

|

MONETARY POLICY |

VERY POSITIVE |

The Federal Reserve continues to indicate that the monetary environment will remain very accommodative for the foreseeable future. |

|

GLOBAL CONSIDERATIONS |

||

|

GEOPOLITICAL RISKS |

NEUTRAL |

There are few, if any, looming geopolitical risks that could upset the economic recovery. |

|

ECONOMIC RISKS |

NEUTRAL |

Although economic activity mostly remains below 2019’s levels, improvement has occurred across nearly every measure since the April 2020 nadir. With multiple vaccines in distribution, a second fiscal package in place, and interest rates low, 2021 is positioning to be a strong economic year. |

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Quote of the Week

“Patience is the calm acceptance that things can happen in a different order than the one you have in mind.” – David G. Allen

“Your Financial Choices”

Tune in Wednesday, 6 PM for “Your Financial Choices” show on WDIY 88.1FM: Updates on Stimulus, filing dates and amendments

Laurie can take your questions live on the air at 610-758-8810, or address those submitted via yourfinancialchoices.com. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.