The American Rescue Plan includes a significant overhaul of

the child tax credit, but only for the 2021 tax year. The IRS and Treasury

created a website for taxpayers to opt out of receiving advance payments, or to

provide information on status changes that would impact the amount of the

credit at https://www.irs.gov/credits-deductions/child-tax-credit-update-portal

Our VNFA Tax Department sent out personalized recommendations

to clients who may be affected last week. Please look for an e-mail from tax@valleynationalgroup.com, or

reach out to us with any questions.

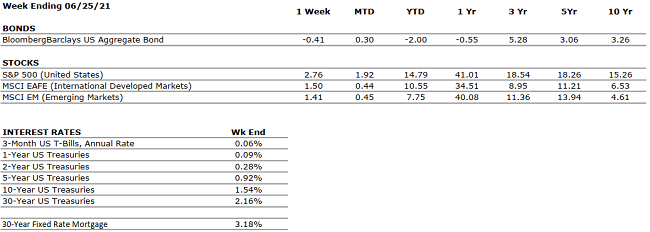

by William Henderson, Vice President / Head of Investments Last week the markets showed conditions remain favorable for equities as easy financial conditions and a healthy economic recovery are firmly in place for the foreseeable future. All three major indices posted strong weekly returns adding to their very healthy year-to-date gains. The Dow Jones Industrial Average rose by +3.4% last week, the S&P 500 Index rose +2.7% and the NASDAQ increased by +2.4%. The “value-over-growth” trade seems to have waned as the major indices have moved into relative parity on a year-to-date basis. Year-to-date, the Dow Jones Industrial Average has returned +13.6%, the S&P 500 Index +14.8% and the NASDAQ +11.8%. Bonds continue to be well bid with yields remaining stubbornly low. The 10-year U.S. Treasury dropped six basis points last week to end at 1.51%.

Three additional factors boosted

the markets. First, all 23 major U.S. banks including

J. P. Morgan Chase, Bank of America, and PNC Bank passed

the Federal Reserve’s annual stress tests, which are

designed to test the

resilience of large banks under severe global recessionary conditions. Second,

after several weeks of negotiation, President

Biden and a bipartisan group of senators announced an

agreement

on an infrastructure deal that could carve

out up to $1 trillion from

the $2.25 trillion American Jobs Plan that was released

in March 2021. The agreement focuses on traditional infrastructure such as

roads and bridges as well as water infrastructure and broadband internet access. The

deal is a positive development because it comes with no

new taxes and instead is funded

by hodgepodge of revenue sources including repurposing

unused pandemic relief funds, tougher Internal Revenue Service tax collection,

and selling oil from the Strategic Petroleum Reserve. And

third, inflation fears are modestly abating as

supply chain pressures have eased and prices for

basic commodities, including metals and lumber, fell

from their recent spikes.

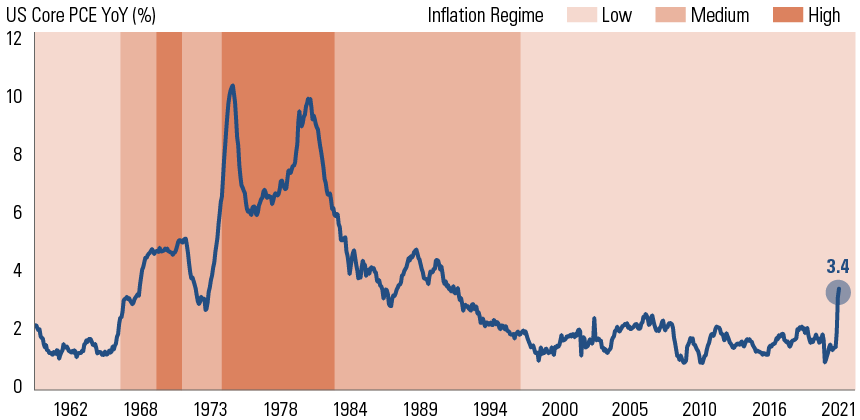

It is important to keep inflation

concerns in the proper perspective. The chart

below shows the long-term U.S. Core PCE (Personal

Consumption Expenditure) year-over-year percent

change. The recent jump in U.S. Core PCE

of +3.4%, is not that significant when you look at inflation over a much longer

term. The Fed’s goal of +2.0% average annual

inflation remains in place,

which means rates remain low for longer.

U.S. Core Personal

Consumption Expenditure (PCE)

(Source:

Bloomberg & Goldman Sachs June 2021)

As we move to close the second

quarter, corporate earnings announcements most

likely will surprise to the upside and revenue growth will remain robust. However,

companies may have to

deal with cost increases due to supply chain disruptions and

higher wages going forward. The economic tailwinds for the second half of

2021 will be consumer driven rather than stimulus driven.

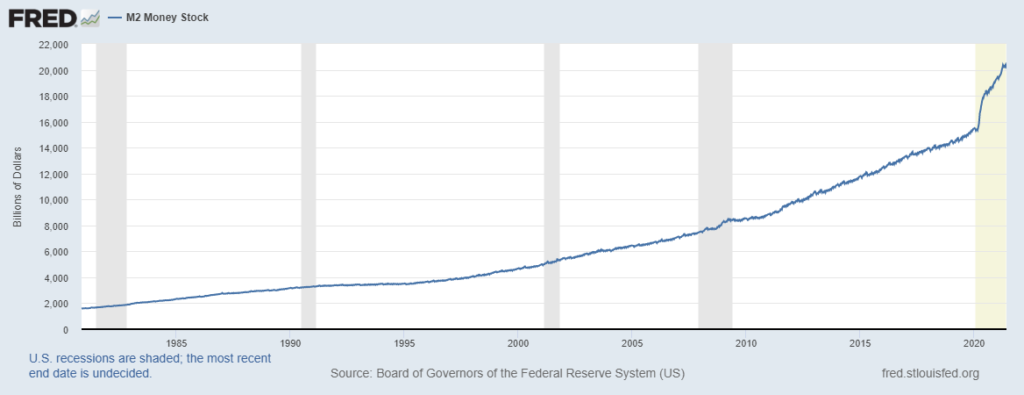

Consumers are in excellent

financial shape with personal savings accounts at record levels. According

to the Federal Reserve Bank of St. Louis, M2, the money supply measure that

includes cash, checking deposits and money market funds, reached $20.3 trillion

on June 22, 2021 (See chart above). There

is massive pent up demand

for travel and leisure; and with summer upon us, watch

for the consumer to fuel the economy and the Fed to keep the pump primed.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

The OECD forecasts that the global economy will grow 5.6% and 4.4% in 2021 and 2022, respectively.

CORPORATE EARNINGS

POSITIVE

S&P 500 Q1 sales and earnings growth were very strong. Corporate earnings are likely to remain strong throughout 2021 on a “year-over-year” basis as companies compare their results to depressed 2020 numbers.

EMPLOYMENT

POSITIVE

In May, the unemployment rate declined to 5.8%, from 6.1% in April.

INFLATION

NEUTRAL

Inflation was 4.5% in April. Inflation has generally been tame since the Great Financial Crisis, less than 2%; however, prices have been increasing in 2021 as a result of a tight labor market and supply chain constraints. The debate at-hand is whether recent inflation numbers are merely passing or here to stay.

FISCAL POLICY

POSITIVE

President Biden recently unveiled a stimulus package directed towards infrastructure that would total more than $2 trillion over eight years. President Biden is also considering a significant capital gains tax increase.

MONETARY POLICY

POSITIVE

The Federal Reserve indicated this week that it plans to hike rates twice in 2023. Previously, the Fed had suggested it would not raise rates until 2024. Nonetheless, the monetary stance is accommodative in the near future.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

There are few, if any, looming geopolitical risks that could upset the economic recovery.

ECONOMIC RISKS

NEUTRAL

With multiple vaccines in distribution and highly accommodative fiscal and monetary policies in place, 2021 may be one of the strongest economic years on record. If a risk is present, it may be that the economy will overheat, thereby leading to inflation and higher interest rates.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.