by William Henderson, Vice President / Head of Investments

While the markets closed the week with mixed returns, we saw a big move in technology stocks as the NASDAQ inched higher by nearly 2% versus a smaller move in the S&P 500 and a negative return for the Dow Jones Industrial Average. For the week that ended June 11, 2021, the Dow Jones Industrial Average lost -0.8%, the S&P 500 Index added just +0.4% while the NASDAQ jumped higher by +1.9%. Year-to-date returns on all three major indices remain comfortably in positive territory; especially given the NASDAQ’s recent run up which moves its returns more in line with the other broader indices for the full year. Year-to-date, the Dow Jones Industrial Average has returned +13.7%, the S&P 500 Index +13.8%, and the NASDAQ +9.5%. Bonds continued their move lower in yield last week with the 10-year U.S. Treasury Bond falling another 10 basis points to 1.46% from 1.56% the previous week. Strong inflation data, which we will talk more about below, has not budged the Fed’s ongoing zero interest rate policy, which seemingly keeps a lid on higher bond yields.

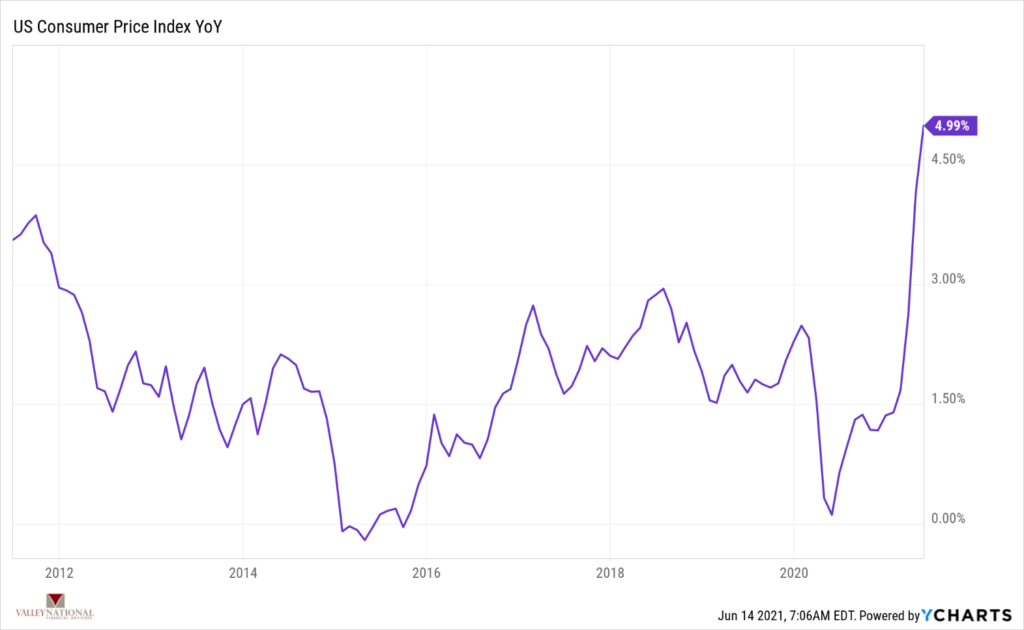

Last week, we saw inflation as measured by the consumer price index (CPI) rise 5.0% from a year ago. The core index, which excludes food and energy, rose 3.8%; the largest 12-month increase since 1992. (See chart below from YCharts of US Consumer Price Index YOY).

The Federal Reserve continues to view current inflationary trends as “transitory” or temporary and solely based on easy monetary and fiscal policies currently in place. Further, the price changes reflected in the recent jump in CPI were largely skewed to those sectors of the economy most impacted by the pandemic (e.g. travel & leisure and hospitality). See the price change examples below reported by the Federal Reserve Bank of St. Louis:

- Car Rental: 12.1% M/M May; 16.2% M/M April

- Airline fares: 7.0% M/M May; 10.2% M/M April

- Used Vehicles: 7.3% M/M May; 10.0% M/M April

The Fed views these significant moves in prices as transitory, relegated to a few “reopening” sectors and largely the result of recent stimulus checks sent to consumers in March 2021. As we have reported, and the Fed has confirmed, their long-term goal is for inflation to average 2.0%. Given that we have had many years of sub-2.0% inflation numbers, seeing inflation well above 2.0% (such as last week’s +5.0%) is just what the Fed has ordered for the economy.

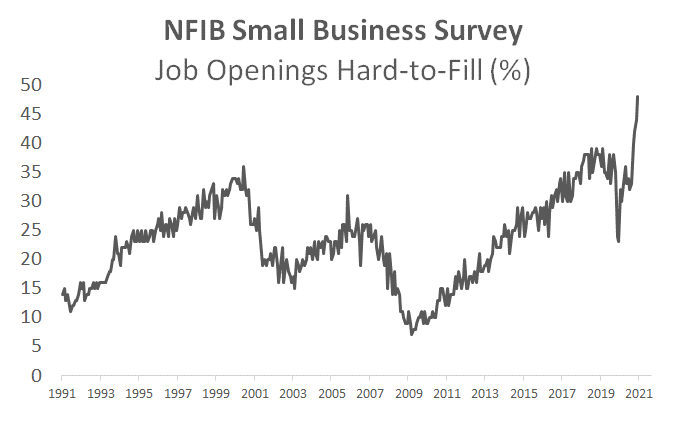

While the Fed is feigning obeisance around the inflation data, the consumer may be embedding fast-rising prices as something more than transitory. Also, some recent evidence of surveys from small businesses suggests that wage growth could be accelerating, which could increase the chance of sustained inflationary pressures as wages are harder to cut once in place. Last week, the “Job Openings Hard-to-Fill” component of the NFIB small business survey reached an all-time high (see chart below from Bloomberg). Jobs in leisure and hospitality are coming back but, with a higher compensation structure because employers are struggling to fill positions.

As noted above, both the equity and bond markets brushed off the inflation numbers released last week; and instead, are banking on the Fed and siding with the “transitory” story. The Fed remains committed to keeping rates lower for longer and thereby assuring we have a strong and sustained economic recovery on the heels of the pandemic recession of 2020. Investors, rarely more efficient than the market, just might be taking heed of the old Wall Street adage, “Don’t Fight the Fed.” We are certainly in that camp and believe long-term, diversified investors almost always win in the end.