We are pleased to

welcome Julie Clementi to our team as Back Office Associate. Julie will be part

of the operations team working in our Bethlehem headquarters. She will handle

paperwork and support service teams with internal account management processes.

Julie has more than eight years of banking and client service experience. She

holds her FINRA Series 6 and 63 licenses.

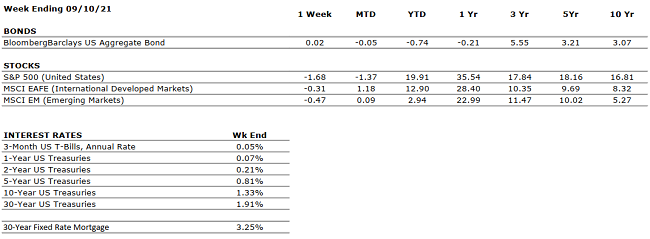

by William Henderson, Vice President / Head of Investments Markets ticked downward last week, and the S&P 500 notched its first five-day losing streak since mid-February. Last week, the Dow Jones Industrial Average lost -2.4%, the S&P 500 Index fell by -1.7% and the NASDAQ, following suit, fell by -1.4%. Modest losses for the week impacted year-to-date returns but returns remain strong for all three indexes. Year-to-date, the Dow Jones Industrial Average has returned +14.6%, the S&P 500 Index +19.9% and the NASDAQ +17.8%. We are seeing global growth concerns as the COVID-19 variant is delaying a stronger reopening of travel and leisure activities by consumers. U.S. Treasury Bonds. continue to offer safety and risk protection for investors and we consistently see a flight to safety when stock markets sell off. That said, last week the 10-year U.S. Treasury Bond fell three basis points to 1.33% from the previous week’s 1.36%. The current 1.33% on the 10-year U.S. Treasury is 41 basis points lower than the 1.74% yield level hit in March of this year when the markets were predicting a strong and steady opening of the economy and hints that the Fed was going to raise rates sooner rather than later. Those concerns have been muted as modest job reports and virus concerns continue to impact the economy. It is important to keep the big picture in perspective. The U.S. economy is growing at a pace that historically would be solid by any measure. Most economists are expecting third-quarter GDP growth nearing 4% and fourth-quarter GDP growth hitting 6% or stronger. These numbers are solid despite headwinds like rising gasoline prices, supply chain disruptions due to port closures, and the latest COVID-19 “wave” rolling through the country.

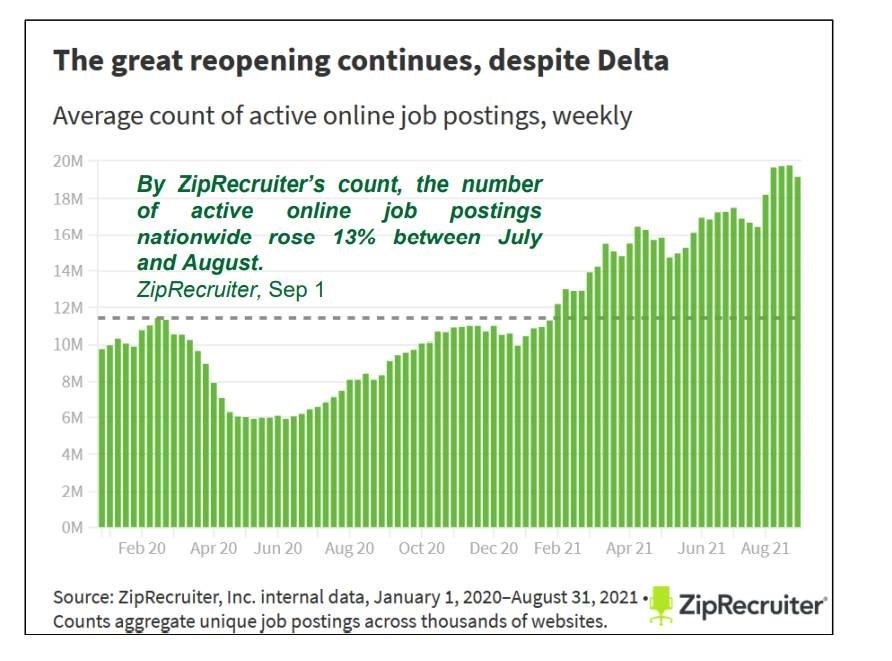

The chart below from

ZipRecruiter shows the number of active online job postings. Postings remain strong

and will stay that way as the unemployment continues to fall closer to the

Fed’s target of 4.5% from the current 5.2% (Bureau of Labor

Statistics).

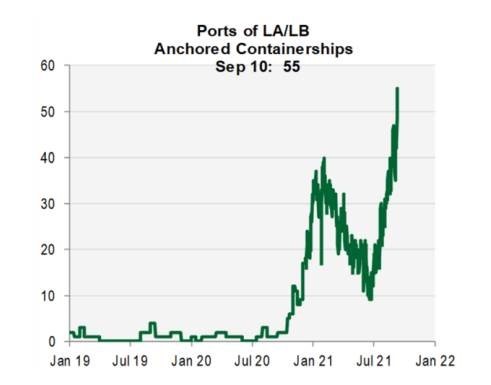

As noted above, there are headwinds impacting continued economic growth. First, supply chain disruptions are impacting corporate activity and logistical problems at U.S. ports are a major problem. See the chart below from Cornerstone Macro showing the number of anchored (meaning waiting to unload) containerships in the Ports of LA/LB.

Snagged ships and clogged ports

mean less freight moving and less economic activity.

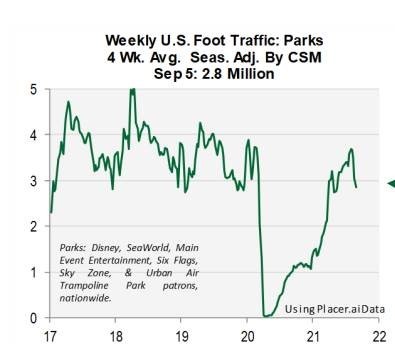

Second, the COVID-19 variants are modestly impacting consumer

activity. An interesting and telling chart below from Cornerstone Macro

shows weekly foot traffic at U.S. Parks (Disney, Six Flags, etc.) Foot traffic is certainly down from recent peaks but

that can also be attributed to the summer season ending and back to school

starting.

Certainly, concerns exist, and we are seeing markets reacting to these concerns as we did last week. But the economy remains healthy and strong. Critically important are corporate earnings and profits which rose 9.2% in the second quarter according to the Bureau of Economic Analysis (BEA). When corporations are growing and earnings are growing, they hire more employees. Consumer activity makes up the bulk of the U.S. economy. Pfizer is close to getting FDA approval for its COVID-19 vaccine for children aged 5-11. Throw in a cooperative Federal Reserve and we have the trifecta for continued economic recovery: healthy corporate activity leading to more jobs, wider distribution of the COVID-19 vaccine and low interest rates well into 2022. Stay focused on the bigger picture, avoid the noise, and remain committed to your long-term financial objectives.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

July retail sales declined 1.1% vs. June 2021 but are 15.8% higher than July 2020.

CORPORATE EARNINGS

POSITIVE

S&P 500 Q2 sales and earnings grew an astonishing 25% and 89%, respectively, when compared to the heavily depressed figures in Q2 2020.

EMPLOYMENT

POSITIVE

The unemployment rate is down to 5.2%. In August, new job creation was disappointing, but jobless claims were as low as they have been since March 2020.

INFLATION

NEUTRAL

Inflation remained at 5.4% year-over-year in July, the same reading as in June. Fed Chairman Jay Powell believes that the high inflation is transitory and will decelerate as global supply chain bottlenecks resolve.

FISCAL POLICY

POSITIVE

The Senate passed a $1 trillion infrastructure package. The bill is expected to be voted on by The House by the end of this year.

MONETARY POLICY

POSITIVE

The Federal Reserve has indicated that it does not plan to increase interest rates until 2023.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

Although the Taliban’s control in Afghanistan is concerning, it is unlikely to have a meaningful global economic impact.

ECONOMIC RISKS

NEUTRAL

2021 is shaping up as one of the strongest economic years on record. The primary risk at present is that of persistent inflation which begets higher interest rates.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Laurie can

address questions on the air that are submitted either in advance or during the

live show via yourfinancialchoices.com.

Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.