Team VNFA is pleased to support the WDIY

88.1 FM Fall Membership Drive for a fifth year. For every $100 WDIY

receives in donations, VNFA will fund 21 meals provided by Second

Harvest Food Bank of the Lehigh Valley and Northeast Pennsylvania to

individuals and families in our community. So far, 9,775 meals have been

pledged. Read more and donate at wdiy.org – WDIY

Partners with Second Harvest Food Bank During the 2021 Fall Membership Drive

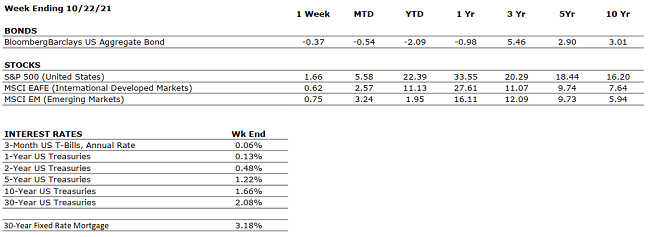

by William Henderson, Vice President / Head of Investments Equities notched yet another win last week with each of the major market indexes adding gains to already strong year-to-date returns. The Dow Jones Industrial Average rose +1.1%, the S&P 500 Index increased by +1.6% and the NASDAQ moved higher by +1.3%. Year-to-date, the Dow Jones Industrial Average has returned +18.3, the S&P 500 Index +22.4% and the NASDAQ +17.7%. Bond yields continued their slow rise recognizing that Fed tapering of bond purchases and higher short-term rates could happen sooner rather than later as the economic recovery from the pandemic continues in force. The 10-year U.S Treasury closed the week at 1.65%, up four basis points from the previous week and only slightly below the 1.74% level reached in March of this year.

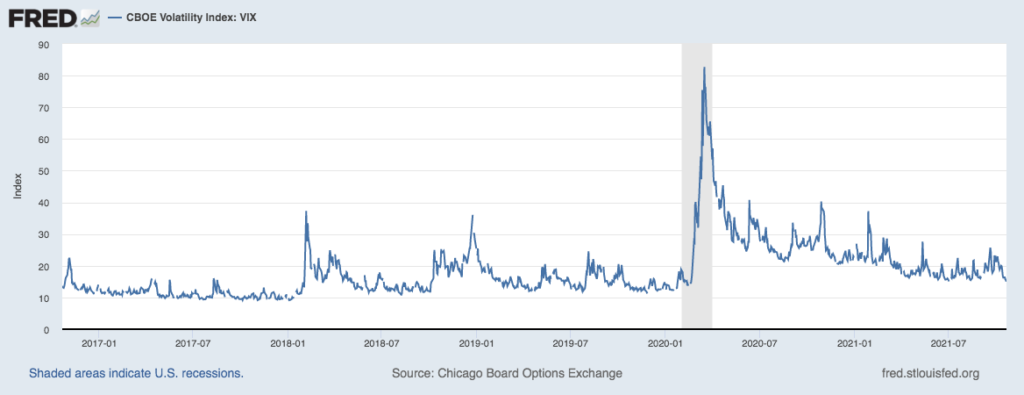

Comments from Federal Reserve Chair Jerome Powell late last Friday afternoon seemed to temper the bond market a bit. He stated that the U.S. Central Bank was on track to begin reducing asset purchases soon; however, he added that it is not yet time to raise interest rates because employment levels are still too low. Lastly, he added that inflation is likely to ease next year as pandemic-related pressures fade and supply chain disruptions settle. Powell’s comments cooled the bond market and helped to heat up the stock market and temper risk levels. The Chicago Board of Exchange Volatility Index (VIX) fell to its lowest level in more than four months. The VIX measures investors’ expectations of short-term market volatility. See the chart below of the VIX from the Federal Reserve Bank of St. Louis.

This week we will see two

important measures of the strength of the economic recovery: Continued 3rd quarter corporate earnings

releases and the U.S. government’s initial

estimate of third quarter GDP

growth. Earnings announcements thus far have bested Wall Street Analysts’ expectations

so watch for this pattern to continue, which would

bode well for the stock market. Conversely

a miss by a major technology firm would put negative pressure on

equity prices. The

third quarter GDP growth report will give us

a clearer picture of the negative impacts of the delta variant and oft talked

about supply chain disruptions. Recall the second quarter GDP

rose at a healthy 6.7% annual rate.

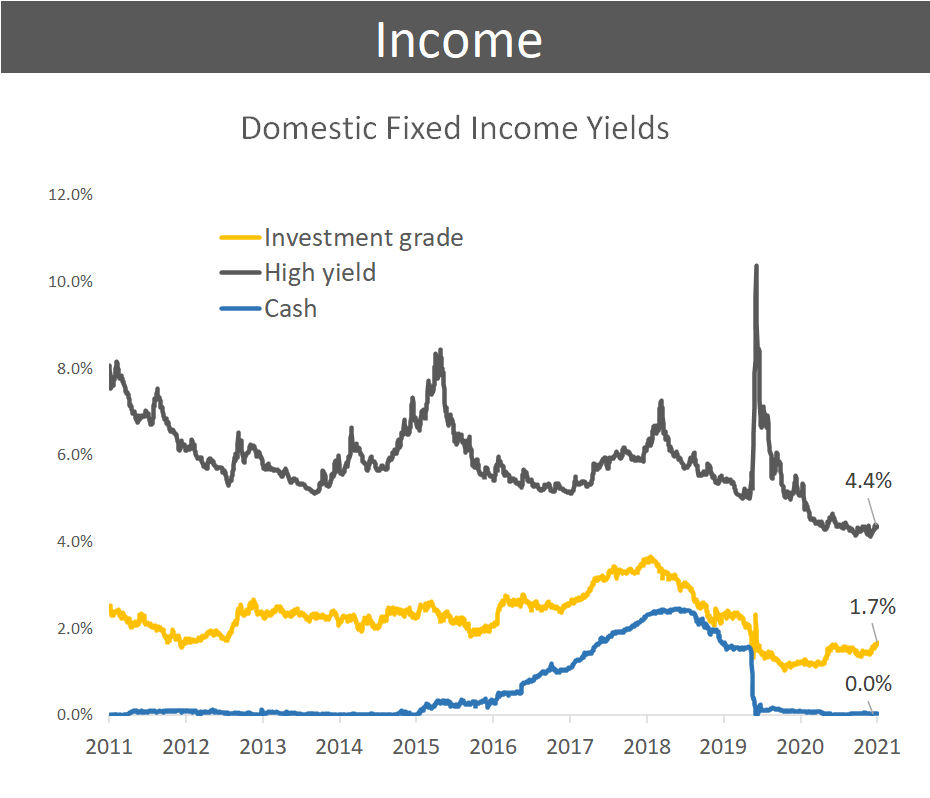

It is important to recognize that

as bond yields rise, their relative attractiveness as an investment also

rises. The 10-year U.S. Treasury at 1.65% yield offers

substantially higher returns than parking money in cash which is effectively

paying 0.00%. Further, while not offering

stellar yields, fixed income investments also provide ballast to a balanced

portfolio in times of market turmoil. See the chart below from Factset showing

Domestic Fixed Income Yields.

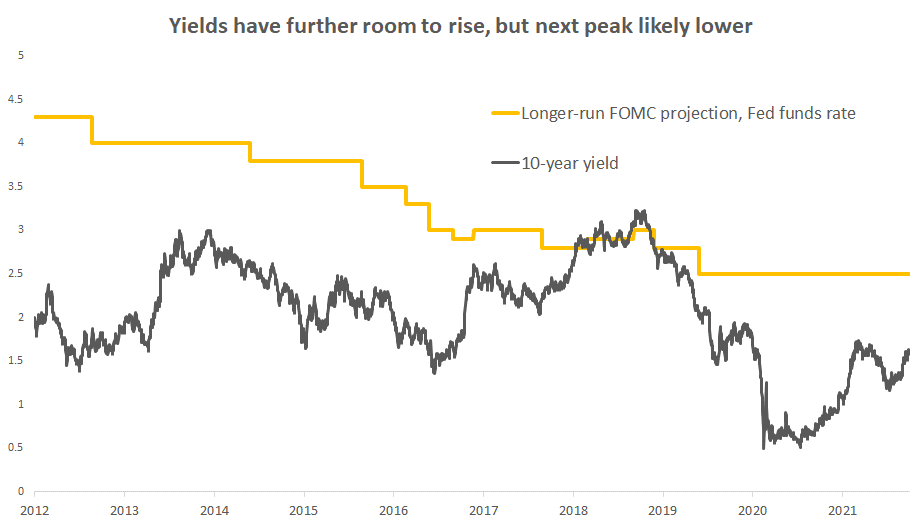

Certainly, rising bond yields are

generally bad news for bond prices because prices move inversely to yields. The

current projections for yields as predicted by the FOMC

(Federal Open Market Committee) shows

short-term rates peaking around 3.00% in this current cycle and the 10-year

U.S. Treasury peaking nearer to 2.50%. See

the chart below from Bloomberg showing Fed policymakers predictions for

short-term rates and the 10-year Treasury yield.

Recall also that while low by

historical standards, U.S. bond yields are higher than most developed countries

and there is still $11 trillion of negative-yielding debt globally. Global

demand for U.S. Treasuries will likely remain strong for some time which will

keep a virtual cover on a significant rise in domestic rates.

We

have pointed out for many weeks that the markets are indeed more efficient than

investors ever believe. This is witnessed by the fact that it continues to

climb the ever-present “Wall of Worries,” which

includes: COVID-19 variants, inflation, Fed Tapering, supply chain

disruptions and concerns about China. As

we move into the fourth quarter, the consumer, flush

with cash and sitting on a clean balance sheet will take over as the engine of

economic growth. Analysts are already predicting a stunning increase

of 15% or more in holiday spending this

season and remember, domestic consumption makes

up about 70% of the U.S. economy.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

September retail sales surprised to the upside, increasing 0.7% month-over-month (m/m) and 13.9% year-over-year (y/y). Economists expected September’s retail sales to decline slightly m/m.

CORPORATE EARNINGS

POSITIVE

With 23% of S&P 500 companies having reported Q3 results, sales and earnings are up 15% and 32%, respectively. However, company commentary suggests that the supply chain will be problematic in the coming quarters.

EMPLOYMENT

POSITIVE

The unemployment rate is down to 4.8%, as of September. The labor market is very tight at present, as many employers, particularly in the Leisure and Logistics sectors, are struggling to fully staff. The labor shortage is one of the causes of the global supply chain glut.

INFLATION

NEUTRAL

CPI rose 5.4% year-over-year in September, driven by the global supply chain backlog.

FISCAL POLICY

POSITIVE

A bill to lift the U.S. debt ceiling by $480 billion – which should provide enough headroom for government operations until December 3 – was passed.

MONETARY POLICY

POSITIVE

In recent communications, the Fed has indicated bond tapering may begin by the end of 2021 while rate hikes could commence by the end of 2022. Nonetheless, monetary policy remains relatively accommodative with rates at historical lows.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

Although the Taliban’s control in Afghanistan is concerning, it is unlikely to have a meaningful economic impact.

ECONOMIC RISKS

NEUTRAL

Supply chain disruptions are hampering the economy; however, demand remains very strong. The hold-ups appear primarily transitory and should ease progressively over time.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Stocks U.S. stocks were modestly down, between 1-2% in the case of each of the major indices, during Q3. Although Q2 corporate earnings (reported during Q3) were very strong, the positive results were already priced in, given that equity markets rose about 15% in the first half of 2021. Moreover, supply chain challenges were noted widely in company commentary, dampening the earnings outlook for Q3 and Q4. In the present environment, demand remains extremely strong – even in the face of the Delta Variant – but companies are struggling to meet said demand as labor and material shortages abound, while global logistics are obstructed by recurring covid outbreaks in Asia. Expectations are that consumer sentiment will remain very healthy for the foreseeable future, with the unemployment rate nearly back to long-run central bank targets, from as a high as 14.8% in April 2020, so the key determinant to corporate earnings over the coming periods is the health of the global supply environment.

Bonds The ten-year Treasury Bond ticked up a bit, from 1.44% to 1.48%, between the first and last days of the quarter; correspondingly, bond indices were basically flat in Q3. However, rate volatility tells a different story: the ten-year declined to as low as 1.19% in early August and peaked at 1.55% in late September. In turn, bonds performed negatively in the last month of Q3 as rates rose. Nonetheless, rates remain very low, that is, accommodative to economic growth, in the context of the long-term precedent, with the U.S. economy historically operating with a ten-year around 4-5%.

Inflation was high during the quarter, with CPI readings near 5%, because of the tight supply environment combined with booming consumer demand. Although economists and central bank personnel now believe inflation may be of greater permanence than previously considered, Q3 2021 could represent the inflation peak. Inflation was quite low following the Great Financial Crisis, so modestly higher and persistent price increases relative to pre-covid is not necessarily concerning. Fed Chairman, Jay Powell, indicates he will not be increasing rates until the end of 2022, and the probable future environment in which rates move higher, slowly and at a consistent pace, with inflation readings near 3%, is unlikely to be harmful to economic activity. Should inflation continue at clips near 5%, more rapid and material rate increases could be in order, which may present an obstacle to economic growth.

Outlook Looking forward to the next 6-18 months, the most important economic issue is the status of supply. As previously noted, supply challenges are primarily deriving from 1) sheer natural resource shortages, 2) labor shortages, 3) logistics congestion resulting from covid outbreaks. It is impossible to know with certainty when global supply will resume in a fully functional, normalized way, however, generally speaking, the global economy is extraordinarily good at allocating resources such that demand is fulfilled. It may take up to a couple years for supply to resolve itself fully, during which inflation may be elevated around 3%, but as mentioned, this scenario is not a bad one for economic health. Demand should remain strong, though the U.S. labor shortage is likely to persist, challenging employers. Finally, a fiscal infrastructure bill remains up for vote, providing additional demand stimulus if passed.

Tune in

Wednesday, 6 PM for “Your Financial Choices” with Laurie Siebert on WDIY

88.1FM. Laurie welcomes William Henderson, VP/Head of Investments for Valley

National Financial Advisors to discuss: Third Quarter Market Review & Investment Terms

Laurie can

address questions on the air that are submitted either in advance or during the

live show via yourfinancialchoices.com.

Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.

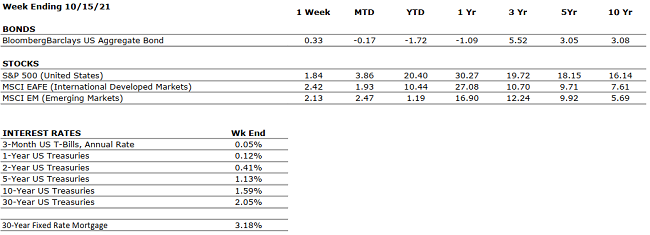

by William Henderson, Vice President / Head of Investments Last week seemed to be a tale of two markets. After starting the week off lower Monday and Tuesday, the markets came roaring back in a big way by week’s end after earnings announcements surprised to the upside and weekly unemployment claims declined much further than expected. Last week, the Dow Jones Industrial Average rose 1.6%, the S&P 500 Index increased by 1.8%, and the NASDAQ moved higher by 2.2%. Investors took advantage of the market’s 5% pullback in September and continued to pour money into equities. Last week’s rally added to an already strong year. Year-to-date, the Dow Jones Industrial Average has returned +17.0, the S&P 500 Index +20.4% and the NASDAQ +16.2%. Bond yields continued to rise as expectations of tapering of bond purchases by the Fed and higher short-term rates next year crept into fixed income traders’ plans. The 10-year U.S Treasury closed the week at 1.61%, 86 basis points higher than one year ago but still modestly below the March 2021 high of 1.74%.

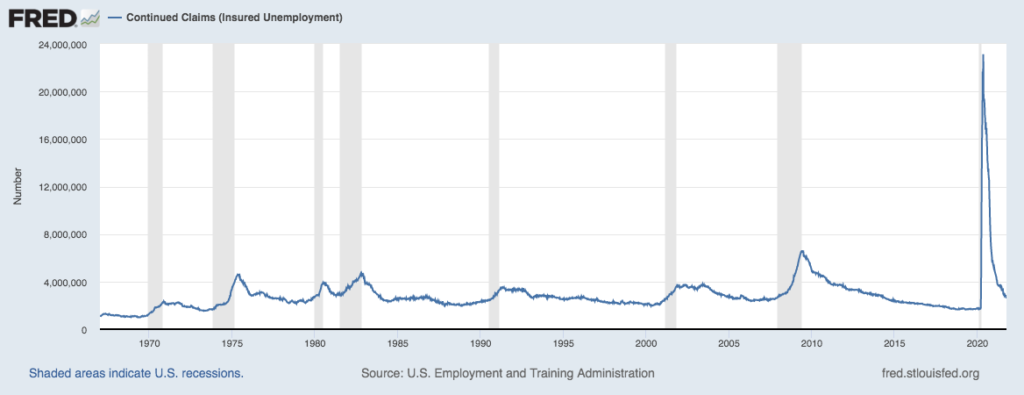

As mentioned, the economy and resultant earnings announcements continue to surprise to the upside suggesting there is still plenty of steam left in the economic recovery. A clear indication of the strength of the economy was last week’s decline in unemployment claims. See the chart below from the Federal Reserve Bank of St. Louis showing the continued precipitous drop in unemployment claims over the past year and reaching the lowest level since March 2020.

One piece of information released

last week was certainly good news for retired folks and Social Security Income

recipients. According

to the Social Security Administration, payments of America’s 64 million

retirees will increase by 5.9% next

year in the retirement benefit’s biggest cost of living adjustment (COLA) since

1982. While

this “wage inflation” adjustment seems like

good news to retirees, the reality is that the cost goods and services in

the U.S. is increasing at recently unprecedented

levels. Last

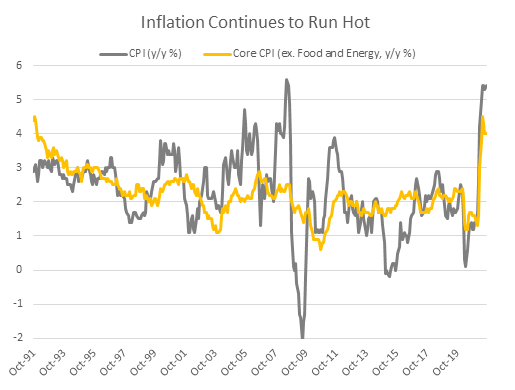

week’s release of September CPI (consumer price index) showed inflation is

continuing to heat up. CPI was up 5.4% year-over-year due

mostly to food and energy prices, while Core

CPI (ex food and energy) was up 4% year-over-year. (See chart

below from Bloomberg).

Clearly, the Fed has successfully

engineered inflation (as was their plan all along). And having annual inflation

well below their 2% target level, we are going to get numbers

well above 2% to move the

average number higher. The

question for the markets and investors is: Will inflation be transitory or

permanent? Generally, energy prices can be transitory as supplies

eventually catch up to demand and prices adjust. However,

wages and food price increases tend to stick around much longer. Large

and powerful unions such as the Longshoremen and Teamsters will use the current

supply chain disruptions and cargo ship back log to

negotiate labor contracts more favorably for workers. Conversely,

continued improvements in technology such

as microchip capacity and cloud storage prices will put

negative pressure on inflation and resultant prices.

The concerns with China seem to

have softly abated

this week as the Chinese Central Bank (PBoC) reported

that the problems with Chinese real estate developer Evergrande, are unique to

the company and not endemic of the overall real estate

market in the country. Additional positive news for the U.S.

came around shipping rates from China. China’s

official Global Times reported last week that shipping rates from China to the

U.S. west coasts are down 22% over the past 4 weeks. While

west coast ports are still congested, the tide may have turned on the supply of

available

goods which will clearly help to ease inflationary

pressures.

As mentioned above, earnings

announcements from companies last week surprised to the upside; specifically

bank and financial stocks topped analysts’ expectations with

names like Goldman Sachs showing higher revenues from trading and investment

banking. The threefold pressures on

economic growth: positive earnings releases, unemployment claims dropping,

and softening of global supply chain

disruptions all point to the potential of solid market returns for 2021. Inflation

will remain a concern and COVID-19 variant cases, while lessening globally,

could impact the economy going forward if we see

a spike later in the year. As always, keep to your long-term

financial plan and understand the markets are more

efficient than investors.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

September retail sales surprised to the upside, increasing 0.7% month-over-month (m/m) and 13.9% year-over-year (y/y). Economists expected September’s retail sales to decline slightly m/m.

CORPORATE EARNINGS

POSITIVE

S&P 500 Q3 earnings season is just kicking off. With <10% of companies having reported, sales and earnings are up 15% and 29%, respectively. However, company commentary suggests that the supply chain will be problematic in the coming quarters.

EMPLOYMENT

POSITIVE

The unemployment rate is down to 5.2%. In August, new job creation was disappointing, but jobless claims were as low as they have been since March 2020.

INFLATION

NEUTRAL

CPI rose 5.4% year-over-year in September, driven by the global supply chain backlog.

FISCAL POLICY

POSITIVE

A bill to lift the U.S. debt ceiling by $480 billion – which should provide enough headroom for government operations until December 3 – was passed this week.

MONETARY POLICY

POSITIVE

In recent communications, the Fed has indicated bond tapering may begin by the end of 2021 while rate hikes could commence by the end of 2022. Nonetheless, monetary policy remains relatively accommodative with rates at historical lows.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

Although the Taliban’s control in Afghanistan is concerning, it is unlikely to have a meaningful economic impact.

ECONOMIC RISKS

NEUTRAL

Supply chain disruptions caused by the Delta variant are hampering the economy, however, demand remains very strong. While supply bottlenecks will likely arise over time as new strains surface, the hold-ups appear primarily transitory and should ease progressively in a post-COVID world.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in

Wednesday, 6 PM for “Your Financial Choices” – Guest

hosts Rodman Young and Jaclyn Cornelius from Valley National Financial Advisors

will discuss: Retiring Early.

Laurie can

address questions on the air that are submitted either in advance or during the

live show via yourfinancialchoices.com.

Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.