by William Henderson, Vice President / Head of Investments

Markets were weaker across the board last week as each major index show a negative return. Further, as noted earlier last month, September proved to be a losing month overall, keeping with stock market history. Last week, the Dow Jones Industrial Average lost -1.4%, the S&P 500 Index lost -2.2% and the NASDAQ closed -3.2% lower. Poor weekly showing by the indexes chipped away at year-to-date gains, but each major index remains solidly in the black column. Year-to-date, the Dow Jones Industrial Average has returned +13.7%, the S&P 500 Index +17.3% and the NASDAQ +13.6%. Bond yields rose last week as implications of reduced monetary stimulus, inflation concerns and the Fed’s previous announcement of bond purchase tapering by year 2021, sank in and investors reacted accordingly. The 10-year U.S Treasury closed the week at 1.49%, eight basis points higher than the previous week but still below the March 2021 high of 1.74%.

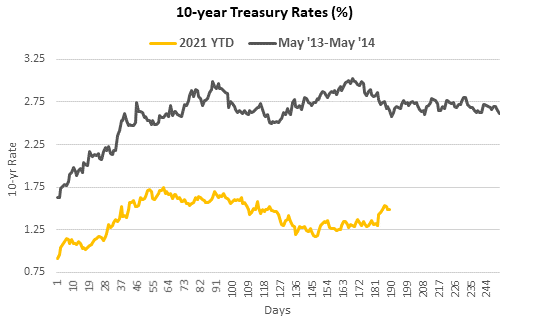

Much has been made of the Fed’s tapering and parallels have been drawn between the 2013-2014 “Taper Tantrum,” where the Fed previously announced and subsequently followed through with a substantial tapering of bond purchases. The chart below from Bloomberg shows the 10-year U.S. Treasury during two periods of rising rates (2013-2014) and (YTD 2021). In both instances, rates rose, and volatility entered the bond markets. However, also during both periods, the stock market continued its broader bull runs.

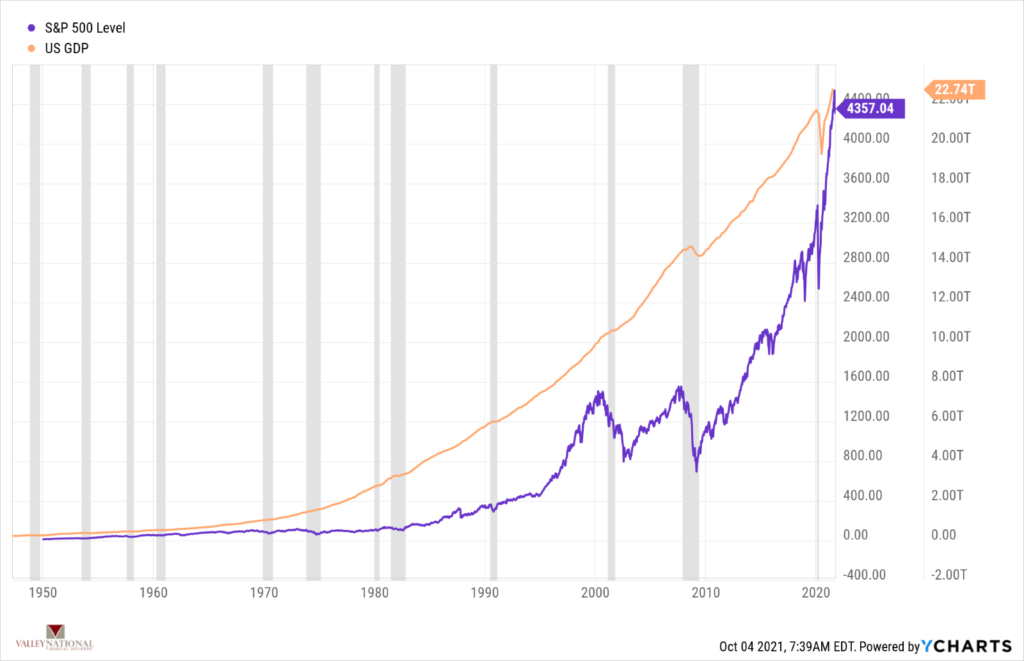

In our opinion, bond yields are impacted by the Fed while they maneuver through economic recessions and expansions, while the stock market is impacted by demographic trends and global macroeconomic factors such as GDP growth and population growth. This is evidenced by the chart below from YCharts and VNFA, where we show U.S. GDP and the S&P 500 Index from 1950 to present with recessions shaded. Notice the trend, from bottom left to upper right; and during all this time we had periods of bond yields falling and rising as impacted by the Federal Reserve’s monetary policy. Certainly, volatility in markets will never go away but trends are here to stay.

Looking beyond the U.S. economy and markets, we see some economic headwinds in a few places. China, the second largest economy behind the U.S., is dealing with supply chain concerns, energy shortages and fall out from Evergrande, the world’s largest indebted real estate developer, where bond holders are still awaiting their interest payment. Inflationary concerns are shared in many parts of the world as energy prices, food prices and labor shortages compound each other putting serious headwinds in the way of a global recovery from pandemic. In the U.S., lawmakers are still debating spending bills and an increase in the federal debt limit; both of which add unneeded uncertainty to the markets. While no one expects the U.S. Government to default on its debt, the anxiety produced by pandering on both sides of the aisle in Congress does not help the markets. Both sides know the debt limit must be increased but neither wants to be held responsible for adding more to the mountain of federal debt which already exceeds $28 trillion (about $86,000 per person in the U.S.).

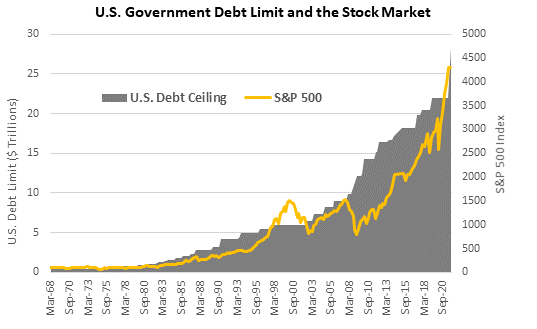

It is likely that the debt limit will be increased in the eleventh hour simply because the result of not doing so would be catastrophic and neither side of Congress wants that to happen. Given how relatively low interest rates are, the cost of borrowing by the government to finance its activities also remains historically low; thereby naturally permitting greater amounts of debt. See the chart below from Bloomberg showing U.S. Government Debt limit levels and the S&P 500 Index. The market has consistently proved itself to be more efficient and forward thinking than our own congressional leaders.

We expect the Fed to keep interest rates low even as they engage in bond purchase tapering. The economy will continue to improve while dealing with COVID-19 variants, supply chain issues, higher energy and raw material prices, and squabbling in Washington but volatility in the markets is the result. Keep focused on long-term trends and returns rather than the short-term volatility.