Tune in

Wednesday, 6 PM for “Your Financial Choices” with Laurie Siebert on WDIY

88.1FM. Laurie welcomes VNFA’s Ryan Mulhearn, CIMA®

to discuss: Behavioral

Finance.

Laurie can

address questions on the air that are submitted either in advance or during the

live show via yourfinancialchoices.com.

Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.

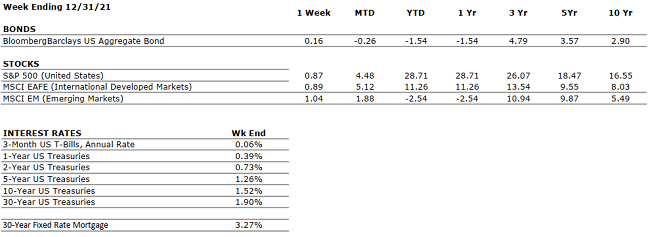

Stocks The three major U.S. equity indices – The Dow Jones Industrial Average, the S&P 500 Index and the NASDAQ Composite were each up between 21.0 – 28.7% for the full year of 2021. Continuing the year-long trend of equity industrials and dividend heavyweights outperforming technology, the S&P 500 Index came away as the big gainer for the year notching a stellar return of 28.7%. Regardless of the divergence in returns, the strong performance of all three market indexes shows the strength, depth, and breadth of the current bull market. In fact, the VIX, the standard measure of market volatility, fell throughout the year and provided very few large market pullbacks or sell-offs. Rather, the run up in stock prices in 2021 was slow and steady.

Bonds During this record rise in stock prices, fixed-income markets, while selling off early in 2021, regained some composure mid-year and stayed relatively steady into year-end. In late November 2021, on the news of the new omicron variant of COVID-19, there was a flight to quality and as a result yields on bonds fell once again. The 10-year U.S. Treasury opened 2021 at a yield of 0.91%, hit a high of 1.74% in March and then closed the year at 1.51%. While not a year for strong bond returns, for the few occasions in 2021 when risk assets sold off, it was important that smart investors held anchor positions in risk management assets like bonds.

Economy and Outlook The Fed successfully orchestrated a recovery from the pandemic-induced recession of 2020, which gave consumers the confidence to spend on everything from leisure activities to new homes and renovations to existing homes. While inflation became a concern along with supply chains disruptions, labor markets were hot all year and unemployment slowly fell to 4.2% as hiring continued across all sectors of the economy. The omicron variant could have some impact on the future hiring process and worker’s willingness to return to work. However, the strength and virulent activity of this strain has proven weaker than previous variants. Further, it seems logical to assume that as the strains expand and mutate, they get weaker and eventually the pandemic becomes an endemic.

As we

look to 2022, there are headwinds and tailwinds to consider. While monetary

stimulus will slowly get removed as the Fed reduces its bond buying and then

moves to higher interest rates, fiscal stimulus could continue in the form of

big policy spending like the Biden-proposed $1.8 trillion Build Back Better

Bill. The consumer starts the year in excellent financial shape bolstered by

strong increases in savings accounts and limited spending in 2021. Corporate

balance sheets are also in excellent shape allowing firms to boost wages and

hiring but supply chain disruptions and drastic increases in raw material costs

pose dilemmas for corporate CEOs. Wall Street economists are modestly

optimistic on 2022 with growth estimates for U.S. GDP averaging +3.0% which

certainly provides a solid base that supports the continuation of the bull

market.

An issue to keep in perspective is inflation and whether current

elevated inflation levels remain in place or prove to be transitory and temporary.

The Fed has committed to focus on inflation and will take the relatively high

inflation numbers seriously as they consider future monetary policy. Recall

that the Fed operates under a dual mandate of price stability and full

employment.

We are clearly in the camp that the U.S. economy and corporate America

will continue to recover as we move into the post-pandemic period. The omicron

variant worries us, but its impact seems less so that previous strains. Overall,

the economy and the markets are headed in the correct direction, but we are

moving into a period where fiscal and monetary stimulus will be waning, and

markets will take some time to digest that significant change.

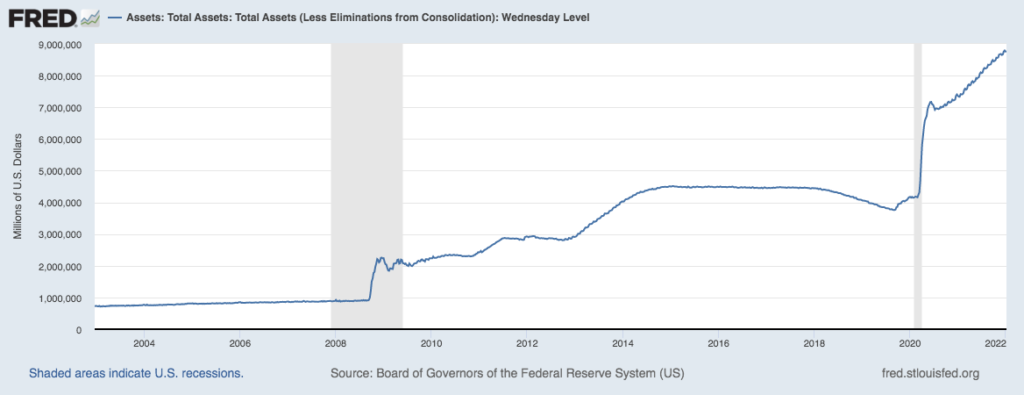

by William Henderson, Vice President / Head of Investments Equity markets began the year with a dose of volatility that was largely absent in 2021; with all three indexes selling off and U.S. Treasury yields rising leaving investors with few places to shelter from the storm. The Dow Jones Industrial Average lost a respectable –0.3%, the S&P 500 Index lost –1.8%, and the NASDAQ got walloped dropping –4.5%. All the news that was fit to print was bad for the markets and the headlines were dominated by the Fed and the release of the minutes from the December 2021 FOMC meeting. The minutes revealed a Fed not only willing to taper bond purchases and raise rates in 2022 but one also willing to begin some serious balance sheet management. This sent the yield on the benchmark 10-Year U.S Treasury higher by 40 basis points to 1.75%. The Fed’s attention to its balance sheet should not be considered shocking in our view as you look at how large balances have grown even since the Great Financial Crisis of 2008 and before the pandemic. (See the chart below from the Federal Reserve Bank of St. Louis.)

Certainly, a Fed relying

more heavily on balance-sheet reduction, which in turn removes liquidity

from the market as the largest buyer of bonds slows its process, although this

action alone may not be all bad for markets. With this action, the Fed

could focus more on its balance sheet and less on rate hikes as a way of

removing monetary stimulus. Lower short-term interest rates allow

for a steeper yield curve (the measure of rates between short-term levels and

long-term levels); which generally is good for financial

firms and banks and therefore the overall economy.

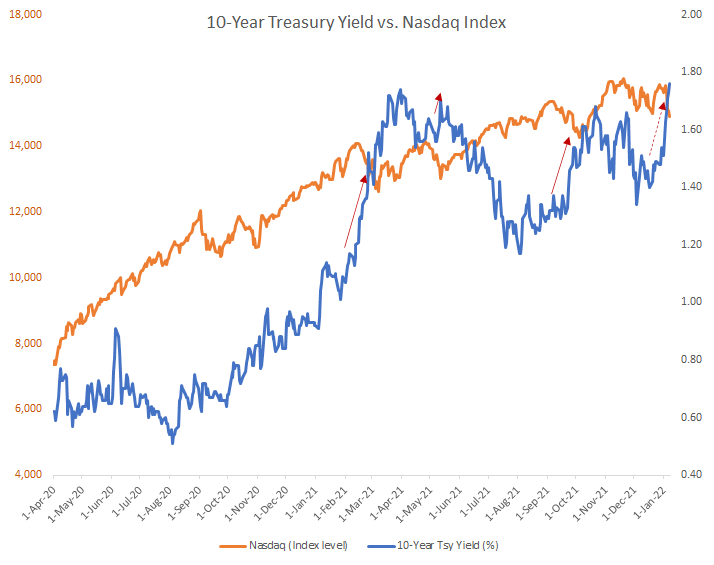

Last week’s market moves were impactful,

but this same movie

played early last year, and Wall Street strategists

prognosticated

the

great growth-to-value rotation in equity markets. Yet,

by the end of the year, markets moved closer to

parity and all three major indexes posted strong gains for the full year. Three

times since the pandemic interest rates rose

sharply in a brief time followed by a sell-off in growth stocks

and the NASDAQ. (See

the chart below from FactSet)

Generally, the technology heavy

NASDAQ sees higher rates as a headwind to upward performance. This is true

because technology firms typically borrow more than established firms and

therefore higher rates affect future performance, due to

increased borrowing expenses. Besides

the obvious relationship between rates and growth, this chart also shows that

these selloffs

tend to be brief and often create

a window to buy technology and growth sectors at

more

reasonable

prices.

2022 looks to be a year with more volatility and uncertainty than 2021. You will hear the phrase “All Eyes on the Fed” about 1,000 times this year as Wall Street tries to decipher the FOMC dot plots and tea leaves of Fed minutes and comments made by Chairman Jay Powell at his press conferences. It is understood that monetary policy whether in the form of higher rates, less bond purchases or balance sheet management must be adjusted to reflect recent strong inflation data and an unemployment level reaching 3.9%. Fiscal policy seems in flux as well, as President Biden’s Build Back Better plan flounders in Washington with each passing week. This leaves us with the consumer and the corporation to propel the economy alone. That’s not a bad picture when you consider both are very healthy with strong balance sheets, healthy cash positions and relatively low interest rates.

This week we will get a good amount of economic data with inflation (CPI) coming out Wednesday, unemployment level on Thursday and retail sales and consumer confidence on Friday. “All Eyes on the Fed”? We say all eyes on the consumer.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

U.S. GDP growth decelerated to a 2% annualized pace in Q3. The slowdown was driven primarily by supply chain constraints. Economists expect a modest acceleration in Q4. Early high-frequency data (shopping, travel, movie ticket sales) is showing some slowing. Holiday retails sales numbers will be important to gauge consumer behavior.

CORPORATE EARNINGS

POSITIVE

Fourth quarter wrapped up and earnings are likely to be impacted by labor, supply shortages, price increases and wage inflation. As EPS estimates are ironed out each of these items will play a role, some greater than others. Watch for increases but at a muted pace.

EMPLOYMENT

POSITIVE

Although December increase in payrolls did not meet expectations (199,000 jobs added versus 422,000 expected), the unemployment rate fell to 3.9% versus an expected 4.1%. Wages increased more than expected at 4.7% year-over-year. Strong recovery in leisure and hospitality which had the biggest gain by industry and accounted for more than 25% of all jobs added in December (55,000).

INFLATION

NEGATIVE

CPI rose 6.8% year-over-year in November, the highest increase since 1982, driven by the global supply chain backlog and continued consumer pent up demand. Will inflation be transitory or permanent? Goldman Sachs capital market assumption forecast CPI at an average of 3.1% for 2022 suggesting a significant decrease in inflation from the current 6.8%. Updated inflation numbers for December to be released on January 12th.

FISCAL POLICY

NEUTRAL

The Build Back Better Bill has been pushed into 2022 in a scaled back $1.8 trillion version as Senator Manchin continues to hold back support. The economy seems to be digesting a new world where fiscal policy is no longer considered an economic stimulus.

MONETARY POLICY

NEUTRAL

Fed discussed a triple threat of tightening: raise interest rates, halt purchases, and reduce its balance sheet (reducing holdings of Treasurys and mortgage-backed securities). Gradual and steady reduction of liquidity will be key in preserving market performance (fast and sudden changes would most likely result in panic-driven sell offs). Expect three rate hikes in 2022 beginning in March.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

The new omicron COVID-19 variant has shown up in many parts of the world. This strain seems less virulent and more reactive to boosters so its impact it still yet to be calculated. A rebound in travel and leisure now seems unsure. Important to watch the Russia/Ukraine situation.

ECONOMIC RISKS

NEUTRAL

Supply chain disruptions are hampering the economy; however, demand remains very strong. While global logistics are operating far below normal efficacy, it appears the supply chain is slowly improving and may reach normalcy by mid-to-late-2022.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in

Wednesday, 6 PM for “Your Financial Choices” with Laurie Siebert on WDIY

88.1FM. Laurie welcomes William Henderson, VP/Head of Investments at VNFA to

discuss: 2021

Review & 2022 Outlook

Laurie can

address questions on the air that are submitted either in advance or during the

live show via yourfinancialchoices.com.

Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.

Fourth quarter estimated tax payments are due January 18, 2022. These estimates may include federal, state and/or local vouchers depending on your situation.

If quarterly estimates were recommended when we prepared your 2020 return, they would be included with your tax return. If you requested a paper client copy of your return, the instructions, vouchers and envelopes were included with your tax folder. If you requested an electronic client copy, the instructions and vouchers were included in both the client copy and action needed copy posted to your client portal.

Please follow the applicable instructions previously provided to mail your payment and voucher by January 18, 2022.

There may be situations where the estimates were generated, but an overpayment was applied in full or in part. If your income or withholdings have significantly changed since last year, please contact your tax preparer to review. If you change or do not make the estimates, please let your tax preparer know at tax filing time.

Given the recent rapid spread of the omicron variant and the addition of potential exposures over the holidays, this week most of our team will be working remotely. Our offices will be open for scheduled appointments and deliveries during normal office hours. Our commitment to keep our team and our client safe continues to be a priority and we thank you for your understanding as we continue masking inside our office spaces in January.

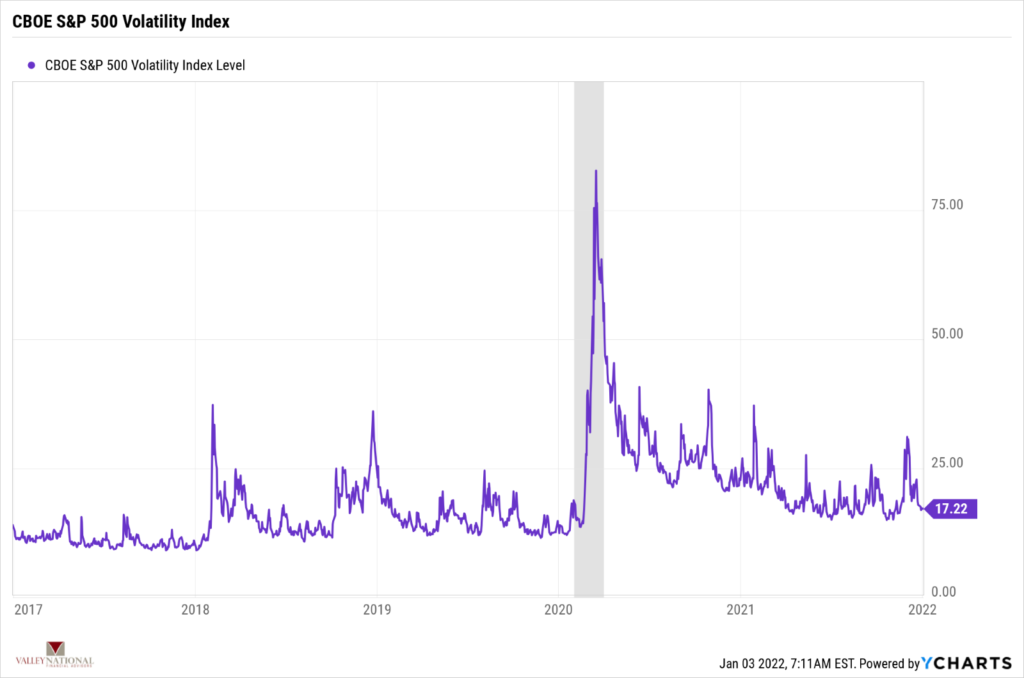

by William Henderson, Vice President / Head of Investments Stocks ended the year on a mixed note with the broader markets posting modest gains while the technology-laden NASDAQ notched a barely noticeable loss. The Dow Jones Industrial Average rose +1.1%, the S&P 500 Index gained +0.9%, and the NASDAQ dropped –0.1%. Massive piles of cash in consumer coffers, corporate earnings hitting new records, and waning but still in place federal monetary and fiscal stimulus propelled markets to new records in 2021 and the patient investor was richly rewarded with double-digit full year 2021 returns in all three major market indexes. Year-to-date 2021, the Dow Jones Industrial Average has returned +21.0%, the S&P 500 Index +28.7% and the NASDAQ +22.2%. What made the returns in equities more palatable was that these returns were garnered with very little volatility. A brief look at the VIX (Chicago Board of Options Exchange S&P 500 Volatility Index), which measure stock market volatility shows that by historic measures the VIX in 2021 was calm. See the chart below from YCharts and Valley National Financial Advisors. There were very few spikes in the VIX above 25, and for most of the year, the index was modestly falling.

During this record rise in stock

prices, fixed-income markets, while selling off early in 2021, regained some

composure mid-year and stayed relatively steady into year-end. he 10-year

U.S. Treasury opened 2021 at a yield of 0.91%, hit a high of 1.74% in March and

then closed the year at 1.51%. While not a year for strong bond returns,

for the few occasions in 2021 when risk assets sold off, it was important that

smart investors held anchor positions in risk management assets like bonds.

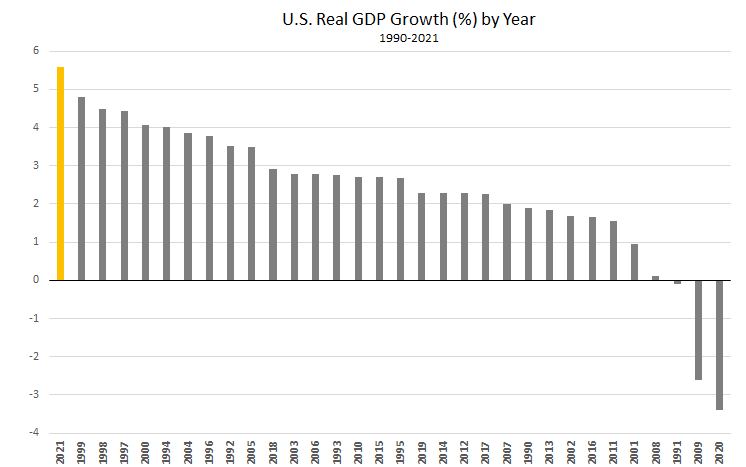

As mentioned, corporate earnings

were strong, reflecting economic growth that was the strongest since 1984. (See

the chart below from Factset.)

The Fed successfully orchestrated

a recovery from the pandemic-induced recession of 2020, which gave consumers

the confidence to spend on everything from leisure activities to new homes and

renovations to existing homes. While inflation became a concern along with

supply chains disruptions, labor markets were hot all year and unemployment

slowly fell to 4.2% as hiring continued across all sectors of the

economy.

As we look to 2022, there are

headwinds and tailwinds to consider. While monetary stimulus will slowly

get removed as the Fed reduces its bond buying and then moves to higher

interest rates, fiscal stimulus could continue in the form of big policy

spending like the Biden-proposed $1.8 trillion Build Back Better Bill. The

consumer starts the year in excellent financial shape bolstered by strong

increases in savings accounts and limited spending in 2021. Corporate

balance sheets are also in excellent shape allowing firms to boost wages and

hiring but supply chain disruptions and drastic increases in raw material costs

pose dilemmas for corporate CEOs. Wall Street economists are modestly

optimistic on 2022 with growth estimates for U.S. GDP averaging +3.0% which

certainly provides a solid base that supports the continuation of the bull

market.

Stay focused on the

tailwinds while being aware of the headwinds and keep a long-term perspective

on your investments and your financial plan.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

U.S. GDP growth decelerated to a 2% annualized pace in Q3. The slowdown was driven primarily by supply chain constraints. Economists expect a modest acceleration in Q4. Early high-frequency data (shopping, travel, movie ticket sales) is showing some slowing. Holiday retails sales numbers will be important to gauge consumer behavior.

CORPORATE EARNINGS

POSITIVE

Fourth quarter wrapped up and earnings are likely to be impacted by labor, supply shortages, price increases and wage inflation. As EPS estimates are ironed out each of these items will play a role, some greater than others. Watch for increases but at a muted pace.

EMPLOYMENT

POSITIVE

The unemployment rate is down to 4.2%, as of November. The labor market is very tight at present as many employers, particularly in the Leisure and Logistics sectors, are struggling to fully staff because the labor participation rate remains below pre-COVID levels. The labor shortage is one of the causes of the global supply chain glut.

INFLATION

NEGATIVE

CPI rose 6.8% year-over-year in November, the highest increase since 1982, driven by the global supply chain backlog and continued consumer pent up demand. Will inflation be transitory or permanent? Powell may remove “transitory” from his testimony this week.

FISCAL POLICY

NEUTRAL

The Build Back Better Bill has been pushed into 2022 in a scaled back $1.8 trillion version as Senator Manchin continues to hold back support. The economy seems to be digesting a new world where fiscal policy is no longer considered an economic stimulus.

MONETARY POLICY

POSITIVE

By early 2022, all Fed bond purchases will halt. The Fed’s bond buying program works to keep interest rates low. Once tapering ends, rate hikes follow. Mid-June or sooner for rate hike?

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

The new omicron COVID-19 variant has shown up in many parts of the world. This strain seems less virulent and more reactive to boosters so its impact it still yet to be calculated. A rebound in travel and leisure now seems unsure. Important to watch the Russia/Ukraine situation.

ECONOMIC RISKS

NEUTRAL

Supply chain disruptions are hampering the economy; however, demand remains very strong. While global logistics are operating far below normal efficacy, it appears the supply chain is slowly improving and may reach normalcy by mid-to-late-2022.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.