Team VNFA is taking a short break for an afternoon – Thursday, May 26. Of course, you will be able to reach us with any urgent questions or trade requests. Otherwise, our offices will be closed starting at noon on Thursday. We are taking a few hours for team building and relaxation after another busy tax preparation season.

Our offices will be closed on Monday, May 30 in observance of the Memorial Day holiday.

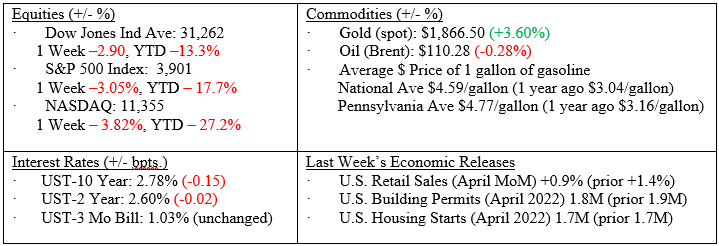

by William Henderson, Chief Investment Officer Markets continued to reel from a slew of negative news headlines including poor earnings releases from retail stalwarts Wal-Mart and Target, new cases of COVID-19 in Shanghai, and persistent inflation especially in gasoline with the national average for a gallon of gasoline hitting $4.59/gallon vs $3.04/gallon one year ago. Thankfully, U.S. equities posted a monster 614-point rally late on Friday which allowed the markets to avoid being labeled a true “Bear Market” (meaning down 20% on the S&P 500 – see returns below).

Markets (as of May 20, 2022; 1 week Returns, Year-to-date Returns)

It is hard being a market optimist these days and we can certainly understand how investors feel given year-to-date returns on stocks and bonds are so poor. Further, you would think the world is in even worse shape than the markets are telling us if you listen to the news. A new pandemic called Monkeypox is making headlines along with baby formula shortages in the United States seem like stories ripped from a movie about the end of the world. A market prognosticator once said, “if someone wants to bet you on the end of the world, take that bet.” We are on the other side of that bet as well. Current headlines are bad and downright scary, but the underlying fundamentals of our economy remain sound. However, the issues surrounding us are real and impact consumers in ways that eventually impact the economy. Remember, our economy is 60-65% consumer driven and when the consumer slows down or stops spending the economy will be impacted in a big way.

Several Wall Street economists are calling for a recession within the next 12 months. Certainly, with the S&P 500 Index down -18% year-to-date, the markets have already priced in a 75% chance of a recession. The issue at hand is that the Fed is doing its part to combat inflation, not prevent a recession. Fed Chairman Jay Powell refuses to temper his hawkish tone and instead is committed to raising all year toward a more neutral rate of 2.25% to 2.50% (currently 0.75% to 1.00%). At that level, or even a bit higher, it is expected that inflation will begin to significantly decline.

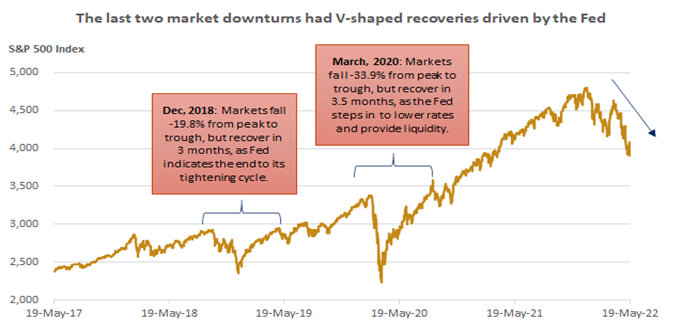

As mentioned, the Fed is focused on fighting inflation rather than the markets and that is a dramatic change from previous market downturns. See the chart below from Edward Jones showing the two previous downturns (2018 & 2020) and the Fed’s reaction to those market selloffs. At the point of December 2018 correction sparked by growth concerns, the Fed clearly and succinctly stated lower interest rates were ahead which helped spur a rapid market rebound. Similarly, at the March 2020 pandemic-related sell-off, the Fed came into the markets with every tool in their toolbox and markets again rebounded quickly.

Here we are in 2022, and the Fed is on a different mission than helping the markets rebound quickly. Instead, Mr. Powell and his Fed are all about fighting inflation. That clear divergence in mission is pushing a slower market recovery than a quick snapback as witnessed in the two previous significant downturns.

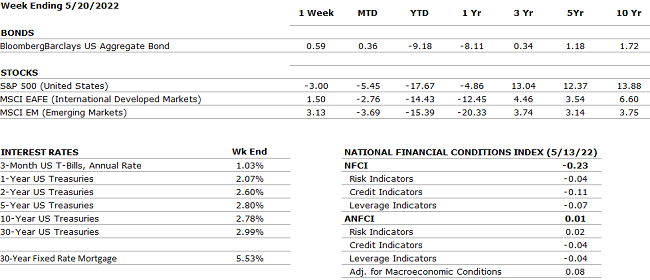

We talked above about bond and stock markets both suffering poor returns thus far in 2022. However, for the second week in a row, U.S. government bonds rallied sending the yield on the 10-Year U.S. Treasury to 2.78% down from 3.13% a couple of weeks earlier. While a long way from the 1.51% yield we saw at the beginning of the year, the move higher in Treasury Bond prices has softened the hit fixed income investors have taken thus far in 2022. It also shows there is a modest flight to quality in the markets with buyers moving once again to U.S. Treasury Bonds when markets sell-off so aggressively.

Watch for a few important economic indicators this week including the release of the minutes from the May Federal Reserve meeting on Wednesday and the Personal Consumption Expenditures (PCE) Price Index – the Fed’s preferred gauge for tracking inflation – on Friday. We remain committed to a long-term investment philosophy and understand that sell-offs and market corrections are common in well-functioning financial markets.

THE NUMBERS The Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

Q1 2022 Real GDP shrunk at a 1.4% annual rate according to the first advance estimate. This is the first contraction since the beginning of the pandemic. The main factors that resulted in a decrease in GDP were a surge in imports and trade deficit highlighting that the U.S. is buying more goods from foreign countries. This may be an indication that the U.S. economy has recovered faster than other countries.

CORPORATE EARNINGS

NEUTRAL

For Q1 2022 the estimated earnings growth rate is 9.1% — the lowest since Q4 2020 (3.8%). This estimate was revised upward from the previous forecast of 7.1% in April. So far, 91% of S&P500 companies have reported earnings — 77% reported a positive EPS surprise and 74% beat revenue expectations.

EMPLOYMENT

POSITIVE

Total nonfarm payroll employment rose by 428,000 in April compared to an estimated 398,000. The unemployment rate remained constant at 3.6%. Job growth was widespread, led by gains in leisure and hospitality, manufacturing, and transportation and warehousing.

INFLATION

NEGATIVE

CPI rose 8.3% year-over-year in April 2022, compared to an estimated increase of 8.1%. Core CPI recorded a 6.2% increase, and PPI increased by 11%. Shelter, food, airline fares, and new vehicles were the largest contributors to the soar in CPI. The energy index fell for the first time in recent months — gasoline decreased by 6.1% while natural gas and electricity increased.

FISCAL POLICY

NEUTRAL

After passing a $13.6 billion package to support Ukraine a few weeks ago, the House approved an additional $40 billion military and humanitarian package for Ukraine. The bill was passed with 368 votes against 57 votes. The total of the two packages ($53 billion) is the largest foreign aid moved through Congress in over 20 years.

MONETARY POLICY

NEUTRAL

The Fed raised rates by the expected 25 bps in March and 50 bps in May. Jay Powell projected a clear path for 2022 with as many as five additional rate hikes bringing short-term rates to 1.75- 2.00% by year end 2022. The next decisions by the Fed will be data-driven based on future inflation numbers and estimated economic growth.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEGATIVE

Russia was able to avoid default last week by making the required payment on its debt however, the markets are still assessing the probability of default in the coming months at 87%. This is primarily due to sanctions imposed by Western countries which are hindering the Russian economy and restricting capital flows in and out of Russia.

ECONOMIC RISKS

NEUTRAL

Supply chain disruptions in the U.S. are waning but the rising cost of oil due to the Russian- Ukraine war is likely to cause additional inflationary pressures not only on gasoline prices but also on many other goods and services. China is targeting June to end the Shanghai Covid-19 lockdown in hopes to revive its economy.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in Wednesday, 6 PM for “Your Financial Choices” with Laurie Siebert on WDIY 88.1FM. Laurie welcomes guest Daniel Banks from Silvercrest Insurance to discuss: Medicare Supplemental Plans & Premiums

Laurie can address questions on the air that are submitted either in advance or during the live show via yourfinancialchoices.com. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.