Join us in congratulating Amanda Pugliese, CPA on her promotion to Director of Tax Services.

Mandy has been part of Team VNFA for more than 14 years in several capacities, most recently as Senior Tax Manager. In addition to continuing to work on tax preparation and planning, Mandy will manage the VNFA Tax Department moving forward.

Tim Richmond, CPA has been given the title of Senior Tax Accountant. Tim joined the team in 2020, bringing 15 years of experience in tax and accounting.

Team VNFA is still searching for CPA professionals to join our Tax Department and work with Tim and Mandy. Learn more about this and other opportunities at valleynationalgroup.com/ join-our-team

Major equity markets finished mixed last week with the Dow Jones Industrial Average falling by a modest -0.13%, the S&P 500 Index increasing +0.36% and the NASDAQ finishing the week up a healthy +2.15%. Markets were compelled higher on an extraordinarily strong July 2022 new jobs numbers +528,000 and a near record low unemployment level of 3.5%. This new employment data means the economy has gained back all the jobs lost since the COVID-19 pandemic began in March of 2020.

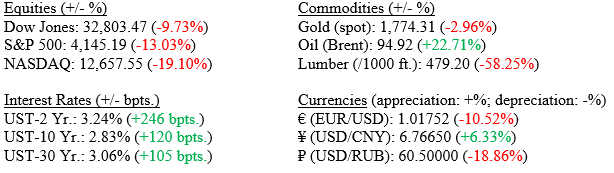

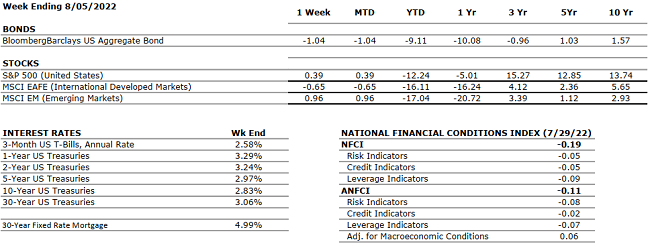

Markets (as of EOD 08/05/2022; change YTD)

Global Economy U.S. Treasury bonds sold off last week on Friday’s stronger-than-expected jobs report. Investors sold bonds on the news and the yield of the 10-Year U.S. Treasury bond increased to 2.83% from 2.67% last week. What is more important to watch is the continued steeply inverted yield curve (Chart 1) we are witnessing with the 2-Year U.S. Treasury yielding 3.24% vs the 10-Year U.S. Treasury at 2.84%. We have mentioned it many times that inverted yield curves (when shorter-term bonds yield more than longer-term bonds) typically precede recessions.

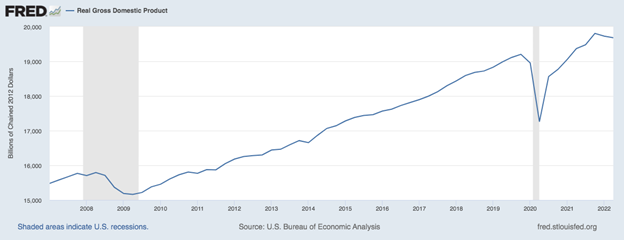

Since the curve first inverted earlier in 2022, we have since seen two quarters of negative GDP (Gross Domestic Product): 1Q -1.6% and 2Q -0.9%; which historically has defined a recession (Chart 2).

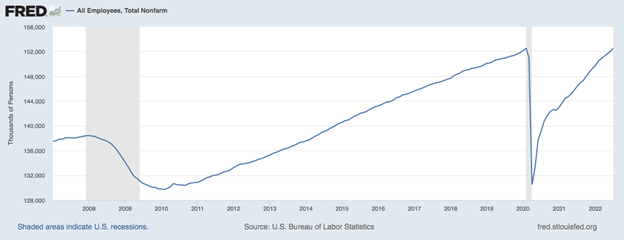

Herein lies the conflicting data the Fed and economists need to deal with. We have massive new job growth (Chart 3) strong EPS (Earnings Per Share) and healthy U.S. banks, so it is difficult to admit we are in a recession.

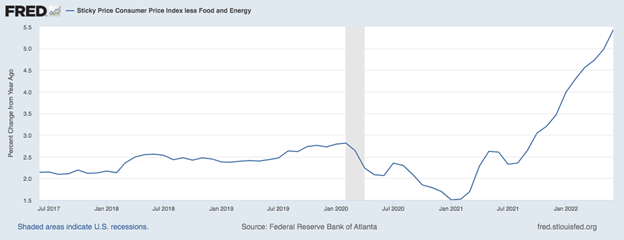

However, continued hot inflation data (Chart 4) is compelling the FOMC (Federal Open Markets Committee) to raise rates aggressively, which is slowing the economy, as shown in Chart 2 above.

Our summary here is that the markets are telling us something different than the economic data. Since the 10-Year U.S. Treasury bond hit its recent high on June 14, 2022, of 3.48%, the S&P 500 Index is up 11%. Whether this signaled the end of the bear market or not is yet to be seen. However, the stock market has historically been the best predictor of future economic growth. We are giving credit to Chairman Powell and hoping that he can achieve a path to a soft landing from extremely high inflation to modest inflation (~2.5%) and solid employment (unemployment ~ 3.5%).

What to Watch

U.S. Retail Gas Price for the week of August 8, 2022, released at 4:30 p.m. on August 8th.

U.S. Consumer Price Index, Year-over-Year for July 2022 released at 8:30 a.m. on August 10th

U.S. Inflation Rate for July 2022 released at 8:30 a.m. on August 10th

U.S. Producer Price Index, Year-over-Year for July 2022 released at 8:3 a.m. on August 11th

30-Year Mortgage Rate for the week of August 11, 2022, released at 10:00 a.m. on August 11th

THE NUMBERS The Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

Q1 2022 Real GDP shrunk at a 1.5% annual rate according to the second estimate. The main factors that resulted in a decrease in GDP were a surge in imports and trade deficit highlighting that the U.S. is buying more goods from foreign countries. Real GDP for Q2 2022 decreased at an annual rate of 0.9% marking the second consecutive quarter of declining GDP.

CORPORATE EARNINGS

NEUTRAL

The estimated growth rate for Q2 2022 is now 6.0% (up from 4.3%) which would mark a new post-pandemic low; but still solidly in the “growth” stage. 56% of S&P500 companies have now reported earnings — 73% beat earnings estimates and 66% reported actual revenue above expectations. For Q3, 28 companies issued negative EPS guidance while 17 companies issued positive guidance.

EMPLOYMENT

POSITIVE

U.S. Nonfarm Payrolls for July 2022 increased by a stunning 528,000 new jobs compared to economist’s estimates of 250,000. The latest unemployment rate for July came in at 3.5%, nearing a record low. Employment activity and job growth continues to impress everyone while also confounding everyone as GDP is slowing at the same time.

INFLATION

NEGATIVE

The annual inflation rate in the US accelerated to 9.1% in June, the highest since November 1981,from 8.6% in May and above forecasts of 8.8%. Core CPI increased by 5.9%, slightly below 6% in May, but above forecasts of 5.7%. The increase in CPI was driven by major surges in food and energy prices, as food costs rose by 10.4% and energy prices by 41.6%.

FISCAL POLICY

NEUTRAL

Senator Manchin and Majority Leader Schumer reached an agreement on the latest tax and energy bill. The bloated bill is stacked with incentives for green energy, EV cars, and conversely oil & gas companies for exploration. Further, no changes in private equity taxes or higher tax rates for the very wealthy were enacted.

MONETARY POLICY

NEUTRAL

The current target for Fed Funds is a range of 2.25% to 2.5%. With inflation still running hot, Fed Chairman Jay Powell is clear on his path to slow the economy enough to cool inflation. The next Fed meeting is September 20-21 and markets are pricing in another 0.50-0.75% increase in short-term rates.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEGATIVE

Russia has defaulted on its debt as of Sunday, June 26th when the 30-day grace period on $100 million of interest payments expired. This is the first Russian default since 1918. Sanctions imposed by Western powers effectively isolated Russia and its financial system from Europe and the U.S. making it much harder for Russia to complete international financial transactions.

ECONOMIC RISKS

NEUTRAL

Supply chain disruptions in the U.S. are waning but the rising cost of oil due to the Russian- Ukraine war is likely to cause additional inflationary pressures not only on gasoline prices but also on many other goods and services. Starting in June, China has started to remove some restrictions in major cities to end the COVID-19 lockdown.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in Wednesday, 6 PM for “Your Financial Choices” with Laurie Siebert on WDIY 88.1FM. Laurie will discuss: Navigating Social Security Options

Laurie can address questions on the air that are submitted either in advance or during the live show via yourfinancialchoices.com. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.