Our Chief Executive Officer, Matthew E. Petrozelli, was featured in Lehigh Valley Business as one of the Region’s Power Players in their Banking, Finance, Accounting, and Wealth Management Power List.

“This is a well-deserved recognition of Matt’s hard work and dedication to Valley National Financial Advisors. His leadership has inspired us all,” said Founder & Chairman Thomas M. Riddle, CPA, CFP®.

Matt oversees all the company’s operations and executive leadership. Under Matt’s leadership, vision, and commitment to excellence, our company has achieved tremendous success, and this recognition reflects his remarkable contributions. #TeamVNFA celebrates his continued success!

“Each employee is proud to be part of his team. This acknowledgment confirms the success of the company’s leadership transition as part of the long-term succession plan. Valley National Financial Advisors is celebrating its 38th year of serving its clients. Many more years are assured under Matt Petrozelli’s leadership,” said Founder & Chairman Thomas M. Riddle, CPA, CFP®.

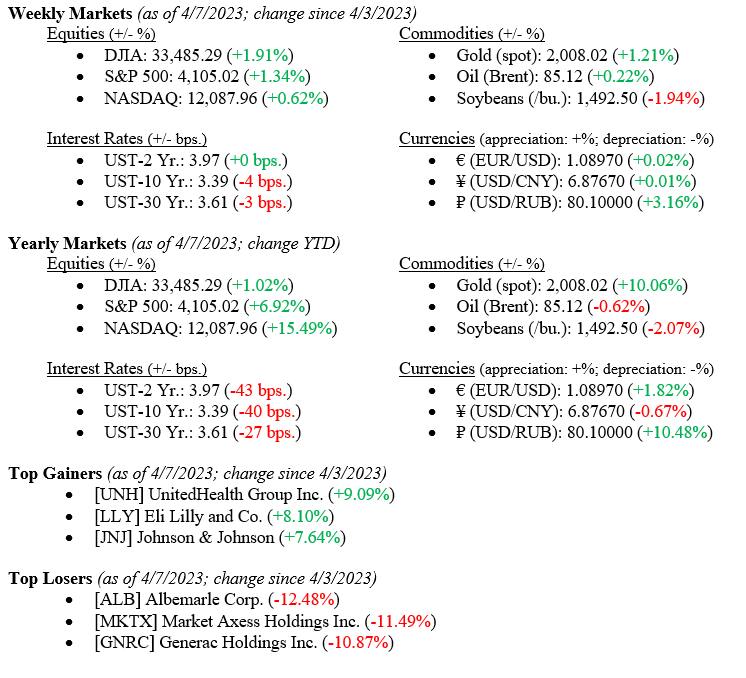

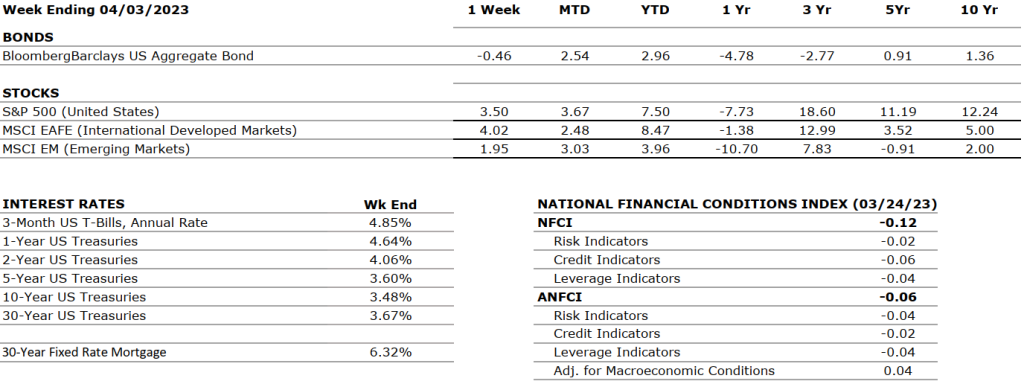

Although last week’s jobs report showed a slowing in hiring during March 2023, equity markets posted another positive week across all three major market indexes, with the Dow Jones Industrial Average leading the way at +1.91% for the week ended April 7, 2023. Meanwhile, the S&P 500 Index notched a decent +1.34% for the week, while the NASDAQ returned +0.62%. Bond prices increased during the week but only modestly, with the 10-year U.S. Treasury bond falling four basis points to close the week at 3.39%. As recently as October 2022, the yield on the 10-year U.S. Treasury was 4.25%, marking a shocking move in rates due to still-unfounded recessionary fears and a clear flight to quality after the mini-banking crisis we saw in March as Silicon Valley Bank & Signature Bank failed.

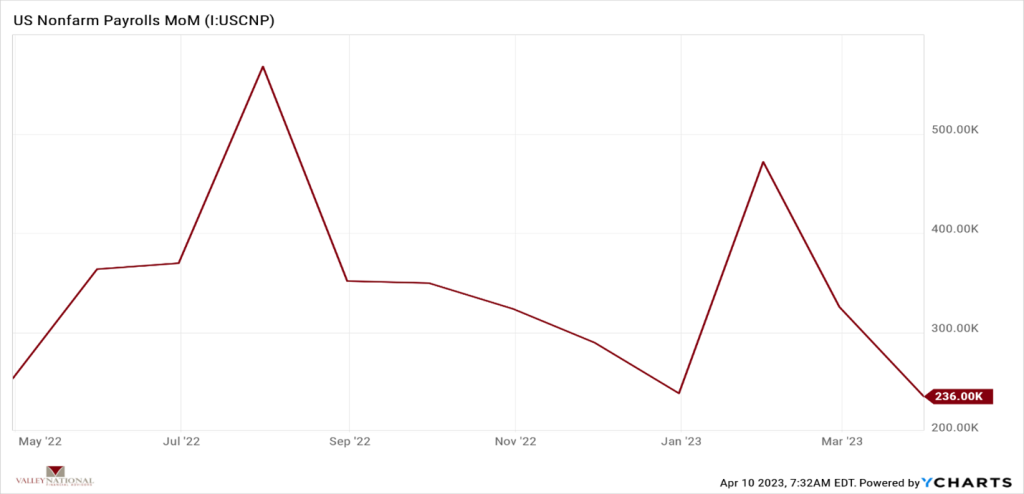

Last Friday’s employment report from the Bureau of Labor Statistics showed the U.S. added 236,000 nonfarm payrolls in March, below the median economists’ forecast of 239,000 and down from February’s revised figure of +311,000, see Chart 1 below. Oddly, the unemployment rate moved a bit lower to 3.5% from 3.6%, and the labor force participation rate increased from 62.5% to 62.6%. At VNFA, these moves are modest and still point to a strong labor market by any historical measure. We continue to believe the U.S. labor market remains a strong point continuing to underpin the economy.

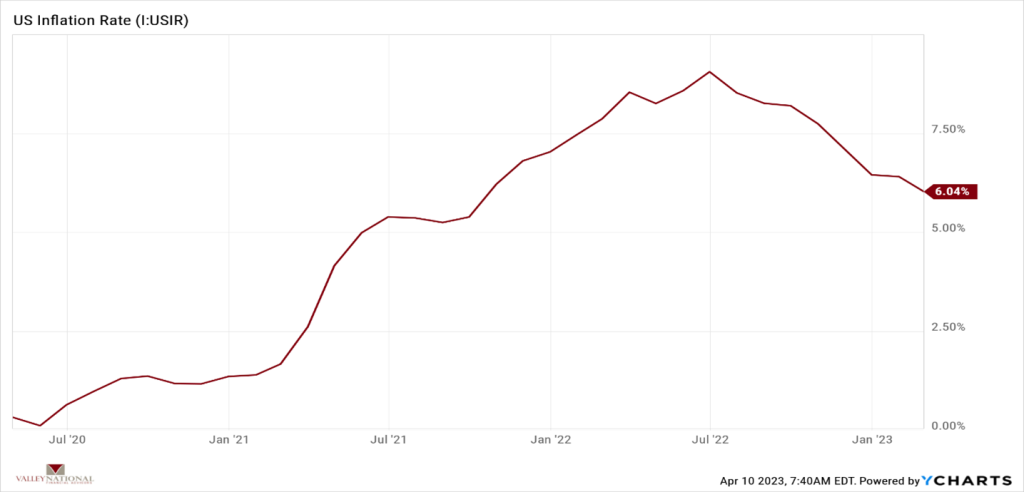

Investors understand the current objective of Fed Chairman Jay Powell is combatting inflation which peaked last summer at 9.06% and has since tapered to 6.04%, see Chart 2 below. Chair Powell has raised interest rates at a near-historic pace, and last year’s markets showed the result of that with poor returns across all sectors. As inflation comes under control and further rate hikes fade into the sunset, we expect markets to moderate but remain volatile.

What to Watch

Monday, April 10th

U.S. Wholesale Inventories MoM at 10:00AM (Prior: -0.42%)

U.S. Retail Gas Price at 4:30PM (Prior: $3.606/gal.)

Wednesday, April 12th

U.S. Consumer Price Index MoM/YoY at 8:30AM (Prior: 0.37% / 6.04%)

U.S. Core Consumer Price Index MoM/YoY at 8:30AM (Prior: 0.45% / 5.53%)

Thursday, April 13th

U.S. Producer Price Index MoM/YoY at 8:30AM (Prior: -0.15% / 4.58%)

U.S. Core Producer Price Index MoM/YoY at 8:30AM (Prior: -0.00% / 4.40%)

30 Year Mortgage Rate at 12:00PM (Prior: 6.28%)

Friday, April 14th

U.S. Export Prices MoM/YoY at 10:00AM (Prior: 0.20% / -0.85%)

U.S. Import Prices MoM/YoY at 10:00AM (Prior: -0.14% / -1.05%)

U.S. Index of Consumer Sentiment at 10:00AM (Prior: 62.00)

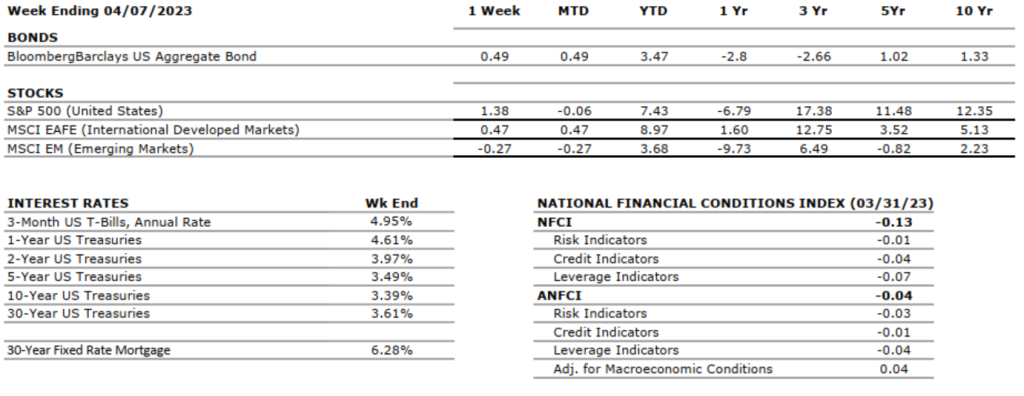

Equity markets finished the week slightly higher, while treasury yields fell slightly. Last week, the BLS (Bureau of Labor Statistics) labor report was right on target, missing median expectations by only a few thousand jobs and indicating a strong labor market as participation increased and the unemployment rate decreased. However, the strong jobs market is still running a bit contrary to the Fed’s rate-hike path. It was expected that the historic pace of rate increases would negatively affect workers and put many out of jobs, which has yet to be seen. Despite the continued strength in this area, inflation has trended downwards from a peak of 9.06% and is currently down to 6.04%, indicating that the Fed is putting up a good fight. We believe the path to 4% is ahead of us, while returning to the 2% average target may take years longer than initially expected.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five- and 10- yearreturns are annualized excluding dividends.Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

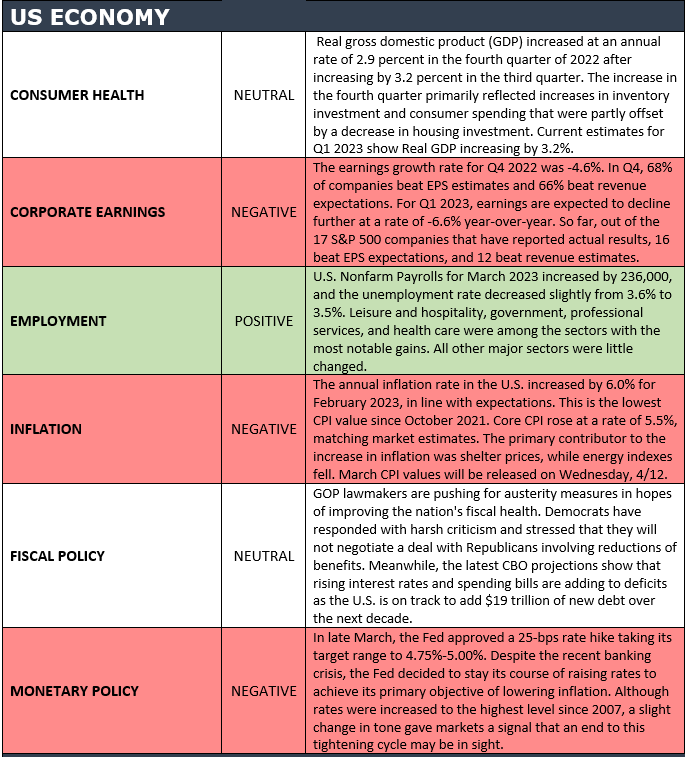

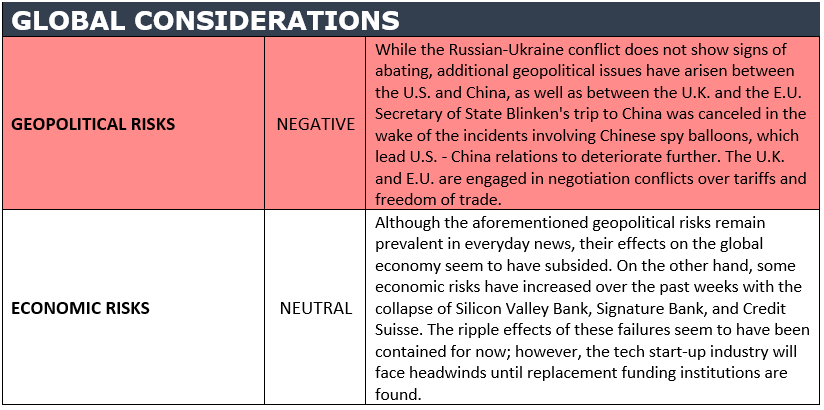

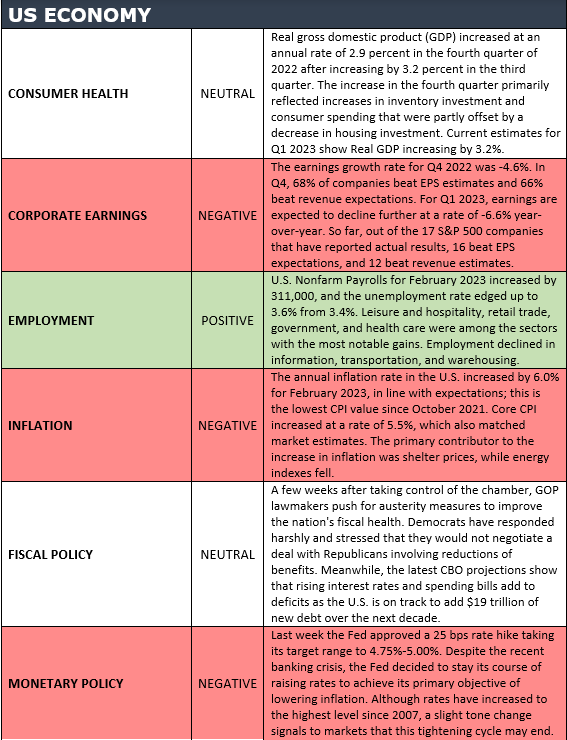

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade key economic conditions that we believe are of particular importance to investors.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Easter is also a time to celebrate the arrival of spring!

Easter is a holiday that marks the arrival of spring, new beginnings, and hope. It is celebrated by many people worldwide with traditions such as Easter egg hunts, the Easter Bunny, and springtime festivals. The Easter egg has become a popular symbol of Easter, representing new life and renewal.

The Easter Bunny is another popular symbol of Easter, known for bringing Easter eggs and treats to children who have been good throughout the year. Many people also celebrate the arrival of spring by planting new flowers, enjoying outdoor activities, and participating in community events. As we celebrate Easter this Sunday, Apr 9, 2023, let us cherish our loved ones, enjoy the beauty of spring, and spread joy and kindness to those around us.

Your VNFA family wishes you a joyful Easter filled with love and laughter.

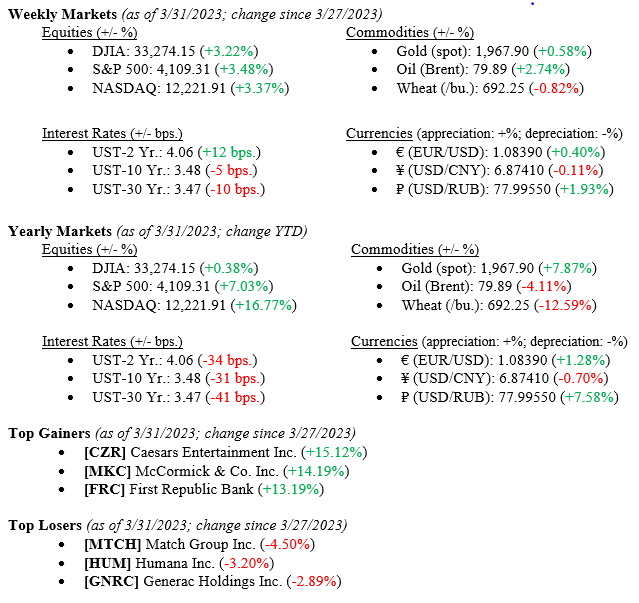

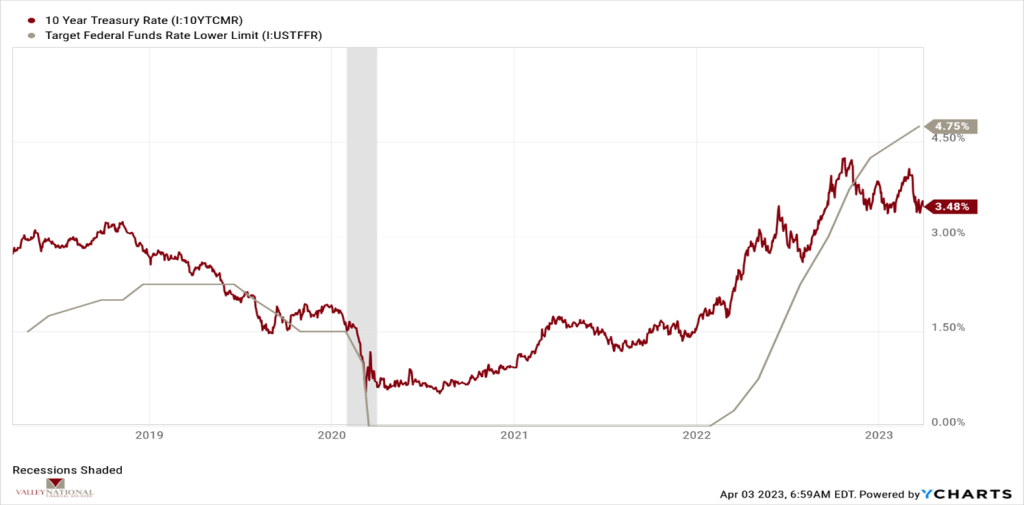

Equity markets wrapped up a volatile quarter with a volatile week as each major market index posted strong gains to end the week. The S&P 500 Index led the markets higher last week, notching a +3.48% gain, followed by the NASDAQ with a +3.37% gain, and finally, the Dow Jones Industrial Average returning +3.22% for the week ending March 31, 2023. These gains, coupled with gains thus far in 2023, pushed all three indexes into positive territory for the year’s first quarter (see year-to-date returns below). The weakness in markets spurned by the short-lived regional bank crisis was offset by investor beliefs that the Fed is finally winding down its aggressive interest rate hiking cycle, and the Fed will announce a long-awaited pause or pivot in interest movements at the May 2023 FOMC (Federal Open Markets Committee) Meeting. Interest rate expectations moved the 10-year US Treasury bond lower by 10 basis points, ending the week at 3.47%. Recall, as recently as October 2022, the 10-year US Treasury was trading at 4.24%, fully 77 basis points higher than today, see Chart 1 below.

US Economy

As mentioned above, US Treasury bonds have moved sharply lower in yield since the recent peak in rates in October 2022. Chart 1 below by Valley National Financial Advisors and Y Charts showing the current 10-year US Treasury bond yield and the current Fed Funds Target Rate). The chart shows the dramatic rise in the Fed Funds Rate (the interest rate at which depository institutions trade balances to each other overnight) as the FOMC has moved interest rates higher to combat inflation. While initially moving higher, long-term rates have tapered off and dropped, indicating that the markets are pricing to this current interest rate cycle. The equity markets are efficiently reading this Fed pivot and reacting accordingly – in the current case, by rallying in 2023.

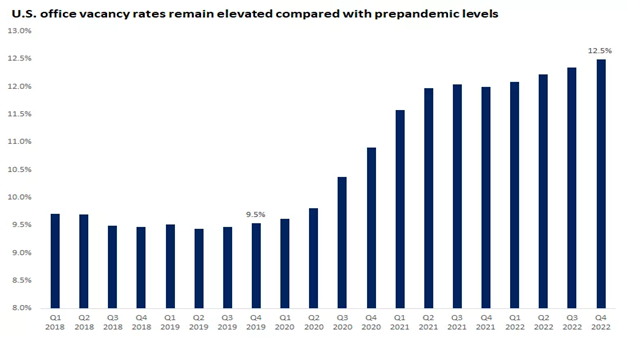

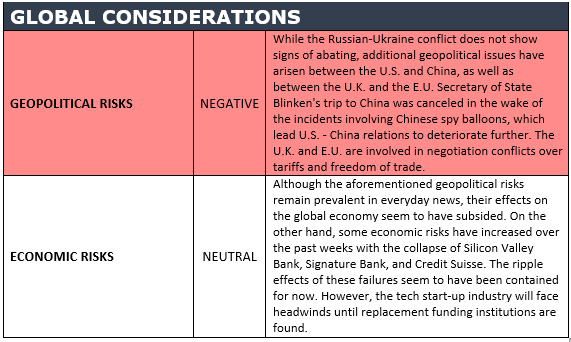

While the markets appear to have moved beyond the recent regional banking crisis, we do not want to ignore other issues showing weakness in 2023 which could again put pressure on banks. Many companies in the U.S. and globally have begun to require a full-time return to work rather than work from home. Office vacancy rates remain elevated compared with pre-pandemic levels; see Chart 2 below from the National Association of Realtors. Like commercial loans, most commercial real estate loans are held by regional banks, and until office vacancy rates recede, pressure will remain on this banking sector. Furthermore, local economies rely on regional bank activities for growth and expansion.

Policy and Politics

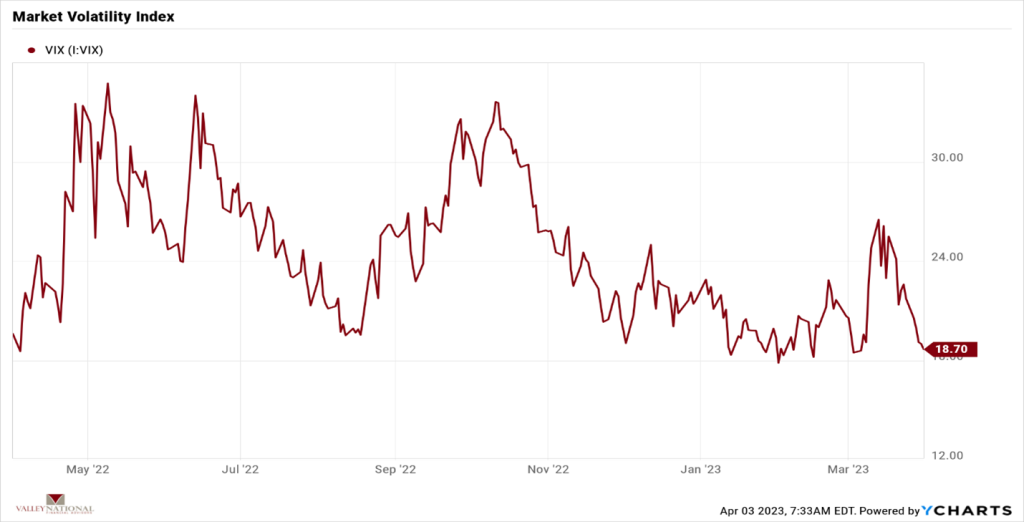

Clearly, all is not well in Washington, and a media firestorm is about to unfold with former US President Trump being indicted. Some may argue that a distracted Washington is good for the markets and the economy as lawmakers are too busy making noise to impart new restrictive or harmful laws; lawmakers can stay out of the way and let the economy do its own thing. A returning calm in the markets can be seen from the VIX (The Volatility Index), which measures the implied expected volatility of the US Stock Market. See Chart 3 below from Valley National Financial Advisors and Y Charts showing the VIX. After a recent spike in the VIX due to the failures of Silicon Valley Bank and Signature Bank, the VIX has fallen back to recent pre-bank crisis levels.

What to Watch

Monday, April 3rd

U.S. Retail Gas Price at 4:30PM (Prior: $3.533/gal.)

Tuesday, April 4th

U.S. Job Openings: Total Nonfarm at 10:00AM (Prior: 10.82M)

Wednesday, April 5th

ADP Employment Change at 8:15AM (Prior: 242,000)

ADP Median Pay YoY (Year Over Year) at 8:15AM (Prior: 7.20%)

Thursday, April 6th

U.S. Initial Claims for Unemployment Insurance at 8:30AM (Prior: 198,000)

30-Year Mortgage Rate at 12:00PM (Prior: 6.32%)

Friday, April 7th

U.S. Labor Participation Rate at 8:30AM (Prior: 62.50%)

U.S. Nonfarm Payrolls MoM at 8:30AM (Prior: 311.00K)

U.S. Unemployment Rate at 8:30AM (Prior: 3.60%)

World famous British Economist John Maynard Keynes said in 1930, “Markets can remain irrational longer than you can remain solvent.” This was a sly way of saying that timing the markets is a fool’s errand. We at VNFA, and others, say that it is “time in the markets rather than timing the markets” that creates true generational wealth. There is always a lot to digest when watching the financial markets. Bulls and Bears exist on both sides of a trade. We remain cautiously optimistic about market returns for 2023 and believe the Fed can moderate inflation without tanking the economy. Opportunities exist for investors, but volatility, while quiet today, could return in short order. Speak with your financial professionals at Valley National Financial Advisors for assistance.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five- and 10- yearreturns are annualized excluding dividends.Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade key economic conditions that we believe are of particular importance to investors.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in Wednesday, 6 PM “Your Financial Choices” on WDIY 88.1FM. Laurie and her guest Bill Henderson, Chief Investment Officer at Valley National Financial Advisors will be discussing: Market Overview.