by Connor Darrell CFA, Assistant

Vice President – Head of Investments U.S.

equities generated their worst week in over a decade as fears that the novel

coronavirus might pose a real threat to economic activity began to spread. In

our view, the market action we observed last week was not based upon fundamentals,

because market participants simply don’t have that type of concrete information

available to them. The selling was, however, unsurprising as the panic that

rippled through the financial system last week was likely amplified by the fact

that equity markets had performed so strongly over the previous year. Throughout

2019, stocks generated strong returns despite minimal growth in corporate

earnings. That happened because the global economy was showing signs of

improvement and the prospects for future earnings growth were increasing. The

coronavirus represents a significant unknown that is eating away at the

positive sentiment that built up throughout last year, and investors should

expect continued volatility in markets as the situation continues to evolve.

But with all of that said, while the

coronavirus itself is new and the public health concerns very real, the fact of

the matter is that what we are seeing in markets is not out of the ordinary. Since

World War II, there have been a total of 26 stock market corrections (this one

makes 27) with an average market decline of 14.3%. Some have been larger, and

some have been smaller. What makes this correction particularly difficult is

that there are so many details we still don’t know about the coronavirus. At

what point will cases reach a peak? How

severe might the economic impacts be, and how widespread? The markets have

reacted strongly to these uncertainties because investors’ appetite for risk

tends to dissipate as more unknown variables enter the equation. In times like

these, we like to remind investors that drastic portfolio changes are unlikely

to add value over the long-term. In fact, there is overwhelming evidence that

most investors make themselves worse off by reacting too strongly to negative

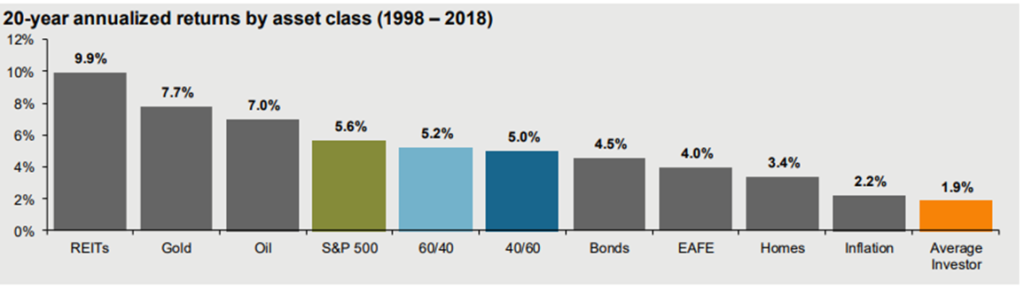

news. The below chart from JPMorgan shows the historical performance of the

average investor compared to a variety of different asset classes. The average

investor has a propensity to act emotionally during periods of market stress

and make efforts to time the markets, which has clearly led to significant

underperformance. In fact, the average investors’ mistakes have caused

portfolio returns to even lag inflation!

Source: JPMorgan Guide to the Markets

The evidence above suggests that investors

should consider the amount of fixed income in their portfolios before making

drastic decisions to exit equities en masse. For those who have multiple years’

worth of withdrawals that can be funded from bond positions, there is little

that should be done to address the pullback.

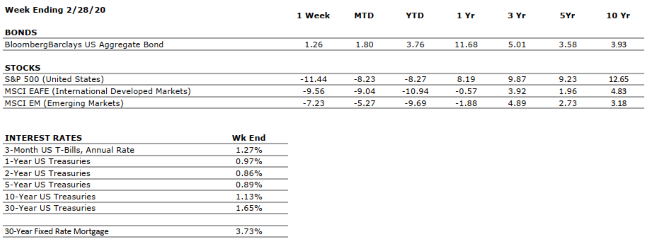

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

U.S. ECONOMIC HEAT MAP

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

VERY POSITIVE

The consumer has been the bedrock of the US economy through much of the current expansion and we have seen little to suggest that this cannot continue.

CORPORATE EARNINGS

NEUTRAL

Corporate earnings growth was weak throughout 2019 as a result of slowing in the global economy and trade policy uncertainty. However, analysts are expecting mid to high single digit earnings growth in 2020, which will be important to sustaining recent levels of equity returns.

EMPLOYMENT

VERY POSITIVE

The economy added 225,000 new jobs in January, exceeding consensus expectations. The report also indicated that the unemployment rate ticked up to 3.6% as a result of more people looking for jobs. The expansion of the labor force should be taken as an additional sign of the confidence Americans have in the health of the labor market.

INFLATION

POSITIVE

Inflation is often a sign of “tightening” in the economy and can be a signal that growth is peaking. Recent inflationary data has increased slightly, but inflation remains benign at this time, which bodes well for the extension of the economic cycle.

FISCAL POLICY

POSITIVE

The Tax Cuts and Jobs Act of 2017 lowered the effective tax rates for many individuals and corporations. We view the cuts as a tailwind for economic activity over the next several years.

MONETARY POLICY

POSITIVE

With the potential threat that COVID-19 poses to the economy, attention is now turning to whether the Federal Reserve will take action following its March policy meeting. Markets are beginning to anticipate a rate cut from the Fed, which would provide support for market in the near-term.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

VERY NEGATIVE

Our geopolitical risks rating is now VERY NEGATIVE as there is more evidence of the coronavirus spreading outside China. However, we think it is important for investors to disentangle the public health concerns over the near-term from the expectations for markets over the long-term. The outbreak remains a near-term issue at this time.

ECONOMIC RISKS

NEUTRAL

Due to low inflation and lukewarm economic activity, central banks around the world remain in a very accommodative stance. We have seen some recent evidence of modest recovery in places like Germany, but overall, we expect global economic growth to remain modest.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Did you see Laurie Siebert on WFMZ 69 News last week? She was interviewed about Women United’s funding for non-profits assisting women, children and families.

Plus, Elizabeth

Wilson’s interview with PICPA went live via the organization’s CPA

Conversations podcast.

This week, Laurie will address more: “Listener Tax Questions.” Listen to the February 19 show devoted to listener tax questions at yourfinancialchoices.com.

The show airs on WDIY Wednesday

evenings, from 6-7 p.m. The show is hosted by Valley National’s Laurie Siebert

CPA, CFP®, AEP®.

by Connor Darrell CFA, Assistant

Vice President – Head of Investments It

was a “risk off” week for global markets as stocks retreated from their highs

and bonds generated positive returns amid growing fears of further spreading of

the coronavirus. Many of those fears were realized over the weekend as evidence

emerged of a substantial increase in the number of cases outside of mainland

China, particularly in Italy, South Korea, and Iran. We have discussed in

previous iterations of The Weekly Commentary that two key areas we are focusing

on with respect to evaluating the risks posed by the virus are contagion and

severity. In our assessment of contagion, our internal discussions have focused

on evaluating whether containment efforts in China would be successful in

keeping the virus from spreading beyond Chinese borders. The significant

increase in cases outside of China over the weekend suggests to us that these

measures have likely failed. As a result, we are increasing our assessment of

geopolitical risks within our economic Heat Map from “Negative” to “Very

Negative”. Below, we provide further

details of our current thinking.

Coronavirus Update: How Should Investors Be Approaching the Issue? In our view, it is becoming increasingly likely that the spread of this disease will reach pandemic status, and many in the scientific community believe it is already at that point. There is of course a significant symbolic weight behind the word ‘pandemic’, and the simple reclassification of the current state of the coronavirus situation has the potential to strike fear into the general public. But by definition, the World Health Organization (WHO) defines a pandemic as simply “the worldwide spread of a new disease.” There is no specific standard that must be met with respect to the severity of the disease or its financial impact. It just needs to spread globally in order to reach the status of pandemic. We think that this is an important point to make, because that leaves open the very real possibility that a disease reaches pandemic status without the need for mass hysteria. In fact, the 2009 strain of H1N1 flu reached pandemic status with more than 60 million cases in the U.S. alone; and few if any of us look back at that pandemic and associate it with intense fear.

As investors, it is imperative that we

disentangle our concerns for the near-term impacts on public health from our

long-term expectations for markets. As a financial planning firm, we are

long-term investors by nature. Everything we do for clients stems from the

financial plan, which is constructed through a process that is designed to

account for bouts of market volatility stemming from exogenous shocks (such as

a pandemic virus) that may happen over the course of the implementation period.

The beauty of the technology used by financial planners when constructing

long-term plans is that we can test the resiliency of our plans across

different scenarios, and those possibilities can be baked into the

recommendations as well as into the construction of client portfolios. In our

view, as long as a financial plan is properly constructed in a way that it

aligns with an investor’s long-term goals, there should be no need for the

investor to become overly concerned with the potential near-term impacts of

these types of risks.

The important assumption that is made in

the paragraph above is that the impacts of the coronavirus will be near-term in

nature. There are multiple reasons that we continue to operate based on this

assumption. The first relates to the

severity of the disease. Looking back through history, there is really only one

pandemic illness over the last 100+ years that was severe enough to

unilaterally push the global economy into recession; and that was the Spanish

Influenza of 1918. When we compare the data currently available on the

coronavirus with what we know about the Spanish Flu, it becomes immediately

clear that the two diseases are miles apart in terms of their severity. There

are some conflicting estimates of the true severity of the Spanish Flu, but

most suggest a mortality rate somewhere in the range of 10-20%, with

significantly higher rates among certain age cohorts. The severity of the

coronavirus remains somewhat difficult to fully evaluate given that it is an

ongoing situation, but the current estimate is a mortality rate somewhere

around 3%. Furthermore, the Spanish Flu is infamous among epidemiologists for

being particularly deadly among younger, healthier adults. The data we have

thus far regarding the coronavirus is that the mortality rates are

significantly higher among older patients with compromised immune systems, much

like the seasonal flu.

The second reason we continue to operate

under the assumption of short-term impacts is recent history. An evaluation of

several of the most recent viral epidemics (including SARS, H1N1, Ebola, and

MERS) reveals that both economic and market impacts of the diseases could be

measured in quarters rather than years. It would take a particularly deadly and

long-lasting disease to alter the trajectory of economic output worldwide for

more than a couple of quarters, and until we see evidence that this disease is

capable of that, we are not sounding the alarm for investors to run for cover. It

will continue to be important for investors to keep themselves informed of new

developments, and it is our intention to provide as many updates as we can

through The Weekly Commentary, but long-term investors should continue

operating through a long-term lens.

There remains the distinct possibility that additional news flow related to the disease could continue to weigh on equity markets, so investors who have near-term spending needs and plan to draw money from their portfolios within a year should make sure they have that money available in a low-risk investment vehicle. But for many others, an adjustment to the investment strategy should not be necessary. If you have specific questions related to your situation or a change in circumstances that warrants further consideration, your financial advisor is available to help you evaluate what the best course of action might be for your unique situation.

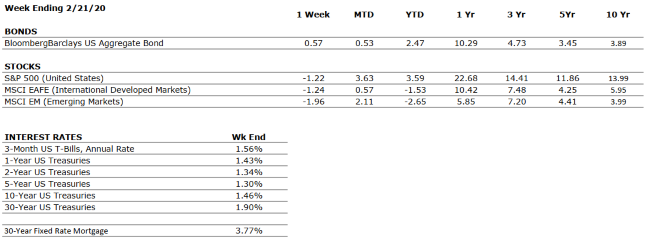

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

U.S. ECONOMIC HEAT MAP

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

VERY POSITIVE

The consumer has been the bedrock of the US economy through much of the current expansion and we have seen little to suggest that this cannot continue.

CORPORATE EARNINGS

NEUTRAL

Corporate earnings growth was weak throughout 2019 as a result of slowing in the global economy and trade policy uncertainty. However, analysts are expecting mid to high single digit earnings growth in 2020, which will be important to sustaining recent levels of equity returns.

EMPLOYMENT

VERY POSITIVE

The economy added 225,000 new jobs in January, exceeding consensus expectations. The report also indicated that the unemployment rate ticked up to 3.6% as a result of more people looking for jobs. The expansion of the labor force should be taken as an additional sign of the confidence Americans have in the health of the labor market.

INFLATION

POSITIVE

Inflation is often a sign of “tightening” in the economy and can be a signal that growth is peaking. Recent inflationary data has increased slightly, but inflation remains benign at this time, which bodes well for the extension of the economic cycle.

FISCAL POLICY

POSITIVE

The Tax Cuts and Jobs Act of 2017 lowered the effective tax rates for many individuals and corporations. We view the cuts as a tailwind for economic activity over the next several years.

MONETARY POLICY

POSITIVE

With the Federal Reserve expected to refrain from any further adjustments to interest rates without a material change in the economic outlook, it is unlikely that changes in Fed Policy will disrupt the economic cycle in the near future. Furthermore, the low absolute level of interest rates remains a positive for markets.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

VERY NEGATIVE

Our geopolitical risks rating is now VERY NEGATIVE as there is more evidence of the coronavirus spreading outside China. However, we think it is important for investors to disentangle the public health concerns over the near-term from the expectations for markets over the long-term. The outbreak remains a near-term issue at this time.

ECONOMIC RISKS

NEUTRAL

Due to low inflation and lukewarm economic activity, central banks around the world remain in a very accommodative stance. We have seen some recent evidence of modest recovery in places like Germany, but overall, we expect global economic growth to remain modest.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

We’re Hiring Entry-Level Professionals Valley National’s Entry Level Professional (ELP) program is designed to hire a select group of Associates who can be immediately integrated into Valley National’s expanding “one-stop” financial planning business model. Ideal candidates are recent graduates of top university programs, or professionals with one to two years of experience, who are looking to establish a long-term career in the Lehigh Valley area. The ELP program will train, educate, and teach each employee the foundations of financial planning, tax preparation, and investment management in order to give them the skills necessary to serve and grow Valley National’s client base. READ MORE / APPLY

Why do I need to complete

a tax questionnaire each year before my CPA can file my return? The

tax questionnaire helps to ensure that your preparer has pertinent information

and data for preparation of your tax return(s). It will also assist them with

referencing your return information for future tax planning and/or tax

questions that might arise after the return is submitted.

The ‘Tax Questionnaire’ contains a series of ‘yes’ or ‘no’ questions about

the prior year with regard to personal information, dependents, education,

healthcare, income, investments, retirement, itemized deductions and credits,

and miscellaneous items related to tax law changes or special situations.

In addition, our VNFA questionnaire

will ask you to indicate delivery preferences for both (i) the supporting

source documents you will provide to us and (ii) how you would like your tax

return(s) delivered to you for review and completion.