Questions can be submitted at yourfinancialchoices.com in advance of the live show. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.

The VNFA Team is thrilled to participate in the 2023 Volunteer Center Holiday Hope Chests, marking a joyous occasion to deliver smiles and laughter within beautifully packed shoeboxes.

The Volunteer Center makes it easy for anyone that wants to participate and bring extra smiles to kids in our community. Team VNFA is happy to share a little joy this year. If you are interested in being part of this amazing cause visit the Volunteer Center of the Lehigh Valley.

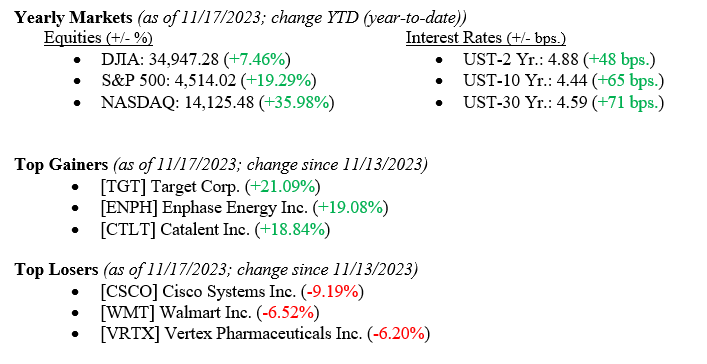

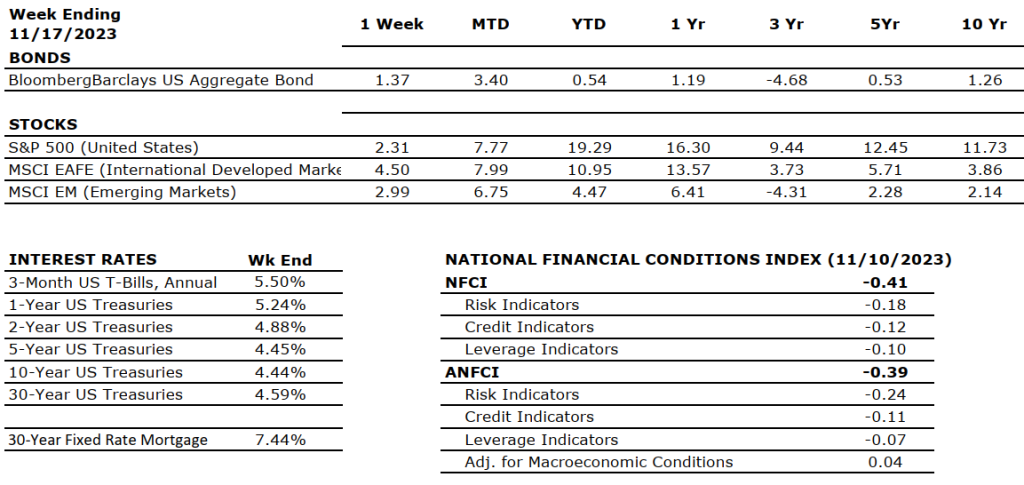

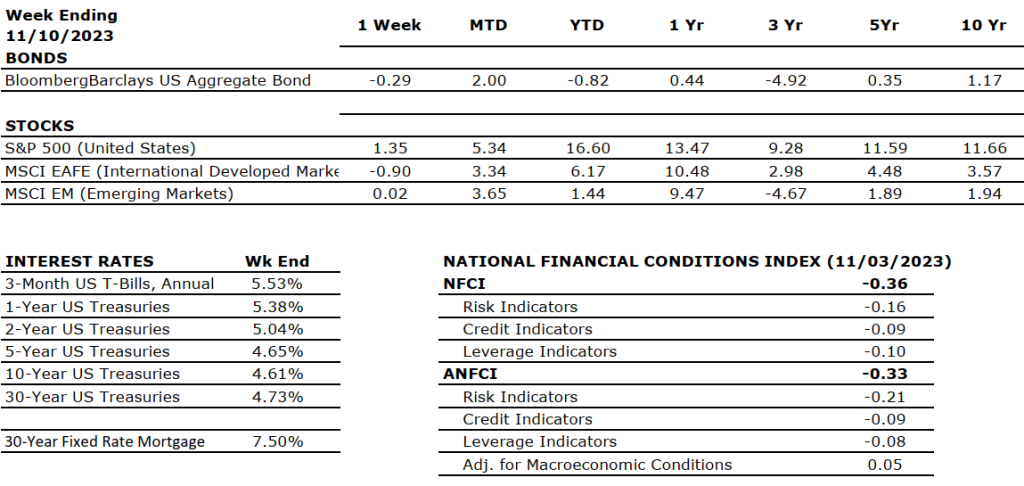

Equity markets notched another modest win last week, with all major indexes reporting gains (see year-to-date numbers below). We typically only point out the major indexes here at Valley National Financial Advisors, but last week saw gains in small capitalization stocks, a sector left out of this year’s market rally. As measured by the Russell 2000 Index, small caps gained +5.5% last week, which also shifted their year-to-date return into positive territory at +3.5%. A rally in small-cap stocks has been long overdue as most of the big gains this year have been in large-cap and even mega-cap stocks like the “Magnificent Seven.” An equity market rally balanced across all sectors and includes deep depth and breadth of all capitalization stocks rather than just large or mega-cap is healthier and more sustainable over longer periods. Bonds also continued their rally, with the 10-year U.S. Treasury falling 18 basis points to close the week at 4.44%.

US Economy

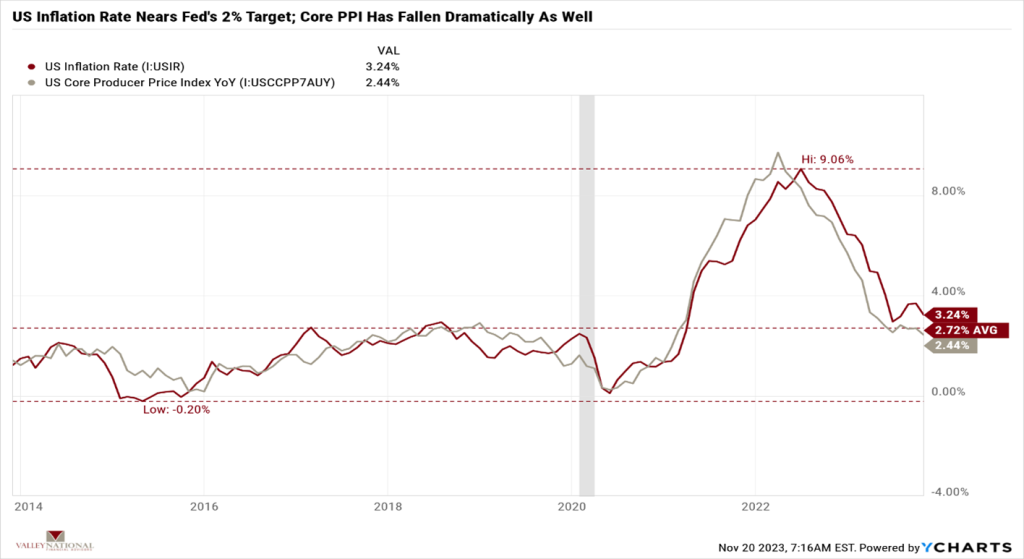

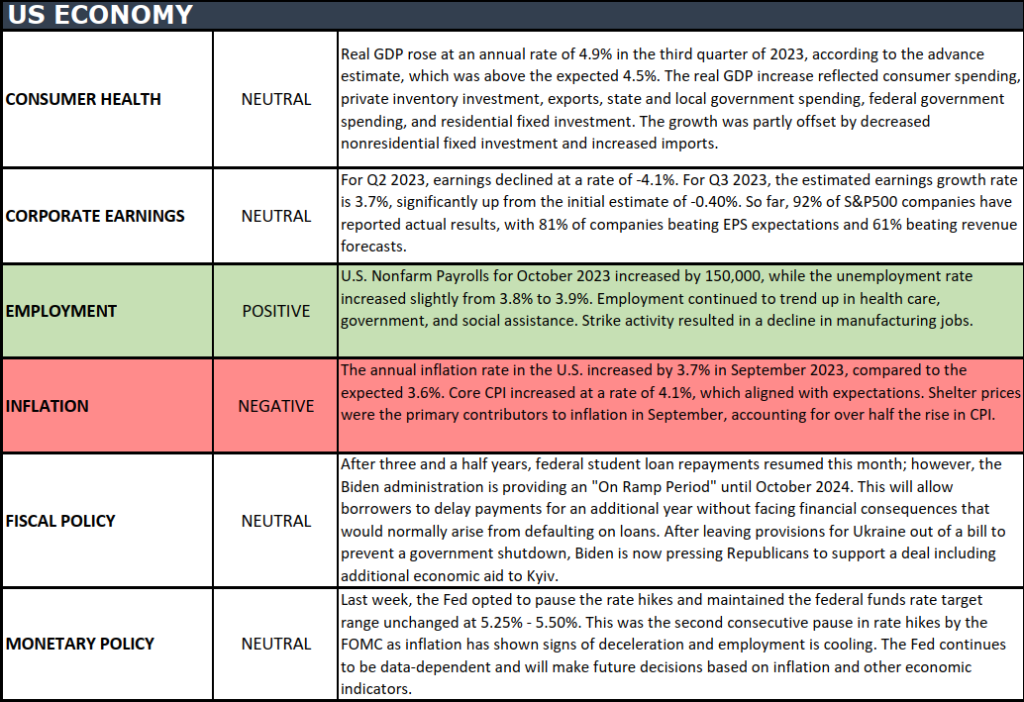

Last week’s equity gains were precipitated by the inflation data released mid-week. The U.S. Inflation Rate fell to 3.24% for October, down from an August 2022 high of 9.06%. See Chart 1 below from Valley National Financial Advisors and Y Charts showing the U.S. Inflation Rate and the U.S. Core Producer Price Index. While the U.S. inflation rate is not yet at the Federal Reserve’s target rate of 2%, the rate has come down dramatically. Furthermore, as we have stated many times here at Valley National Financial Advisors, interest rate hikes take time to work their way through the economy; therefore, even without further rate increases, the inflation rate should continue to track downward from here, given all the tightening that has occurred over the past 18 months. This view, shared by most economists, confirms that the Fed will remain on the sidelines, refraining from further intervention and instead watching and interpreting the data.

Policy and Politics

We have talked about global turmoil often and how global issues create uncertainty and fear—both of which markets hate. The Ukraine/Russia War continues to languish well into its second year. Further, the Israel/Hamas War shows no signs of abating. Thankfully, last week’s APEC Summit in San Francisco and the meeting of Chinese President Xi Jinping and President Biden may help to revive the recently cool relations between China and the U.S., the world’s two largest economies. Both countries are moving past pandemic-related inflation periods and experiencing growing economies, so healthy relationships rather than trade wars or tariff spats are important going forward.

What to Watch

We have a Thanksgiving Holiday shortened trading week so Wall Street will be quiet but Main Street will be all buzz on Friday as the Holiday Season will kick off with Black Friday sales hitting the retail space. Next week Cyber Monday starts and by the end of the week we will have some idea of the consumer’s appetite for shopping and spending as many retailers will report 3rd quarter earnings.

Everyone agrees that the U.S. has avoided a recession in 2023, and the outlook for 2024 is starting to look equally rosy. We remain cautiously optimistic about the markets and the economy, as we have been for over a year. The Fed may be done with interest rate hikes, but even if more hikes are coming, they will be modest, if at all, and minimally impactful. Investors have been rewarded this year for staying the course and remaining invested, a path that is often painful. According to the Nation Retail Federation, consumer spending is expected to be 3-4% higher this holiday season. The U.S. consumer has remained resilient all year and continues to support the economy. Reach out to your financial advisor at Valley National Financial Advisors for help and advice, but more importantly, enjoy the Thanksgiving Holiday Weekend.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five- and 10- yearreturns are annualized excluding dividends.Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

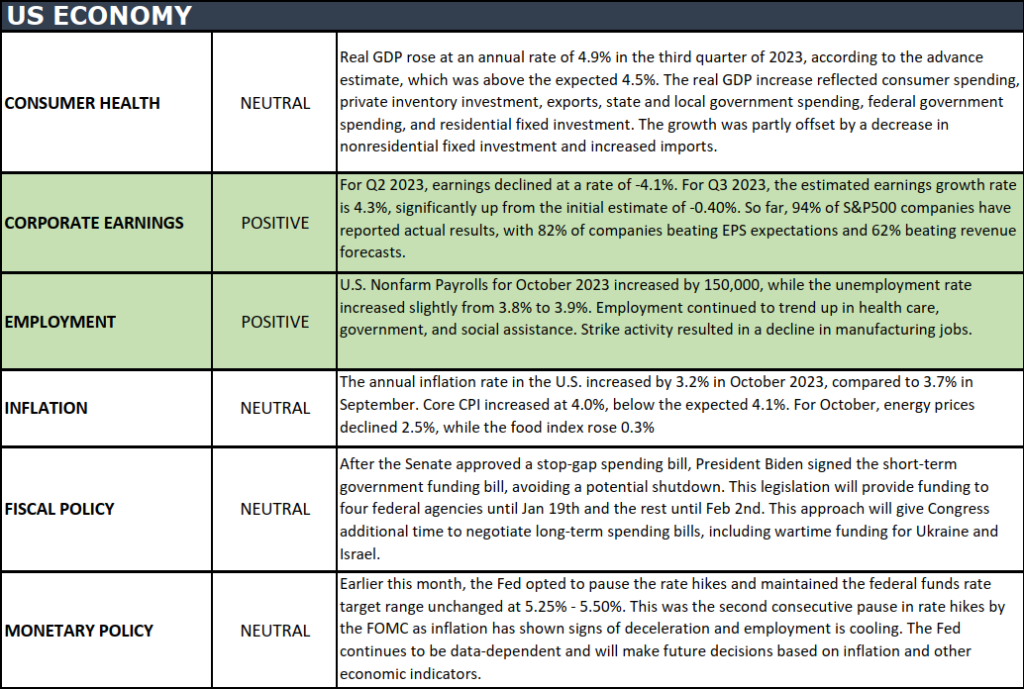

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade key economic conditions that we believe are of particular importance to investors.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in Wednesday, 6 PM for a pre-recorded “Your Financial Choices” show on WDIY 88.1 FM. Laurie will address questions submitted online during the next live broadcast.

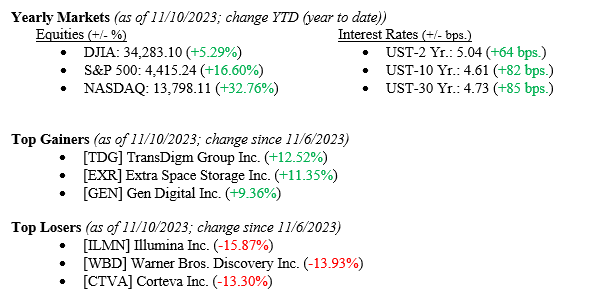

We will talk about market headwinds and tailwinds later in the report, but for now, let us just talk about what the markets did last week and year-to-date to remind investors where we really are and what the markets have done. Last week, the Dow Jones Industrial Average added +0.7%, the S&P 500 Index notched a +1.3% return, and the NASDAQ added +2.4%. These returns pushed year-to-date figures higher for each major index, with the Dow at +5.3%, the S&P 500 at +16.6%, and the mega-tech heavy NASDAQ at 32.8%. Certainly, few investors own only index-based investments or only mega-tech equities. Still, most investors with balanced portfolios own a slice of each and, therefore, have captured their risk-related slice of these market returns thus far in 2023. Bonds moved little last week, with the 10-year U.S. Treasury closing at 4.62%, five basis points higher than the previous week.

Global Economy

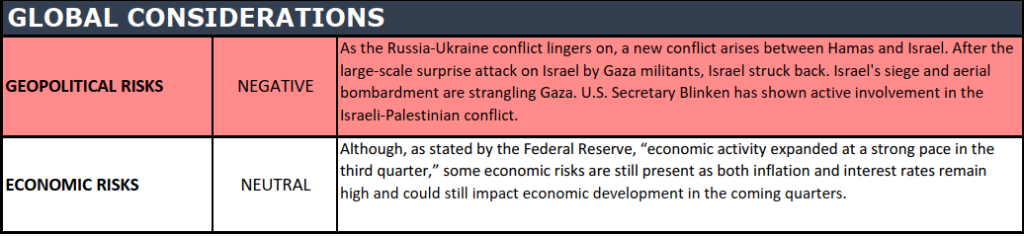

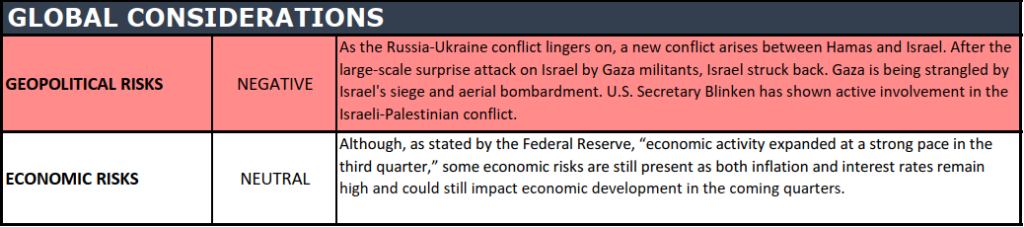

There continues to be sufficient geopolitical global turmoil to worry us at Valley National Financial Advisors. The Israeli/Hamas War shows no signs of abating, while the Russia/Ukraine War has dragged on for almost two years; both wars are overheating the already unsteady markets for oil, natural gas, and some food commodities like wheat and creating an ongoing humanitarian crisis. On the flip side of bad news, Chinese President Xi Jinping will meet with President Biden this week in California in a move that officials on both sides hope will ease tensions in the important bilateral relationship between the U.S. and China. While these three events seem distant from the U.S. equity markets, they individually and collectively add uncertainty to the markets, which everyone who reads The Weekly Commentary knows we hate.

Policy and Politics

In the continuing saga of Washington, DC’s version of “The Gang That Couldn’t Shoot Straight,” we are three days away from another government shutdown. The newly elected Speaker of the House, Mike Johnson, must bring together the contentious parties from both sides of the aisle to pass a budget bill before Friday, November 17, to avoid a government shutdown. While a lot of the actions and bargaining going on in Washington are in partisan brinkmanship, the farce of a looming U.S. Government shutdown has real market implications. For example, last week, the credit rating agency Moody’s lowered the outlook on the U.S. Credit to “negative” from stable, citing large fiscal deficits and declining debt affordability. Moody’s move followed a rating downgrade by another rating agency, Fitch, to A.A. from AAA earlier this year. Although the actions by rating agencies do not have any real market implications, as U.S. Treasury bonds still represent the “risk-free” market measure, moves like this slowly chip away at investor confidence and place a finer negative global spotlight on the U.S.

What to Watch

Monday, November 13th

4:30PM: Retail Gas Price (Prior: $3.52/gal.)

Tuesday, November 14th

8:30AM: U.S. Consumer Price Index MoM/YoY (Priors: 0.40% | 3.70%)

8:30AM: U.S. Core Consumer Price Index MoM/YoY (Priors: 0.32% | 4.13%)

Thursday, November 16th

8:30AM: Initial Claims for Unemployment Insurance (Prior: 217,000)

10:00AM: NAHB/Wells Fargo U.S. Housing Market Index (Prior: 40.00)

12:00PM: 30-Year Mortgage Rate (Prior: 7.50%)

Friday, November 17th

8:30AM: U.S. Building Permits (Prior: 1.473M)

8:30AM: U.S. Building Permits MoM (Month Over Month) (Prior: -4.41%)

8:30AM: U.S. Housing Starts (Prior: 1.358M)

8:30AM: U.S. Housing Starts MoM (Prior: 7.01%)

We have focused on quite a few negative notions this week, which we know is a bit out of character, but there are plenty of positive things to highlight. Contrary to most economists, the U.S. has avoided a recession in 2023, and it looks like 2024 will continue our growth pattern, at least into the first half of the year. Further, inflation has come down from 9% to 3% in just over a year, which means the Fed and most other global central banks are nearing completion in their interest rate hiking cycle. Corporate earnings remain healthy, with most companies reporting earnings that beat Wall Street expectations. Lastly, while the consumer may be getting understandably tired of supporting the economy with their spending, we expect consumer spending to continue well into 2024, especially during the 2023 holiday season. The markets are efficient and always look well into the future rather than watching the past. Investors would do well to do the same. Reach out to your financial advisor at Valley National Financial Advisors for help or questions.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five- and 10- yearreturns are annualized excluding dividends.Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade key economic conditions that we believe are of particular importance to investors.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.