People

with a financial adviser say they aren’t just better with money – they’re

happier with life overall. We think so, of course, but

don’t take our word for it… read (and share) this Business Insider

article covering the results of a Northwestern Mutual survey. READ MORE

by Connor Darrell

CFA, Assistant Vice President – Head of Investments As

was widely anticipated by markets, the Federal Reserve opted to reduce its

target interest rate by 0.25% last week. However, the dovish pivot was not

enough to support equity markets, which ended the week in a downswing following

a series of tweets from President Trump which indicated he was moving forward

with an additional round of tariffs on Chinese goods. That this announcement

came just one day after the Federal Reserve’s interest rate decision is likely

no coincidence, as the Fed’s accommodative stance will provide the President

with greater confidence that the economy can withstand the consequences of

upping the ante with the Chinese.

With the confirmation that interest rates

would slide downward and the increase in equity volatility stemming from

President Trump’s tariff announcement, the bond market managed a small rally

last week. The Barclays Aggregate Bond Index is now in the midst of one of its

strongest years since 2011.

Global Manufacturing in Contraction Purchasing

Managers’ Indices (which utilize survey data to evaluate business confidence

and manufacturing activity) released last week revealed that global

manufacturing activity remains challenged by the uncertainties posed by the U.S.-China

trade dispute and Brexit negotiations. The U.S. PMI remains the only major

region that has held above 50 (a critical level which separates expansion and

contraction), though it has declined materially over the last several quarters.

PMIs in the eurozone, Japan, and China all remained below 50 last month,

indicating that these manufacturing markets are in contraction.

Manufacturing is far more cyclical than

top line economic growth, but the reduction in global manufacturing activity

that we have observed over the past year is a symptom of the toll that mounting

geopolitical uncertainties are having on business decisions. If businesses’

reluctance to invest in production permeates into hiring decisions, it could begin

to impact labor markets and accelerate the arrival of the next recession. Given

the relative health of the U.S. economy and the potential for these

uncertainties to be lifted by a simple handshake between Presidents Trump and

Xi, this scenario looks a long way from playing out. But for investors who have achieved double

digit returns in a year where the economic backdrop has continued to weaken,

this type of data should not be ignored and may represent a reminder of the

prudence of maintaining discipline and avoiding the urge to chase returns

during late cycle investing.

Our VNFA team is “gearing up” for another Community Bike Works SPIN-A-THON fundraiser. Teams of 4-8 riders will raise a minimum of $1,000 and tag-team cycle for 3 hours at LVHN Fitness on September 28. Learn more about the cause and how to participate or lend support at Community Bike Works’ crowdrise web page.

VOTE FOR US? VNFA is one of the nominees for the 2019 Lehigh Valley Business Reader Rankings Award in the category of Wealth Management. If you feel we are worthy, click here to vote. Plus, check out all the other worthy LV businesses in each category.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

US ECONOMIC HEAT MAP

The health of the US economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

CONSUMER SPENDING

A

Our consumer spending grade remains an A. Surveys of US consumers continue to indicate that the consumer is in a strong position, and last week’s GDP provided further evidence of healthy consumer spending.

FED POLICIES

B+

We have increased our Fed Policies grade to a B+ after Jerome Powell commented that “a number” of Fed decision makers believe that the case for a rate cut in the near future has strengthened. Markets are expecting a rate cut this week.

BUSINESS PROFITABILITY

B-

As was anticipated, first quarter earnings revealed a tapering of growth. Expectations for Q2 earnings are also relatively low. However, this is largely a result of the fact that YoY comparisons are made relative to a historically strong 2018.

EMPLOYMENT

A

The US economy added 224,000 new jobs in June, beating consensus estimates by a wide margin. We continue to view the jobs market as very healthy.

INFLATION

B

Inflation is often a sign of “tightening” in the economy, and can be a signal that growth is peaking. The inflation rate remains benign at this time, but as the economic cycle continues to mature, this metric will deserve our ongoing attention.

OTHER CONCERNS

INTERNATIONAL RISKS

6

We have adjusted our international risks rating down one notch to a 6 following a recent cooling of rhetoric in the US/China trade negotiations. While new developments are still likely to create short-term volatility in markets, both sides have an incentive to reach a deal.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

529 Plan FAQ Jaclyn Cornelius, CFP®, EA, spends five minutes answering the most frequently asked questions about 529 plans as a savings and investment tool. WATCH NOW

RELATED VIDEO: 529 PA Tax Benefits

Jaclyn Cornelius, EA, CFP®, offers some insights and options Pennsylvania taxpayers may want to know about 529 plan contributions and deductions. WATCH NOW

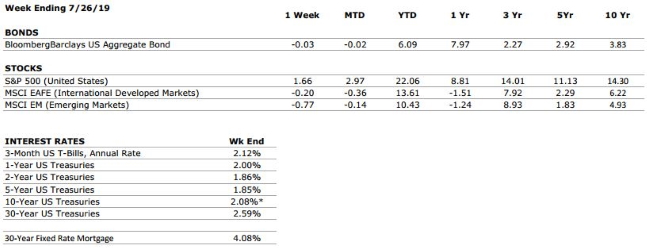

by Connor Darrell CFA,

Assistant Vice President – Head of InvestmentsThe S&P 500 led global equities forward last week as the market’s focus

began to turn once again toward monetary policy. In Europe, the ECB indicated

that it would reduce short-term interest rates in September in an effort to

stimulate the eurozone’s softening economy. Meanwhile, the Federal Reserve is

widely expected to take a similar course of action when it meets this week.

Also weighing on global equity returns was

mounting uncertainty surrounding the ongoing Brexit saga. Boris Johnson, who

has pledged to deliver on 2016’s Brexit referendum with or without a concrete

deal in place, won the race to become the next Prime Minister of the United

Kingdom.

All Eyes on the Fed At

this week’s meeting, the Federal Reserve is widely expected to cut short-term

interest rates by at least 25 bps. However, the bond market has had this

expectation baked into current prices for several weeks now, and any market

movements are likely to be driven by the forward outlook for monetary policy,

which will likely be discussed during the press conference on Thursday. At

present, markets are anticipating more than two rate cuts before the end of the

year.

Whether or not the market’s expectations

for monetary policy are met will be largely contingent upon the strength of

economic data between now and the end of the year. Last week, it was reported

that the U.S. economy expanded at a rate of 2.1% annualized, which was on the

upper range of consensus expectations. That growth was supported by very strong

consumer spending, which more than offset a slight decline in business

investment. Business investment has remained an area of weakness in recent GDP

figures around the world (primarily as a result of uncertainty surrounding

trade policy), but the strength of the consumer continues to help keep the U.S.

economy on a solid foundation. Furthermore, with face-to-face trade talks

resuming between the U.S. and China this week, there is some optimism that

progress can be made. Any meaningful progress on trade would likely improve

business confidence and could begin to push business investment trends back in

a positive direction.

Our HR Director, Ashley Santiago

has earned her SHRM-CP. This professional distinction, given by the Society of

Human Resources Management, requires an existing level of education and

experience, the completion of an intensive course and exam covering knowledge-

and competency-based questions.