Laurie can

address questions on the air that are submitted either in advance or during the

live show via yourfinancialchoices.com.

Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.

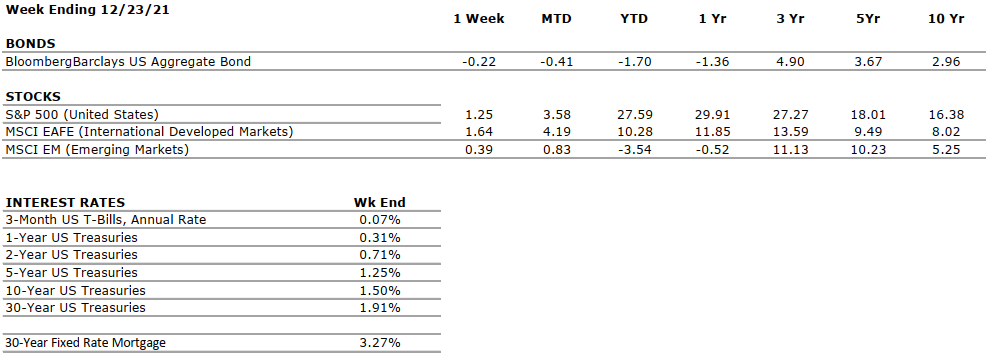

by William Henderson, Vice President / Head of Investments A shortened Christmas Holiday week pushed markets higher even in the face of increased omicron variant threats and global travel snafus. The Dow Jones Industrial Average rose +0.2%, the S&P 500 Index gained +1.2%, and the NASDAQ gained a healthy +3.1%. Further, year-to-date returns remain well into near-record territory for 2021. Year-to-date, the Dow Jones Industrial Average has returned +19.7%, the S&P 500 Index +27.6% and the NASDAQ +22.2% giving us solid returns across all market sectors. With the healthy returns in risk assets, as expected, bonds sold off. The 10-year U.S. Treasury bond rose by nine basis points to close the week at 1.50%. The fixed income markets react as quickly as the stock market to good news or bad news and each market reminds us why investors own each asset class. Equities remain a portfolio’s return generator and bonds remain a portfolio’s risk management tool.

As mentioned above, the week gave

us mixed news on the pandemic and its

impact on the U.S. economy and financial markets. Cases of the omicron variant

spread rapidly in pockets of

the country, and the government

announced an initiative to distribute COVID-19 tests to the public for

free.

Lastly,

regulators

approved two new pills that will be available by prescription for those who are

sick with COVID-19.

In a revision to last quarter’s

GDP, the U.S. government reported economic growth last quarter was slightly

stronger than it had estimated previously. In its final estimate released last

Wednesday, GDP growth in the third quarter was 2.3%,

an

upward revision from the original release of 2.1%.

By comparison, GDP accelerated at annual rates of 6.4% and 6.7% in the first

and second quarters of 2021,

respectively. A

report on Bloomberg showed that Christmas

shopping, both in person “bricks and mortar” and online was much stronger than

2020. According

to the report by Mastercard SpendingPulse, U.S.

holiday sales jumped 8.5% from last year as consumers spent more money on

clothes, jewelry, and electronics. Sales

boomed across the board during the holiday season defined as November 1 to

December 24. Many consumers were savvy

shoppers and started earlier than normal,

most likely due to widely reported supply chain concerns,

which in the end, were largely unfounded rumors as most retailers were

plentifully stocked with goods.

As we move into 2022, it is

important to keep the markets in perspective. Certainly, central

banks globally are taking a more hawkish tone and higher short-term rates are a

given next year, but that information is already priced into equities. Two

questions are typically bantered about: 1) Is the market going higher or lower

today? 2) Is today a good day to buy (invest)? And

my answer to both questions is always the same – YES. Yes,

the markets will go up or down today and YES, today is a good day to buy

(invest). Long-term positive returns on

investment portfolios are driven by long-term investment plans and a commitment

to sticking to your investment plan. We’ve

seen this all year as the market

rallies

back as quickly as it sold off. Perspective

and commitment are what matter the most.

by Thomas M. Riddle, CPA, CFP®, Founder & Chairman A group of decision makers at the Federal Reserve Bank (the “FED”) meets periodically during the year. Last week’s meeting led me to strongly suspect the FED will raise interest rates sometime in 2022 and continue through 2023. This action will increase interest rates on variable rate loans such as home equity loans. The reason for the increase is that many home equity loans use a formula to compute interest due on the loan such as the Prime Rate (currently 3.25%) plus 1%, for example. During 2022, some experts are forecasting the Prime Rate may rise from 3.25% to 3.75% – 4%. And, to 5% by the end of 2023. That means borrowers may see their variable rate home equity loan rate soar to 6% during the next two years.

ALERT: Variable rate home equity loan rates will rise in

2022 and 2023 so now is the time to refinance using a fixed rate home equity

loan. Another viable option is to combine the variable rate home equity

loan with your mortgage and consolidate into a single fixed rate

mortgage. Not every bank offers a fixed rate home equity loan. I have

surveyed banks in the Lehigh Valley, and I have located two banks which

do. Contact me at triddle@valleynationalgroup.com

and I will be happy to share the information with you.

PERSONAL NOTES: My family and I are well. My two

daughters, their husbands along with my four grandchildren live only 10 miles

away (all in the same development). There is a well-worn groove in the

road between my house and theirs! Grandchildren are powerful magnets.

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

U.S. GDP growth decelerated to a 2% annualized pace in Q3. The slowdown was driven primarily by supply chain constraints. Economists expect a modest acceleration in Q4. Early high-frequency data (shopping, travel, movie ticket sales) is showing some slowing. Holiday retails sales numbers will be important to gauge consumer behavior.

CORPORATE EARNINGS

POSITIVE

Huge year-over-year increases in corporate earnings are likely to decelerate in 2022 as CapEx begins to have an impact on income statements. The supply chain disruptions are waning but we may have to take omicron shutdowns into account.

EMPLOYMENT

POSITIVE

The unemployment rate is down to 4.2%, as of November. The labor market is very tight at present as many employers, particularly in the Leisure and Logistics sectors, are struggling to fully staff because the labor participation rate remains below pre-COVID levels. The labor shortage is one of the causes of the global supply chain glut.

INFLATION

NEGATIVE

CPI rose 6.8% year-over-year in November, the highest increase since 1982, driven by the global supply chain backlog and continued consumer pent up demand. Will inflation be transitory or permanent? Powell may remove “transitory” from his testimony this week.

FISCAL POLICY

NEUTRAL

The Build Back Better Bill has been pushed into 2022 in a scaled back $1.8 trillion version as Senator Manchin continues to hold back support. The economy seems to be digesting a new world where fiscal policy is no longer considered an economic stimulus.

MONETARY POLICY

POSITIVE

By early 2022, all Fed bond purchases will halt. The Fed’s bond buying program works to keep interest rates low. Once tapering ends, rate hikes follow. Mid-June or sooner for rate hike?

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEUTRAL

The new omicron COVID-19 variant has shown up in many parts of the world. This strain seems less virulent and more reactive to boosters so its impact it still yet to be calculated. A rebound in travel and leisure now seems unsure.

ECONOMIC RISKS

NEUTRAL

Supply chain disruptions are hampering the economy; however, demand remains very strong. While global logistics are operating far below normal efficacy, it appears the supply chain is slowly improving and may reach normalcy by mid-to-late-2022.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

APTC / EIP Information Letters The IRS announced that it would issue information letters (6419) to Advance Child Tax Credit (APTC) recipients starting in December and to recipients of the third round of the Economic Impact Payments (EIPs) (known as the stimulus payments) at the end of January. Using this information when preparing a tax return can reduce errors and delays in processing. The Service also urged taxpayers receiving these letters to make sure they hold onto them to assist them in preparing their 2021 federal tax returns in 2022.

Required Minimum Distributions (RMDs) Effective 1/1/2022, the IRS will begin using a new table when calculating RMDs from your tax-deferred retirement plans. Once you reach age 72 (or age 70 ½ if you reached 70 ½ before 1/1/2020), you are required to take a distribution from your accounts based on the account balance at the end of the preceding calendar year and an IRS tables based on your age. The new table lowers the amount you are required to distribute annually. (You may always take a distribution larger than this amount, if needed.) The goal of lowering the required distribution is to provide retirement funds to participants for longer due to the increasing life spans.

Tune in

Wednesday, 6 PM for a recorded episode of “Your Financial Choices” with Laurie

Siebert on WDIY 88.1FM. Questions submitted online at yourfinancialchoices.com will be

addressed during the next live show.