Tax returns that were extended for partnership and S-Corps are due on September 15 and for individuals on October 15.

The first income tax in America was created in 1861 during the Civil War as a mechanism to finance the war effort. It was repealed 10 years later. In 1913, Wyoming ratified the 16th Amendment, providing the three-quarter majority of states necessary to amend the Constitution. The 16th Amendment gave Congress the authority to enact an income tax. In 1914 The Bureau of Internal Revenue (know as the IRS today) released the first Form 1040.

Valley National Services was incorporated on October 27, 1988 – 30 years ago – adding to the one-stop suite of services you know today as Valley National Financial Advisors.

Valley National Financial Advisors and the Certified Financial Planner (CFP®) Board of Standards were both founded in 1985. VNFA as a local, independent firm with the mission to help people achieve their long-term financial goals by providing solutions in as many areas as possible. The CFP Board as a 501(c)(3) non-profit organization that serves the public interest by promoting the value of professional, competent and ethical financial planning services.

In 1995, the National Commission for Certifying Agencies (NCCA) accredited the CFP Board’s certification program, the first such accreditation for a non-health related certification in the U.S. Individuals who have passed the tests of the CFP Board are known as Certified Financial Planner ProfessionalsTM – Valley National currently has eight Financial Advisors with CFP® certifications.

Why does this matter? It matters to us and to our clients that we uphold the fiduciary standard of care requiring a financial adviser act solely in the client’s best interest when offering personalized financial advice. It is at the very core of our team’s values and one of the reasons we maintain our independence.

Currently, several states are considering legislation that would bar professionals of any type from using the word “certified” or “registered” in their titles unless the title has been conveyed by a state-sanctioned board or agency. What would this mean for the CFP? We will follow that closely and keep you informed. We are certain that no matter what may happen with the titles in the future, our commitment will always be to our clients first.

5 Reasons You May Need A Wealth Manager How do you know when it is time to forge a professional partnership with a Certified Financial Planner™ professional? The team at Valley National Financial Advisors offers five scenarios. READ MOREat LehighValleyStyle.com

Financial Checklist for New Dads and Moms by Michael A. Ippoliti, MBA, CFP®, Vice President

1) Make sure your child has a Social Security number.

If you checked “yes” and supplied the appropriate information when applying for your baby’s birth certificate, the Social Security number should be on its way. If for some reason you didn’t, you can apply at an SSA office, but you’ll have to provide proof of your child’s U.S. citizenship, age and identity, as well as your own identity.

2) Get health insurance right away. If you have insurance through your work, notify your employer as soon as your child is born. In the meantime, review your options to make sure you have the best combination of deductibles and coverage.

3) Evaluate Your Emergency Reserve An emergency fund is always important and more than ever when you have a child. Strive to have enough cash in an easily accessible account to cover three-to-six months of necessary expenses.

4) Create a will and Powers of Attorney for financial and health decisions Even if you don’t have a lot of assets, a will is essential to name a guardian for your child. It doesn’t have to be a complicated document, but I’d suggest consulting with your family attorney. If it’s not in writing, the state could decide who would care for your child.

5) Start saving for education. Everyone thinks about the enormous cost of college, but what if you want to send your child to private elementary or high school? Fortunately, with the new tax law, 529 accounts can now be used for all three with certain limitations. A 529 is a great, tax-advantaged way to save—and provides an easy, tax-smart way for grandparents to chip in as well.

If you or a veteran or surviving family member of a U.S. veteran released from service due to injuries sustained in combat, you may be able to recover a substantial tax refund. “For 25 years, between 1991 and 2016, a computer glitch at the agency caused non-taxable disability severance payments to be subject to income taxes, a Defense Department official told CBS MoneyWatch. The government is now trying to help veterans or their survivors recover these old overpayments, each of which is expected to result in refunds of $1,750 or more.”READ MORE FROM CBS NEWS

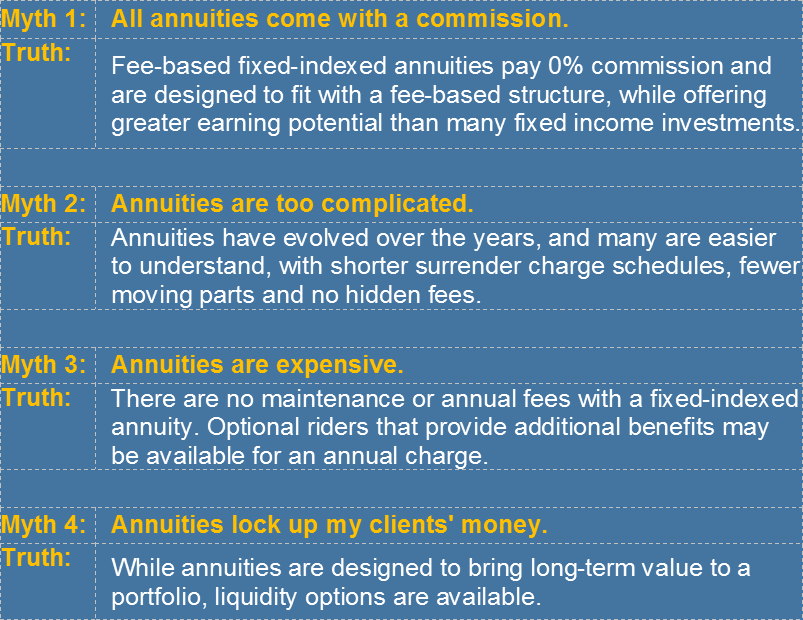

by Roxie Munoz, CLU, FLMI, Assistant Vice President / Manager, Insurance Services

Unique Benefits of Fixed Index Annuities A sound retirement plan can resemble a relay race. Each phase, or leg, has its own needs that demand their own strategy or product strengths to best build, sustain and deliver financial solutions. Fixed index annuities offer unique benefits that work in concert to help you reach your retirement goals.

Protection: A central benefit of fixed index annuities is a level of protection that underpins the product’s guarantees. When you purchase a fixed index annuity, not only is your principal protected, so is any interest credited to your contract. No matter what the index does, your return will never be less than zero due to index volatility.

Tax Deferral: Throughout the accumulation phase, money can grow tax-deferred. This means, while your principal and any interest credited are protected from volatility, the tax-deferral benefit provides the opportunity for compounded growth over time—further bolstering your resources for when you choose to take an income.

Liquidity Options: As a component of a strategic income plan, a fixed index annuity provides added income flexibility through a variety of liquidity options. They offer liquidity features that give access to the contract value. Typically, 10 percent of the annuity’s value annually is available for free withdrawal during the surrender charge period. Many products also have increased or full access to the contract value for qualified care needs.

Guaranteed Income: A study found 78% of workers are looking for lifetime income in retirement. This goal is followed closely behind by 76% who are looking for stability of income.1 Once the accumulation period ends, you can begin receiving distributions from the guaranteed income sources you generated. You can choose to receive a lump-sum payment, fixed amount payments over time, or annuitized payments for life. With an income rider option, you have additional flexibility for guaranteed lifelong income payments. These fail-safe measures can be added to a fixed index annuity contract, securing payments that cannot be outlived, with joint payout options for a spouse.

Take Care of Loved Ones: In addition to helping generate and sustain a stable income throughout your life, with fixed index annuities you can also establish a clear transition of assets to a named beneficiary. Whether death occurs during the accumulation or distribution phase of the annuity, the annuity guarantees direct payment to the named beneficiary. Depending on the contract, these payments may be in the form of a lump-sum, series of payments or lifetime payments. The contract may also help bypass probate, saving time and expense in the process.

Benefits You Can Rely On. Any of these benefits on their own are important in retirement. But, it is their interdependent strengths that can help fund retirement from start to finish. Contact our office today to determine if an annuity should be part of your financial plan.

Sources: Indexed Annuity Leadership Council, The State of America’s Workforce: The Reality of Retirement Readiness. White Paper, 2018

by Jessica Goedtel, Senior Associate If you are on a high deductible health plan, you may have access to a Health Savings Account (HSA). Recently these have become very popular due to their “triple tax exempt” nature. First, if you contribute to your account via payroll, contributions will come out pre-tax. Alternatively, you can make after-tax contributions but receive a deduction on your tax return.

Second, you are not taxed on any investment growth in the account. Some plans offer a variety of investment options, others may work as a simple savings account. Check with your plan administrator to see what options are available to you.

Third, any distribution for qualified medical expenses is not taxable. And, unlike a Flex Savings Account (FSA), the balance can be carried over each year. If you are nearing retirement this could be an excellent strategy to save for medical expenses.

The contribution limits for HSAs for 2018 are $3,450 for a single person plan, and $6,900 for a family plan. If you are over the age of 55, you can increase your contribution by $1,000. One important item to consider is that once you become eligible for Medicare at age 65, you can no longer make contributions.

If used correctly, an HSA can be a very powerful tool in your financial plan.

FROM THE HEADLINES Source: Associated Press, June 25, 2018

Pennsylvania OKs new college saving grants for newborns

HARRISBURG, Pa. (AP) — Pennsylvania is starting a program proposed by state Treasurer Joe Torsella to provide college savings accounts for newborns, beginning with a $100 grant.

Torsella said Monday the program will be open to any child starting next year who is a Pennsylvania resident at birth or adopted by a Pennsylvania family. Parents will be notified about the account set up for them.

Gov. Tom Wolf signed the program into law Friday.

It’s projected at a $14 million annual cost for an average of 140,000 births per year and Torsella says it can be financed by donations and surpluses in Pennsylvania’s existing college savings program.

The Treasury Department will invest the money and income it earns can be spent on a range of post-high-school education needs until the child reaches age 29.

by Mae Gerhart, Tax / Financial Planning Professional Miscellaneous Itemized Deductions were one item that was nixed in the Tax Cut and Jobs Act of 2017. While the deductions may still be allowable on your state and local returns, you are no longer able to write off unreimbursed employee business expenses on your federal return.

Unreimbursed business expenses are defined as an expense that is common and accepted in your trade or business and helpful or appropriate for your business. These expenses may include…

Transportation costs associated with using your personal vehicle for work-related reasons such as a business meeting away from your regular workplace, visiting clients or customers, or traveling between your regular place of business and a second office. The rate for unreimbursed business mileage is 54.5 cents per mile for 2018. You may also deduct the costs associated with parking or tolls. Regular commuting expenses are not deductible.

Travel expenses such as the cost of airline tickets, checked bags, a rental car or cab rides, meals while traveling, or a hotel stay for a work-related conference or out of state client or vendor meeting.

Other business expenses such as business cards, subscriptions to trade and business publications, professional dues (not for recreation, entertainment or pleasure) home office expenses, necessary tools and equipment, hospital scrubs, steel toed boots, union dues, business gifts (up to $25 per client), and work-related education that does not make you eligible for a new position.

If your employer has an accountable reimbursement plan, you may be able to provide receipts or mileage logs documenting these expenses to your employer for reimbursement. Whether your employer participates in an accountable reimbursement plan or you would be deducting it on your state and local returns, you will need to keep adequate records to substantiate the expense. Your records should include the date, amount paid, description of the expense, the business purpose, and other persons in attendance, if any.

Talk to your tax professional about planning strategies around changes in the tax law and how they may affect your individual situation.

by Joseph F. Goldfeder, CFP®, Assistant Vice President Looking to buy a home? How do you know if you’re getting the best rate?

If you’re planning on buying a home soon, one of the most important steps is obtaining a mortgage. It is probably one of the first things you should check off your list. Too often, eager home buyers neglect to search for the best rate possible. Many avoid comparing lenders and go with the first option they can find, which could end up costing borrowers more in the long run. There are many factors that go into your rate that you can’t control, but there are also some ways for you to ensure that you’re getting the best rate possible. Let’s review.

Credit Score One major piece that you can control when it comes to getting the best rate, is ensuring that your credit score is in good shape. Lenders use your credit score to predict how reliable you will be in paying off your loan. The general rule of thumb is the higher your credit score, the lower the interest rate. If you’re looking into purchasing a home, be sure to look into your credit score ASAP and take action if needed. There are many providers such as Credit Karma, which will offer your credit scores for free.

Loan Type and Term When you begin exploring mortgage options, you should keep in mind that the type of loan you choose may have an effect on your rate. Typically, adjustable-rate mortgages have a lower interest rate than fixed-rate mortgages. Adjustable-rate mortgage loans have an interest rate that will “adjust” periodically. They are traditionally structured to change every year after an initial period of remaining fixed. Fixed-rate loans are just that, fixed for term of the loan. Loan term is another big factor. Typically, shorter-term loans have lower rates and lower costs, but higher monthly payments. It is important to weigh all aspects of your loan; type, term, and rate before making a decision.

Down Payment Another factor in your rate is your down payment. Under normal circumstances, the higher your down payment is, the lower your rate will be. This is why people typically like to build a strong savings before they look into buying a home. Usually, 20 percent or more for a down payment can keep you at a lower rate. If your down payment is lower than 20 percent, you face the possibility of a higher interest rate.