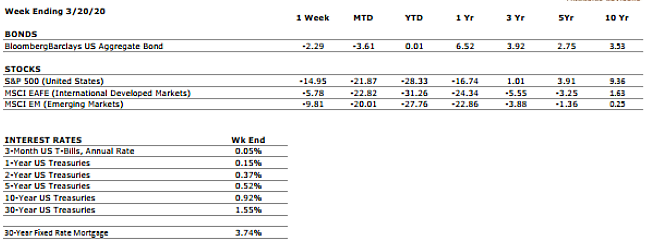

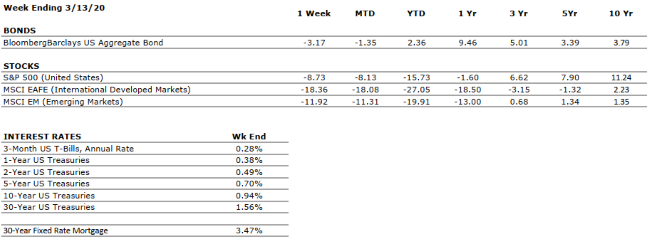

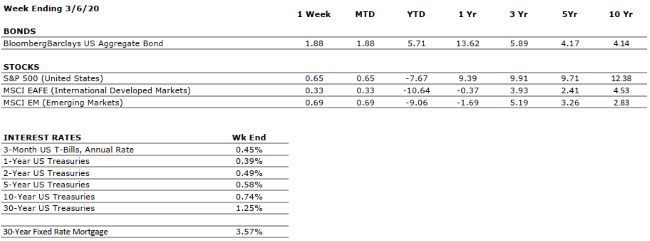

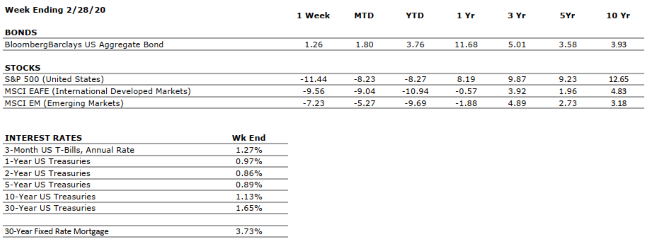

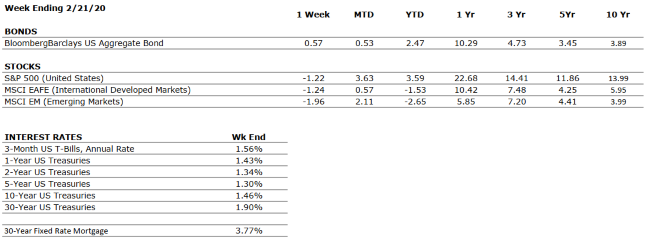

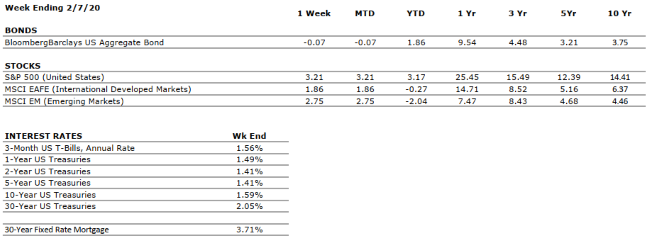

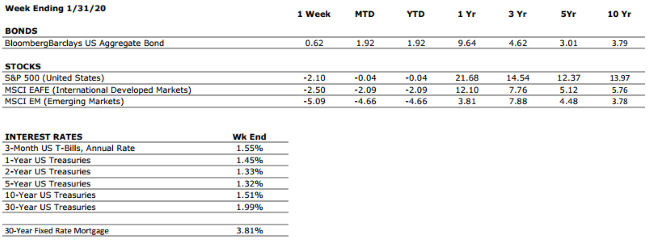

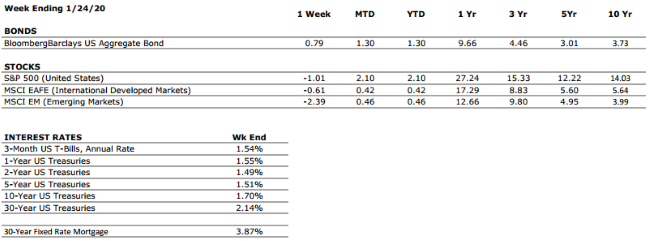

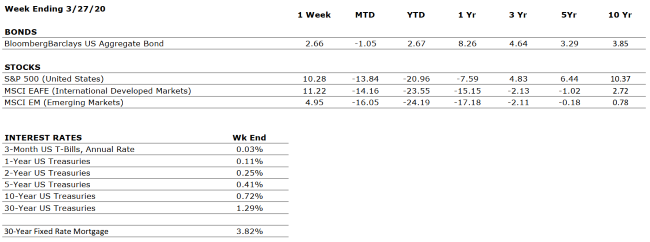

THE NUMBERS

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

|

US ECONOMY |

||

|

CONSUMER HEALTH |

NEGATIVE |

The consumer has been the bedrock of the US economy through much of the current expansion, and remains in a strong position. However, we have further reduced our grade to NEGATIVE as a result of the unprecedented social distancing and quarantining efforts currently being employed to fight the spread of COVID-19. |

|

CORPORATE EARNINGS |

NEGATIVE |

Coming into the year, analysts were expecting mid to single digit earnings growth, but the spread of COVID-19 is likely to have a substantial impact on near-term earnings forecasts. However, earnings could bounce back quickly once the pandemic has run its course. |

|

EMPLOYMENT |

NEGATIVE |

We have downgraded our employment grade another level as we expect the next few weeks will reveal significant job losses due to the suspension of economic activity in the services industry to combat the spread of COVID-19. |

|

INFLATION |

POSITIVE |

Inflation is often a sign of “tightening” in the economy and can be a signal that growth is peaking. The deflationary environment created by COVID-19 should provide additional room for robust stimulus from both fiscal and monetary policy initiatives. |

|

FISCAL POLICY |

VERY POSITIVE |

The CARES Act provides approximately $2.2 trillion of support for businesses and families that are impacted by the economic fallout of the COVID-19 pandemic. This is by far the largest fiscal stimulus package ever passed, and we anticipate the possibility of additional support once we emerge on the other side of the “curve”. |

|

MONETARY POLICY |

VERY POSITIVE |

In response to the threat of COVID-19, the Federal Reserve has implemented two emergency rate cuts and has moved its target interest rate back to zero. Additionally, it has announced its intention to conduct further asset purchases to support markets. We believe that the Fed is doing all it can to support the economy and markets. |

|

GLOBAL CONSIDERATIONS |

||

|

GEOPOLITICAL RISKS |

VERY NEGATIVE |

With COVID-19 being declared a global pandemic, our geopolitical risks rating is VERY NEGATIVE. However, we think it is important for investors to disentangle the public health concerns over the near-term from the expectations for markets over the long-term. The pandemic remains a near-term issue at this time. |

|

ECONOMIC RISKS |

VERY NEGATIVE |

As discussed in our commentary, COVID-19 represents a real threat to economic activity globally. However, we do expect that the eventual economic recovery will occur more swiftly than from previous economic shocks. |

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.