by Connor Darrell CFA, Assistant Vice President – Head of Investments In what might be a perfect example of why market timing is such a fallible investment strategy, the U.S. equity market generated its strongest weekly gain since 1974 last week. Investor sentiment has improved throughout much of the past couple of weeks as new data has started to show signs that the number of new cases of COVID-19 may be peaking. In the United States, the number of deaths projected by epidemiological models declined sharply last week as social distancing efforts have produced positive results.

Also

aiding the market’s recovery has been the unprecedentedly robust response from

the Federal Reserve, which announced additional measures last week to expand

lending programs in an effort to provide a backstop for businesses, households,

and municipalities impacted by the pandemic. As part of these new measures, the

Fed announced it would support new debt issuance for corporations which have

recently lost their investment grade credit ratings. Such companies, often

referred to as “fallen angels” face significant increases in borrowing costs

just as the need for cash has increased. Fed Chair Jerome Powell spoke on

Thursday in conjunction with the announcement of the new policy initiatives and

reiterated that there will be no limit to the aid that the Fed can provide

markets, other than where it is prohibited by law.

Europe Struggling to Pass Fiscal Stimulus All of the above continues to support much of what we have been communicating in recent weeks, which is that the economic impacts of the pandemic will be immense, but that the impact of swift and robust policy responses should not be discounted. These responses, however, are an important part of the puzzle when it comes to determining what the path forward will look like once we reach the other side. A coordinated and effective policy response will be essential for keeping the economy positioned for a recovery, and this creates potential problems for governments around the world which may still be struggling to find the consensus needed to legislate such a response. In Europe for example, economic crises tend to cause an elevated level of friction between the region’s more robust economies and those that are further behind in their development. Thus far, despite what economists around the globe identify as a dire situation, EU leaders have not been able to come to an agreement on a fiscal response to the crisis as a result of this friction. If the governments of the European Union are unable to reach such an agreement, the economic impacts of the virus could be substantially larger and longer lasting than what is seen here in the United States. And while we believe that the magnitude of the situation will eventually push leaders to find a solution, the ongoing discussions among EU leaders should be monitored closely.

Equities: We cautioned in our Q4 commentary that equity market returns last year were achieved on the back of stagnant earnings growth, and that “a tempering of return expectations” may be warranted moving into 2020. Of course, nobody could have predicted that just weeks later, the world would be in the midst of a global pandemic and that financial markets would have been thrown into a state of complete disarray. The rapidity with which markets retreated from their highs in response to the global spread of COVID-19 was historic, and largely representative of the massive shock that the disease poses to the global economy. Stocks across virtually every sector lost significant value, and there was largely nowhere for investors to hide. Volatility in the US equity market (as measured by the VIX) reached its highest level in history, surpassing the previous record set in November of 2008. Over the long-term, equity market returns are driven by fundamentals, but the term “fundamentals” was completely tossed aside during the first quarter as the extraordinary level of uncertainty opened the doors for panic to become the main determinant of market prices. Unfortunately, until the world is able to emerge on the other side of “the curve”, a clearer understanding of market fundamentals will not be achievable, and volatility will continue to be the norm. However, it is vital that investors continue to remind themselves that the economic impacts of COVID-19 will be transitory.

Bonds: What made the first quarter exponentially more painful for investors was that bonds (traditionally viewed as much safer than equities) were not spared from the selloff. In fact, it could be argued that when compared to historical norms, the volatility seen in the bond market was even worse. As fear and panic took hold, buyers disappeared from bond markets just as they did in equity markets, leading to a complete evaporation of liquidity and significant markdowns in bond prices. The Federal Reserve responded swiftly by committing a significant amount of capital as a buyer of last resort, and this helped to stabilize pricing toward the end of the quarter, but much of the damage was already done. Moving forward, default rates on lower quality bonds are likely to accelerate meaningfully. However, because the massive selloff occurred across bonds of all credit quality, many investors in higher quality bonds will likely recoup their losses as their bonds eventually mature and return principal.

Outlook: It goes without saying that the equity bull market finally came to an end in the first quarter, and it is likely safe to say that the second quarter of 2020 will represent the beginning of the next economic cycle. The transition from one cycle to another is always a challenging time, but we believe there are a couple of key factors that should help to keep investor fears at bay. First, both the Federal Reserve and the US Government are responding to the crisis with full force. We have no way of knowing when life will begin returning to normal and when we will be able to shift our focus to revitalizing the economy. But when that day arrives, the impact of such massive economic policy initiatives should not be discounted. The second factor that should help to preserve some level of optimism is the health of the US financial system. Many investors are still scarred by the 2008 financial crisis, but while the banking system became the epicenter of the carnage in 2008, it is likely to be an essential part of the solution today. In order for us to successfully navigate the economic challenges that lie ahead, it will be vital for the financial system to continue operating at full capacity, extending lines of credit to otherwise sound businesses which have been negatively impacted by the temporary shutdown of the global economy. The good news is that due to the stringent regulations put in place following the global financial crisis, banks come into this situation better capitalized than at any point in history, and are well positioned to do their part.

VIDEO: Q1 2020 Market Commentary Connor Darrell CFA, Head of Investments offers his perspective on the first quarter of 2020. Connor is working remotely at his home as is our entire TeamVNFA. WATCH NOW

by Connor Darrell CFA, Assistant Vice President – Head of Investments Last week brought an official end to the worst quarter for equities since the 2008 financial crisis, as the global spread of COVID-19 brought many areas of the global economy to a virtual standstill. In our latest quarterly commentary, we provide a brief summary of what became a quarter to forget, as well as an update on why there are still some key factors that should give investors reason for cautious optimism.

A Note on Our Economic Heat Map As our economic “Heat Map” has been steadily revised lower over the past few weeks, we wanted to take a quick moment to remind readers that the Heat Map is not intended to be used as a market timing mechanism. Our team tracks a variety of economic data and uses it to guide our ratings for the Heat Map. Those ratings are intended to provide a “point in time” assessment of current economic conditions and help to assess where the strengths and weaknesses lie. Of course, the present state of the global economy is drastically different than it was just three months ago, and that is the reality behind the recent reductions to our Heat Map rankings. At present, there is an incredible amount of uncertainty regarding the depth and duration of the economic impacts of the COVID-19 pandemic. Our key takeaways from the current rankings of our Heat Map are as follows:

The global economy is under immense pressure as a

result of the quarantining efforts being put in place around the globe. In the

near-term, we are likely to continue to see historically poor economic data. However,

the long-term impacts should be reduced by the incredible amount of fiscal and

monetary stimulus being pumped into the economy.

by Connor Darrell CFA, Assistant Vice President – Head of Investment Last week brought another series of large swings in equity markets as investors had to balance the still uncertain (though expectedly profound) impacts of government quarantining efforts relating to COVID-19 with historically strong economic policy responses. Markets managed to push meaningfully off of their lows, largely buoyed by optimism surrounding economic policy support. On Monday, the Federal Reserve announced that it would uncap the amount of capital it could pump into financial markets and established other means of providing liquidity to the system. This aggressive action was followed just days later with the passage of a $2.2 trillion fiscal response (known as the CARES Act) aimed at providing aid to troubled workers and businesses. Also hidden in the week’s news flow was a massive increase in claims for unemployment benefits, which skyrocketed to 3.3 million, smashing the previous record of 695,000. Additional data revealed that euro zone and Japanese manufacturing was in the midst of a sharp contraction. We expect the economic data to continue to worsen before getting better but remind investors that much of the negative data likely to come is already expected by markets, which are forward-looking by nature.

Behavioral Finance:A Primer Much

of our previous communication has been focused on providing our interpretation

of the data related to the pandemic, as well as frequent reminders of the

importance of discipline. But for many investors who are facing an

unprecedented amount of volatility in markets, remaining disciplined is much

easier said than done. As human beings,

our brains are wired to address risks and evaluate decisions in certain ways,

and in many instances, the mechanics of our cognitive functions can lead us to

make investment decisions that may prove to be contrary to our best financial

interests.

Interestingly, there is an entire field of

finance that is devoted to studying the psychology of investing. Advancements

in our understanding of the human decision-making process

have provided practitioners of “Behavioral Finance” with lots to offer in terms

of understanding the behavior of investors. In our view, one of the most

important benefits of understanding behavioral finance is that we can use our

understanding of our own psychology to help improve our investment decision

making. Below, we provide a summary of some of the most significant

psychological pitfalls and how they may negatively impact us over the

long-term:

1. Loss Aversion

All investors hate losing money, but the

concept of loss aversion goes beyond this simple notion and suggests that human

beings’ aversion to paper losses can greatly impact investment decisions.

Specifically, study after study has shown that the “pain” associated with

losing money on an investment is more powerful than the “pleasure” derived from

earning it. In the midst of a volatile market, this can cause us to feel the

urge to take action in an effort to protect ourselves from realizing further

losses, even if such action would not be in concert with our long-term

investment objectives. In order to combat this desire, it is essential for us

to focus on our goals and objectives in an effort to focus on the things we

have direct control of over time. This might include

making temporary adjustments to our savings and consumption rates or taking

advantage of cost-saving

opportunities such as lower interest rates, rather than making drastic

adjustments to our portfolios.

2. Confirmation Bias

Another flaw in the way we digest

information is confirmation bias. Confirmation bias occurs when we

inadvertently place higher emphasis on data or information that supports what

we already believe, rather than taking it into consideration at face value. For

example, if we believe strongly in the resiliency of the U.S. economy, we may

overemphasize positive information about U.S. stocks and discount whatever negative views we may

encounter that do not support

this belief. For many of us, this bias

may lead to us rushing to sell positions that have underperformed on a relative

basis and flock to those that have performed better. Giving in to these types

of biases can cause us to sacrifice proper diversification in our portfolios at

the precise time that diversification takes on heightened importance.

3. Herding

Herding is the behavior that leads to our

desire to “follow the crowd.” This is often driven by fear of regret or of

“missing out” (also known as FOMO). Throughout history, there are a plethora of

examples of points in time where market sentiment reached levels that were far

too extreme (this includes periods that fall in both bull and bear markets). In

these instances, those who were able to refrain from following the popular

decision (whether that be to buy more when stocks were expensive, or to sell

when markets were in peril) have often come out ahead. Given the volatility we

are experiencing now, it is important for us to take a step back and develop

our own conclusions rather than simply following the trend.

4. Illusion of Control

Illusion of control bias is a bias in

which people tend to believe that they can control or influence outcomes when,

in fact, they cannot. One example of this bias in a practical study occurred

when a social experiment conducted in the 1980’s found that people permitted to

select their own numbers in a hypothetical lottery game were willing to pay a

higher price per ticket than subjects gambling on randomly assigned numbers.

The belief that we have more control than we really do on the outcome of our

investment returns can lead us to take inappropriate action within our

portfolios. To combat this, it is important to think of investing as a

probabilistic activity, and that the probability of different outcomes is

beyond our control. During periods of market stress, it can be easy to lose sight

of the fact that long-term returns are driven largely by circumstances beyond

our control, and that the probability of experiencing positive returns

increases with an investor’s time horizon.

5. Representativeness

Representativeness is a type of selective memory

that causes us to place too much weight on recent evidence rather than taking a

more holistic approach to decision making. This can cause investors to focus

too much on short-term performance without considering the evidence that may be

found in the more distant past. With markets having fallen so quickly from

their highs, there are likely to be many high-quality

stocks out there which still have very promising long-term prospects but may have fallen considerably off of their

previous prices. If we become too concentrated on the recent past, or even on

the fact that these businesses may operate in industries that could be

particularly troubled in the current environment (i.e., energy or

consumer discretionary), we may be more likely to lose sight of the business’

strengths.

All of the above

biases are particularly important to consider in the current investing climate,

because they can lead us to make suboptimal decisions during a time of stress.

Behavioral economists have found that we can help to reduce the negative

impacts that our cognitive biases may have on our decision-making process just by simply acknowledging that

they exist. This can help us to remain more objective and less emotional when

considering what (if anything) should be done to adjust our portfolios in this

time of uncertainty.

by Connor Darrell CFA, Assistant Vice President – Head of Investments“There are decades where nothing happens; and there are weeks where decades happen.” (Vladimir Lenin)

It may seem counter to open a

discussion about financial markets with a quote from a communist leader, but we

felt the above was a perfect summary of what market participants have

experienced recently (and last week in

particular). In this iteration of The Weekly Commentary, we aim to put some of

the volatility in context, describe what we view to be a much needed and potentially historic economic policy

response, and hopefully address some of the concerns many investors have in

this uncertain environment.

Situation Report In just a few weeks, the COVID-19 pandemic has completely transformed the global economy and caused a massive re-pricing of risk across virtually all markets and asset classes. The uncertainty of the situation is in many ways unprecedented. The world has not faced a pandemic of this magnitude in over 100 years, and the economic costs of government attempts to slow the spread of the virus are likely to be immense. As a result, investors are understandably scared, but the types of market movements we have observed in the past few weeks only occur when panic and fear become the primary determinants of price, rather than fundamentals. The problem for markets is that the fundamentals are very uncertain at this point in time, and it is unlikely that this uncertainty will dissipate for the next several weeks.

With that as a backdrop, it is

entirely plausible that markets fall further before finding a bottom. Investors

should prepare themselves for poor economic data (particularly with respect to

the labor market) and the continued increase in the number of cases to spark

further volatility in the weeks ahead. Importantly, the slew of bad news we are

likely to see in the coming weeks makes it all the more essential for investors

to remain grounded to the core principles of investing discipline. These

principles include employing a disciplined rebalancing strategy, maintaining a

properly diversified portfolio, keeping focused on the long-term, and avoiding

making emotional decisions. As much as it can feel otherwise when we are going

through them, bear markets are temporary events. Pandemics are temporary events

as well, and we expect that the economy will emerge on the other side without

having suffered major damage to productive capacity, which is something that

cannot be said for all economic shocks throughout history.

The Policy Response In our view, this challenge will require a coordinated and targeted response using both fiscal and monetary policy tools. We are looking for (and expect) an historic response to this global crisis from policymakers. We have already seen the Federal Reserve step in to address the first key issue, which is a lack of liquidity in the financial system. Through open market operations which involve buying bonds from those looking to sell them (also known as Quantitative Easing), the Federal Reserve has committed an enormous amount of capital to provide and ensure stability in markets. We anticipate that these policies should provide some relief in the weeks ahead and continue to rate the monetary policy environment as “Very Positive” in our economic heat map.

There has also been heavy focus on

congress as investors have clamored for a fiscal response to the crisis, and we

remain optimistic that differences will be worked out and that a bill (possibly

more than one) will be passed. The initial task for policymakers is to provide

relief to those who need it while quarantines remain in place and the spread of

the virus runs its course. This will likely take several weeks. During this

time, fiscal policies should be targeted at expanding the social safety net

(through increased unemployment benefits and paid family leave) as well as providing

bridge loans for cash-strapped businesses unable to operate with society at a

standstill. Once the rate of contagion has begun to turn downward (which is

likely several weeks away), we then expect the passage of a more traditional

stimulus package aimed at spurring economic demand.

Balancing Near-Term Gratification with Missed Opportunity Over the Long-Term All of this is rather complex, but the crux of the matter is that while the impacts of the coronavirus pandemic are not likely to subside in the near-term, the eventual return to economic activity is likely to be aided by historically powerful fiscal and monetary forces. All of this suggests that it will be exceptionally difficult to time the bottom, and investors who exited risk assets during the worst of the crisis are unlikely to be able to re-enter the market at the right time. If markets continue to slide lower before finding a bottom, those same investors may experience a period of gratification in the near-term as a result of having avoided additional losses, but are just as likely to have made themselves worse off in the long-term as a result of missed opportunities for healthy returns on the back end. In short, maintaining discipline and managing emotions is key. At this point in time, it is safe for investors to approach the current environment as the start of a new economic cycle. This new cycle will bring with it its own set of characteristics and opportunities. Perhaps value stocks will finally regain market leadership? Maybe international equities will once again find their footing relative to domestic stocks? How can I construct my portfolio to maximize my opportunity to achieve my long-term financial goals? The first two questions speak to the concept of diversification. We simply do not know which types of stocks will lead the way in the next cycle (though valuation can provide us with some clues), so a balanced approach is needed. With respect to the third question, bond yields currently stand at historically low levels, making it exceptionally unlikely that goals can be achieved without exposure to equities in a portfolio. All of these questions may seem trifling in the face of a near-term global crisis but are exactly the types of issues that long-term investors should be focused on, because these are the things that ultimately determine investment success over a full-time horizon.

by Connor Darrell CFA, Assistant Vice President – Head of Investments As the threat of COVID-19, the disease caused by the novel coronavirus, has continued to escalate over the past few weeks, fear and panic have gripped financial markets and society at large. The risks emanating from the fallout of the virus’ spread have wreaked havoc on financial markets and pushed equities well into bear market territory. Since it first became apparent that containment of the virus was no longer reasonably achievable, we have spent a great deal of time trying to assess the long-term economic risks that the virus poses. The unpredictability and fluidity of the situation makes any economic forecasting extremely difficult, and that is part of the reason that markets have reacted the way they have. But in times of stress, it’s imperative that investors maintain perspective. With this edition of The Weekly Commentary, we aim to summarize some of the key facts that we have learned over the past few weeks, share our latest assessment on the economy and markets, and offer perspective on how to look forward rather than backward.

COVID-19: What Do We Know? As the scientific community has scrambled to ramp up research efforts and gain a better understanding of this novel disease, there has been no shortage of information being shared via news publications, scientific journals, and word of mouth. Despite the amount of resources being dedicated to research, the fact of the matter is that these analyses take time, and much is still unknown about how the virus operates. We do know that based on the data it has available, the World Health Organization recently made the decision to officially declare the current situation a global pandemic; a decision that many believe should have been made much earlier. We also know that scientists are finally beginning to get a handle on exactly how the disease spreads and how it compares to prior pandemic diseases.

A comparison to

prior pandemic diseases is one of the simplest ways to assess the potential

impacts of COVID-19, but it is important to note that each pandemic is unique

by nature. Coronavirus pandemics are a relatively new phenomenon (many other

pandemics throughout history have been flu viruses), so there are fewer points

of reference for the current situation, but when compared to the virus that

caused the SARS outbreak in 2002, the strain of coronavirus causing COVID-19

appears to be less lethal and have a lower rate of transmission. However, this

disease has been much more difficult to contain because patients are contagious

for a much longer period of time and often while exhibiting no symptoms at all.

As a result, modest containment measures that respond only to confirmed cases

where patients are exhibiting symptoms have been rendered ineffective.

The general

expectation among experts is that the virus will continue to spread through

community transmission, eventually reaching peak levels at some point over the

next 6-8 weeks. Faced with that reality, we anticipate widespread school

closures and recommended telecommuting by employers. We also expect economic

stimulus in the form of both monetary and fiscal policy initiatives aimed at

providing stability to markets and assurances for impacted families and

businesses. President Trump addressed the nation on Wednesday evening, offering

some preliminary measures that did not appear to appease markets, leading to

further large-scale losses during Thursday’s trading session. However, we

anticipate additional measures will be discussed and eventually passed through

Congress.

The Current State of Markets and the Economy The swift and violent nature with which markets have responded to the threat of COVID-19 has been a result of a variety of factors. First, market sentiment was extremely positive coming into the year as a result of improving economic fundamentals and anticipation for accelerating earnings growth. Those lofty expectations led to lofty asset prices, which meant stocks had further to fall once the full threat of COVID-19 became appreciated. Secondly, the exogenous shock to the economy that COVID-19 represents is not something that can be easily addressed through traditional economic policy initiatives. Lower interest rates and tax relief will not stop the spread of the virus, adding to the uncertainty of the situation. Lastly, the immediate reduction in demand for oil resulting from the spread of COVID-19 has coincided with a political struggle between Russia and Saudi Arabia with respect to oil production capacity. Both nations are looking to exert pressure on other oil producers in order to gain market share, and this has led to a sharp decline in the price of oil. Oil’s decline has resulted in a rush of “risk-off” sentiment in corporate credit markets, of which energy producing companies make up a large share of borrowers. It’s important to note however, that lower oil prices will be a net positive for consumers once the spread of the virus subsides and consumer behavior normalizes.

As might be

inferred from reading the paragraph above, the variety of threats that have

surfaced in recent weeks represent a material risk to economic activity over

the next several months. It is not out of the realm of possibility that the global

economy falls into a technical recession (defined by two consecutive quarters

of negative economic growth rates), but we believe there are a number of

reasons for investors to remain optimistic about the ensuing recovery.

First, we know

that the U.S. economy is addressing these threats from a position of strength.

As a result of significant reforms enacted following the global financial

crisis, U.S. banks are extremely well capitalized and are well positioned to

deal with potential stress. Secondly, the risks that the economy faces are

quite different from those of a “traditional” recession. Typical recessions

result from internal shocks such as an asset bubble, monetary policy missteps,

or weaknesses in the financial system. These types of recessions often lead to

structural issues within labor markets that force the reallocation of labor and

resources to different industries. For example, the housing crash and financial

meltdown in 2008 led to a substantial reallocation of resources away from construction

and real estate, and many jobs that were lost were permanently eliminated. By

contrast, as the economy emerges from the impacts of COVID-19, workers are more

likely to be able to simply return to their previous jobs and resume economic

output. At the very least, the friction we have seen in prior recessions which

has slowed the recovery in labor markets is likely to be significantly less

prevalent. As such, we believe it is reasonable to anticipate that confidence

would rebound more quickly than analyses of prior periods of economic stress

might suggest.

Lastly, given

the market’s disappointment in the President’s remarks on Wednesday, we

anticipate that the federal government will continue to look at more aggressive

policy action moving forward. In fact, we have already seen progress on this

front, as the House of Representatives passed a bipartisan legislative package

over the weekend which the Senate is expected to vote on this week. This

package will be aimed at providing assistance to impacted families and

businesses, and there are already discussions in place for further measures to

be taken as needed. We believe that the timing of additional fiscal responses

will be important, with measures focused on boosting demand being enacted after

the disease reaches its inflection point in order to maximize their impact.

Looking Forward At this point in time, equity markets are about 28% off of their previous highs. Given our assessment of the economic picture and the prospects for a relatively swift recovery (though the timing remains uncertain), we believe that the vulnerability of the human psyche has exacerbated market declines, and that market prices have begun to separate from what might be considered rational. Furthermore, the size of the selloff in equities has likely led to significant portfolio drift in many instances. And while we would never seek to “call the bottom” (and consistently advise our clients against attempting to do so), we have long preached that disciplined investors should seek to rebalance to long-term target allocations whenever portfolio drift becomes significant. This principle is true in both up and down markets. As such, rather than falling victim to the fear and panic which have gripped markets and society, we believe investors should begin looking for opportunities to rebalance portfolios. While it can often be emotionally difficult, this process involves purchasing assets such as equities which have significantly depreciated over the past few weeks. Rebalancing does not necessarily need to be achieved in one trade, but it is an important tool for keeping portfolios aligned with what is required to achieve long-term goals.

The rapidity of

the market’s reaction to the spread of COVID-19 has been historic. But as

discussed above, our assessment at this point in time is that panic has played

a significant role in what we have seen from markets, especially over the past

week. When markets are being driven by panic, a disciplined and objective

approach to portfolio management is of the utmost importance. As such, it is

important for us to focus on what we can control rather than what we cannot.

This does not only include details related to our investment portfolios

(maintaining an asset allocation that is appropriately aligned with our

investment goals), but in the wake of the mounting threat we face as a society,

it also includes simple things like proper hand hygiene, taking necessary

precautions as recommended by authorities, and working together to protect ourselves

and our communities. We do not know when the market will find its bottom or how

long it will take for our lives to return to normal, but we do know (because we

have seen it in China and in South Korea) that we will emerge on the other side.

by Connor Darrell CFA, Assistant Vice President – Head of Investments If readers of The Weekly Commentary should take one thing from this week’s edition, it should be the following: Hang in there. It’s scary, but it will normalize.

It was another week of uncertainty-fueled swings in financial markets as evidence continued to mount suggesting that the global spread of COVID-19 has accelerated. Equity investors gained a brief respite from the selling on Wednesday following Joe Biden’s better than expected performance in Super Tuesday primary voting, but the positive sentiment quickly evaporated, and stocks ended the week with just small gains. However, what positive sentiment that remained on Friday quickly eroded over the weekend after the Italian government placed about a third of the country’s population under quarantine and oil prices declined precipitously due to OPEC’s failure to reach a consensus for how to address the demand shock stemming from the spread of COVID-19.

Resilience and Discipline Remain Key The volatility we have observed over the past two weeks has been extraordinary, with daily market moves over the past 10 trading days having averaged close to 3 percent per day. On Monday morning, trading on the NYSE was halted for 15 minutes as part of procedures that have been in place since 2013. These procedures are designed to provide traders with time to take a deep breath and digest all available information, which is in fact exactly in line with what we have been recommending to investors. With that as a backdrop, we believe it is essential for investors to understand what we are seeing in markets and why.

Across both stocks and bonds, the spread

of COVID-19 has prompted the market to reassess the way in which it views risk.

The reason for that is relatively easy to pinpoint; if people are unable or

afraid to leave their homes, then there is likely to be a substantive impact on

economic activity, productivity, and manufacturing. As such, markets have begun

pricing in a much higher probability that the impacts of COVID-19 will lead to

an economic recession of some kind. Fear tends to compound on itself, and the

collective memory of 2008 still weighs heavily on investors’ minds. The

fluidity of the situation has also exacerbated volatility because news flow has

been quick and fast. In our view, this makes short-term trading even riskier

and the importance of discipline even greater.

At this point in time, it appears abundantly clear that the virus will not be “contained,” and that we will continue to see the number of cases rise around the world. What that means from an economic perspective is still unknown, and that uncertainty will continue to fuel volatility in the weeks ahead. The good news is that the U.S. economy is facing this threat from a position of strength. The catalyst is not fragility in the financial system, and it is not an asset bubble. Additionally, it is difficult to find a point in history where the U.S. consumer was healthier than it is now, and while the recent decline in oil prices has put some areas of the market under pressure, it should translate to savings for the vast majority of Americans. As such, our advice to investors remains the same. A properly constructed, diversified portfolio is equipped to balance risk and return in this environment. Panic is not an investment strategy and attempting to time markets is more akin to gambling than investing; a distinction that is incredibly important since gambling has a negative expected return over time and investing does not.

by Connor Darrell CFA, Assistant

Vice President – Head of Investments U.S.

equities generated their worst week in over a decade as fears that the novel

coronavirus might pose a real threat to economic activity began to spread. In

our view, the market action we observed last week was not based upon fundamentals,

because market participants simply don’t have that type of concrete information

available to them. The selling was, however, unsurprising as the panic that

rippled through the financial system last week was likely amplified by the fact

that equity markets had performed so strongly over the previous year. Throughout

2019, stocks generated strong returns despite minimal growth in corporate

earnings. That happened because the global economy was showing signs of

improvement and the prospects for future earnings growth were increasing. The

coronavirus represents a significant unknown that is eating away at the

positive sentiment that built up throughout last year, and investors should

expect continued volatility in markets as the situation continues to evolve.

But with all of that said, while the

coronavirus itself is new and the public health concerns very real, the fact of

the matter is that what we are seeing in markets is not out of the ordinary. Since

World War II, there have been a total of 26 stock market corrections (this one

makes 27) with an average market decline of 14.3%. Some have been larger, and

some have been smaller. What makes this correction particularly difficult is

that there are so many details we still don’t know about the coronavirus. At

what point will cases reach a peak? How

severe might the economic impacts be, and how widespread? The markets have

reacted strongly to these uncertainties because investors’ appetite for risk

tends to dissipate as more unknown variables enter the equation. In times like

these, we like to remind investors that drastic portfolio changes are unlikely

to add value over the long-term. In fact, there is overwhelming evidence that

most investors make themselves worse off by reacting too strongly to negative

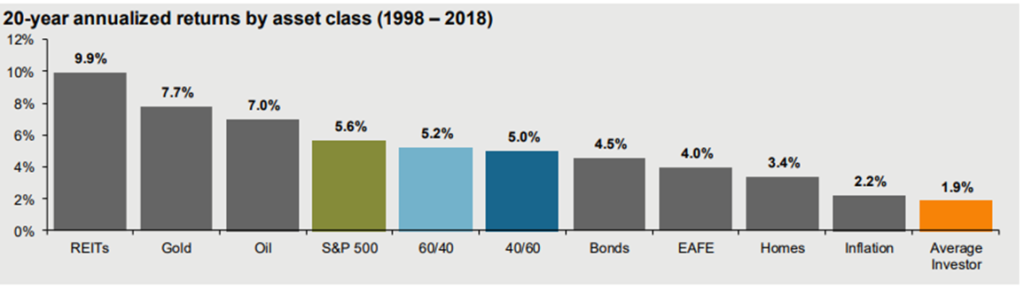

news. The below chart from JPMorgan shows the historical performance of the

average investor compared to a variety of different asset classes. The average

investor has a propensity to act emotionally during periods of market stress

and make efforts to time the markets, which has clearly led to significant

underperformance. In fact, the average investors’ mistakes have caused

portfolio returns to even lag inflation!

Source: JPMorgan Guide to the Markets

The evidence above suggests that investors

should consider the amount of fixed income in their portfolios before making

drastic decisions to exit equities en masse. For those who have multiple years’

worth of withdrawals that can be funded from bond positions, there is little

that should be done to address the pullback.

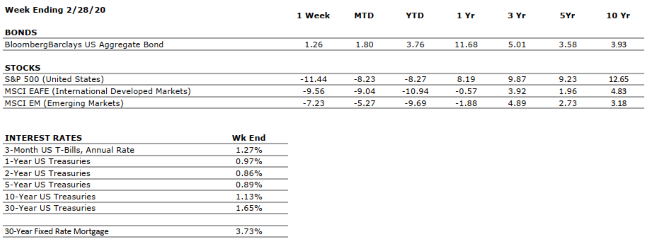

THE NUMBERS Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

U.S. ECONOMIC HEAT MAP

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

VERY POSITIVE

The consumer has been the bedrock of the US economy through much of the current expansion and we have seen little to suggest that this cannot continue.

CORPORATE EARNINGS

NEUTRAL

Corporate earnings growth was weak throughout 2019 as a result of slowing in the global economy and trade policy uncertainty. However, analysts are expecting mid to high single digit earnings growth in 2020, which will be important to sustaining recent levels of equity returns.

EMPLOYMENT

VERY POSITIVE

The economy added 225,000 new jobs in January, exceeding consensus expectations. The report also indicated that the unemployment rate ticked up to 3.6% as a result of more people looking for jobs. The expansion of the labor force should be taken as an additional sign of the confidence Americans have in the health of the labor market.

INFLATION

POSITIVE

Inflation is often a sign of “tightening” in the economy and can be a signal that growth is peaking. Recent inflationary data has increased slightly, but inflation remains benign at this time, which bodes well for the extension of the economic cycle.

FISCAL POLICY

POSITIVE

The Tax Cuts and Jobs Act of 2017 lowered the effective tax rates for many individuals and corporations. We view the cuts as a tailwind for economic activity over the next several years.

MONETARY POLICY

POSITIVE

With the potential threat that COVID-19 poses to the economy, attention is now turning to whether the Federal Reserve will take action following its March policy meeting. Markets are beginning to anticipate a rate cut from the Fed, which would provide support for market in the near-term.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

VERY NEGATIVE

Our geopolitical risks rating is now VERY NEGATIVE as there is more evidence of the coronavirus spreading outside China. However, we think it is important for investors to disentangle the public health concerns over the near-term from the expectations for markets over the long-term. The outbreak remains a near-term issue at this time.

ECONOMIC RISKS

NEUTRAL

Due to low inflation and lukewarm economic activity, central banks around the world remain in a very accommodative stance. We have seen some recent evidence of modest recovery in places like Germany, but overall, we expect global economic growth to remain modest.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

by Connor Darrell CFA, Assistant

Vice President – Head of Investments It

was a “risk off” week for global markets as stocks retreated from their highs

and bonds generated positive returns amid growing fears of further spreading of

the coronavirus. Many of those fears were realized over the weekend as evidence

emerged of a substantial increase in the number of cases outside of mainland

China, particularly in Italy, South Korea, and Iran. We have discussed in

previous iterations of The Weekly Commentary that two key areas we are focusing

on with respect to evaluating the risks posed by the virus are contagion and

severity. In our assessment of contagion, our internal discussions have focused

on evaluating whether containment efforts in China would be successful in

keeping the virus from spreading beyond Chinese borders. The significant

increase in cases outside of China over the weekend suggests to us that these

measures have likely failed. As a result, we are increasing our assessment of

geopolitical risks within our economic Heat Map from “Negative” to “Very

Negative”. Below, we provide further

details of our current thinking.

Coronavirus Update: How Should Investors Be Approaching the Issue? In our view, it is becoming increasingly likely that the spread of this disease will reach pandemic status, and many in the scientific community believe it is already at that point. There is of course a significant symbolic weight behind the word ‘pandemic’, and the simple reclassification of the current state of the coronavirus situation has the potential to strike fear into the general public. But by definition, the World Health Organization (WHO) defines a pandemic as simply “the worldwide spread of a new disease.” There is no specific standard that must be met with respect to the severity of the disease or its financial impact. It just needs to spread globally in order to reach the status of pandemic. We think that this is an important point to make, because that leaves open the very real possibility that a disease reaches pandemic status without the need for mass hysteria. In fact, the 2009 strain of H1N1 flu reached pandemic status with more than 60 million cases in the U.S. alone; and few if any of us look back at that pandemic and associate it with intense fear.

As investors, it is imperative that we

disentangle our concerns for the near-term impacts on public health from our

long-term expectations for markets. As a financial planning firm, we are

long-term investors by nature. Everything we do for clients stems from the

financial plan, which is constructed through a process that is designed to

account for bouts of market volatility stemming from exogenous shocks (such as

a pandemic virus) that may happen over the course of the implementation period.

The beauty of the technology used by financial planners when constructing

long-term plans is that we can test the resiliency of our plans across

different scenarios, and those possibilities can be baked into the

recommendations as well as into the construction of client portfolios. In our

view, as long as a financial plan is properly constructed in a way that it

aligns with an investor’s long-term goals, there should be no need for the

investor to become overly concerned with the potential near-term impacts of

these types of risks.

The important assumption that is made in

the paragraph above is that the impacts of the coronavirus will be near-term in

nature. There are multiple reasons that we continue to operate based on this

assumption. The first relates to the

severity of the disease. Looking back through history, there is really only one

pandemic illness over the last 100+ years that was severe enough to

unilaterally push the global economy into recession; and that was the Spanish

Influenza of 1918. When we compare the data currently available on the

coronavirus with what we know about the Spanish Flu, it becomes immediately

clear that the two diseases are miles apart in terms of their severity. There

are some conflicting estimates of the true severity of the Spanish Flu, but

most suggest a mortality rate somewhere in the range of 10-20%, with

significantly higher rates among certain age cohorts. The severity of the

coronavirus remains somewhat difficult to fully evaluate given that it is an

ongoing situation, but the current estimate is a mortality rate somewhere

around 3%. Furthermore, the Spanish Flu is infamous among epidemiologists for

being particularly deadly among younger, healthier adults. The data we have

thus far regarding the coronavirus is that the mortality rates are

significantly higher among older patients with compromised immune systems, much

like the seasonal flu.

The second reason we continue to operate

under the assumption of short-term impacts is recent history. An evaluation of

several of the most recent viral epidemics (including SARS, H1N1, Ebola, and

MERS) reveals that both economic and market impacts of the diseases could be

measured in quarters rather than years. It would take a particularly deadly and

long-lasting disease to alter the trajectory of economic output worldwide for

more than a couple of quarters, and until we see evidence that this disease is

capable of that, we are not sounding the alarm for investors to run for cover. It

will continue to be important for investors to keep themselves informed of new

developments, and it is our intention to provide as many updates as we can

through The Weekly Commentary, but long-term investors should continue

operating through a long-term lens.

There remains the distinct possibility that additional news flow related to the disease could continue to weigh on equity markets, so investors who have near-term spending needs and plan to draw money from their portfolios within a year should make sure they have that money available in a low-risk investment vehicle. But for many others, an adjustment to the investment strategy should not be necessary. If you have specific questions related to your situation or a change in circumstances that warrants further consideration, your financial advisor is available to help you evaluate what the best course of action might be for your unique situation.