by Connor Darrell CFA, Assistant Vice President – Head of Investments Global equity markets climbed higher for the second consecutive week despite mixed economic data and a significant reduction in forward revenue guidance by Apple, which blamed economic weakness in China for its slumping smartphone sales. The Apple announcement combined with a decline in manufacturing activity to push stocks lower on Thursday before a Friday rally was fueled by a blowout December jobs report and dovish comments made by Federal Reserve Chairman Jerome Powell. Friday’s jobs report showed that the U.S. economy added 312,000 new jobs during the month of December and revised estimates from previous months upward. Fears of an economic slowdown have been a major contributing factor to the volatility in markets over the past few months, but Friday’s employment report provided evidence that the US economy continues to add new jobs at a healthy clip, with new workers joining the labor force and real wages increasing. All of these factors should continue to support consumer spending and keep the risk of recession low in the near term.

Our Q4 Quarterly Commentary Is Now Available Each quarter, we recap the important events that drove markets and identify key themes that will impact the forward outlook. Our Q4 2018 recap can be found at valleynationalgroup.com.

What a difference three months can make. Global equity markets sold off considerably throughout the 4th quarter, with sentiment turning negative as investors pondered the consequences of further monetary policy normalization in the wake of lower expectations for economic growth and inflation. The S&P 500 briefly entered “bear market” territory (defined as a 20% decline from previous highs) on Christmas Eve before bouncing off of lows, but the selloff was large enough to push markets into negative territory (as measured by total return, including dividends) on the year for the first time since the 2008 financial crisis. However, while there are indeed some signs of a moderation of economic growth (slowing housing market and fading impact of recent tax reform), the probability of recession in the near-term remains low. History suggests that non-recessionary bear markets tend to be short-lived.

Bonds:

The Federal Reserve was a major area of focus for bond investors throughout 2018, and that continued into Q4. The Fed implemented its 4th rate hike of the year following its December meeting, but acknowledged that its previous estimate of 4 further hikes during 2019 may be too aggressive. The shift in posture from the Fed reflected a sense of restraint that was already being priced into bond markets and represented a significant change in expectations from just three months prior. In our experience, sentiment tends to shift much faster than economic data, and the data still suggests that the U.S. economy is healthy. However, the Fed will face a difficult balancing act as it continues its normalization process even as markets have begun to show signs of fragility.

The “risk-off” sentiment that dominated the 4th quarter made its way into the corporate bond market, as credit spreads (the difference in yield between corporate and government bonds) widened to their highest level since 2016. However, overall bond market performance was positive during the 4th quarter as the volatility in equity markets caused investors to seek the relative safety of fixed income. It should be noted that despite what many pundits have deemed an unhealthy environment for bond investors, the overall bond market finished the year flat. To us, this is evidence that fixed income remains an important component of a properly diversified portfolio, and that a “bad” year for bonds looks very different from a “bad” year for equities.

Outlook:

After nearly a decade of healthy returns, it is unsurprising that markets have paused to digest the changing economic environment in which we currently find ourselves. Markets managed to squeeze three-years’ worth of gains into just 12 months during 2017, and ultimately, it has been an incredibly impressive run for U.S. equities over the past 10 years. Despite the negative sentiment that has dominated markets over the past three months, it is not unreasonable to suggest that stocks can generate positive returns in 2019.

We continue to express that we believe the forward outlook for investment returns across asset classes looks very different than it did even five years ago, but that is more a product of starting point than anything else. The key areas of focus for markets moving into 2019 will continue to be trade, the Fed, and global economic growth (with a particular emphasis on China, which has showed signs of slowing). We continue to believe that the possibility of “surprises” remains skewed to the upside with respect to trade (potential deal being reached with China) and future Fed policy (slower pace of rate hikes) but believe that the Chinese economy will be important to watch moving forward. It used to be that when the U.S. sneezed, the world caught a cold. But eventually, China’s economy will be large enough that the same could be said for the world’s most populous nation.

VIDEO: Q4 Market Commentary – Connor Darrell CFA, Head of Investments, shares Valley National Financial Advisors’ review of the fourth quarter, and a first quarter 2019 outlook. WATCH NOW

by Connor Darrell CFA, Assistant Vice President – Head of Investments It was another wild ride for investors despite the holiday-shortened week. Markets were sent tumbling throughout Monday’s abbreviated trading session after Treasury Secretary Steve Mnuchin released a curiously timed statement via Twitter, informing markets that he had spoken with executives from the nation’s six largest banks and had been assured that each were suffering from no liquidity issues. The statement was confounding to market participants as it seemed aimed at addressing a concern that had not been apparent to investors prior to its release.

After the holiday, markets seemed to conclude that this was nothing more than a poorly executed attempt by the White House to stabilize markets, and Wednesday’s trading session was one of the strongest in a decade. By the end of the week, U.S. equities managed to climb out of bear market territory to generate a gain of 2.90% (as measured by the S&P 500). Bonds have continued to play their traditional role as safe haven, generating positive returns as well.

Happy New Year from VNFA Markets have been volatile in 2018, but as we have communicated previously, we do not believe that there is a need for drastic measures to be taken in portfolios at this time. CLICK HERE to access our recent market note (which summarizes our current thinking on markets).

We encourage investors to enjoy their New Year’s celebrations with friends and family and wish all TWC readers a happy and prosperous 2019!

by Connor Darrell CFA, Assistant Vice President – Head of Investments The world’s major equity indices ended lower for the second consecutive week, with some uninspiring Chinese economic data and continued geopolitical uncertainty stemming from the Brexit negotiations weighing on investor sentiment. Some of that negative sentiment was outweighed by potential progress in the ongoing trade tensions between China and the United States, but it was not enough to push markets into positive territory. In fixed income, the closely watched spread between the 10-Year and 2-Year Treasury rates held firm at 16 bps. Thus far, high quality bonds have upheld their traditional role as equity diversifiers, producing positive returns amid the recent equity volatility.

A Look Ahead at 2019 In a meaningful deviation from the prior few years, uncertainty and volatility have played a much larger role in market returns during 2018, and we anticipate this will continue into 2019. Global economic growth is likely to slow modestly, led by a deceleration in the U.S. and continued softening in China and Europe. Geopolitical uncertainties will likely remain elevated, with the market’s focus primarily fixed upon potential spillovers from the Brexit negotiations, the U.S./China trade saga, and the potentially disruptive consequences of growing populism around the world.

Despite the change in tone, its important to note that a deeper look at the fundamentals of the U.S. economy still yields no major signs of overheating, and the probability of recession remains low. For that reason, it is likely too early to become overly defensive. History tells us that late-cycle investing, while occasionally tense, can be very rewarding. As in all stages of the cycle, the key for successful investing will be relying upon the benefits of diversification within a disciplined and structured process. A properly constructed financial plan is designed to weather all stages of the economic cycle, including periods where returns are more subdued.

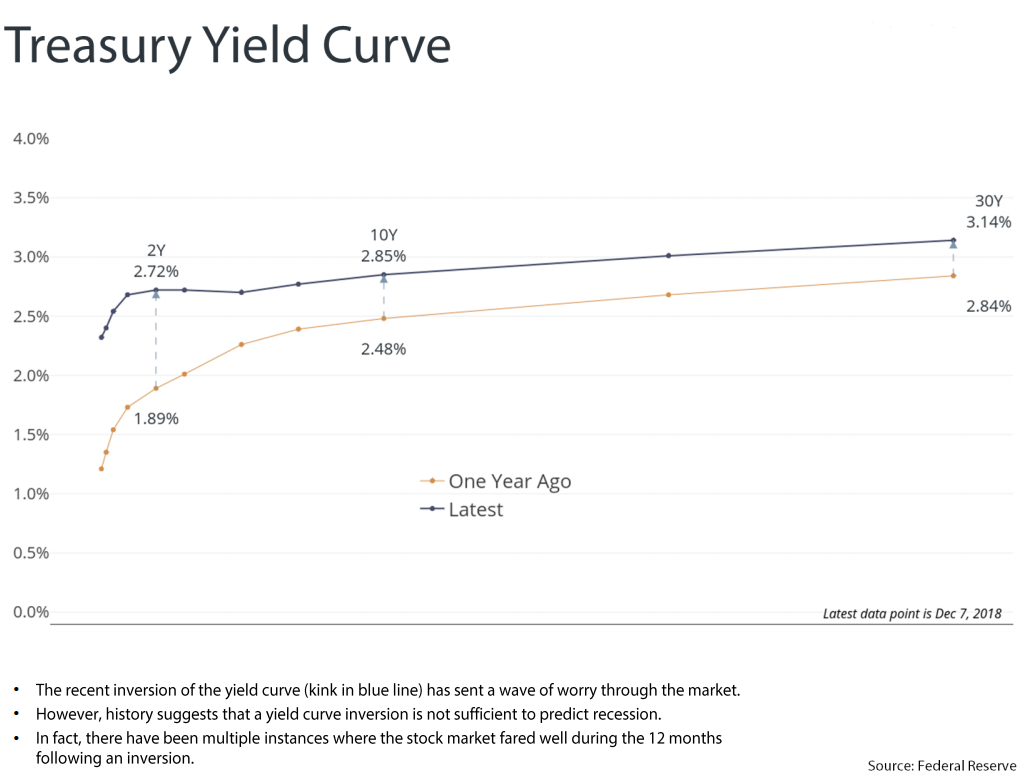

by Connor Darrell CFA, Assistant Vice President – Head of Investments Stocks traded lower in a volatile week where the key focus of investors shifted from the U.S. trade conflict with China to the shape of the yield curve. Late in Monday’s trading session, the yields on five-year Treasury notes fell below two- and three-year Treasury yields for the first time in more than a decade. Historically, yield curve inversions have been a bearish signal for the economy, and markets sold off as a result. The focus of investors will likely now move to the Federal Reserve over the next week in anticipation of its final policy meeting of 2018. The Fed is widely expected to move forward with an additional rate increase, but some have begun to question whether the recent inversion of the curve will lead to a pause. Either way, investors should likely prepare for more volatility as the uncertainty permeates through global markets.

A Historical Look at Yield Curve Inversions The recent inversion of the yield curve has sent a wave of worry through the market. However, it is important to note that while a curve inversion has typically preceded a recession, a curve inversion itself is not a sufficient condition for recession. According to Goldman Sachs Research, a historical analysis from the 1960s onward shows that in three of the last 10 instances when there has been an inversion in the yield curve, there was no recession over a subsequent two-year window. Furthermore, we have observed at least two instances since 1998 where the S&P 500 managed to achieve double digit gains over the 12 months immediately following an inversion of the three-year and five-year Treasury yields.

As the yield curve has flattened over the past several years (see chart below), the bond market has been signaling to investors that growth is likely peaking. Based on history, that fact alone does not mean that a recession is imminent, or even that the stock market has plateaued. Additionally, when we also consider the level of central bank intervention in the global economy over the past several years (where global monetary policy involved direct manipulation of short-term interest rates), it is reasonable to question whether the signaling power of the yield curve has been impacted. In any case, investors should continue to watch other market and economic indicators in order to conduct a more complete assessment of the economic cycle. We still believe that when this more holistic approach is taken, it is difficult to draw the conclusion that a recession is near.

by Connor Darrell CFA, Assistant Vice President – Head of Investments It was a strong bounce back week for equity markets, with the S&P 500 producing its largest weekly gain since December of 2011. Markets rallied strongly on Wednesday following comments made by Fed Chairman Jerome Powell in which he seemed to infer that the federal funds rate is much closer to the Fed’s target than was previously thought. Markets were also bolstered by strong online sales sentiment from the Black Friday shopping period and optimism that the G-20 summit would provide an opportunity for progress toward a trade deal with China.

On a far more somber note, both the NYSE and NASDAQ stock exchanges have announced that they will be closed on Wednesday December 5th to mourn the loss of President George H.W. Bush. Traditionally, the NYSE and NASDAQ stock markets have both closed for a day of national mourning following the death of a former president. The last such closure occurred on January 2, 2007, following the passing of former president Gerald Ford.

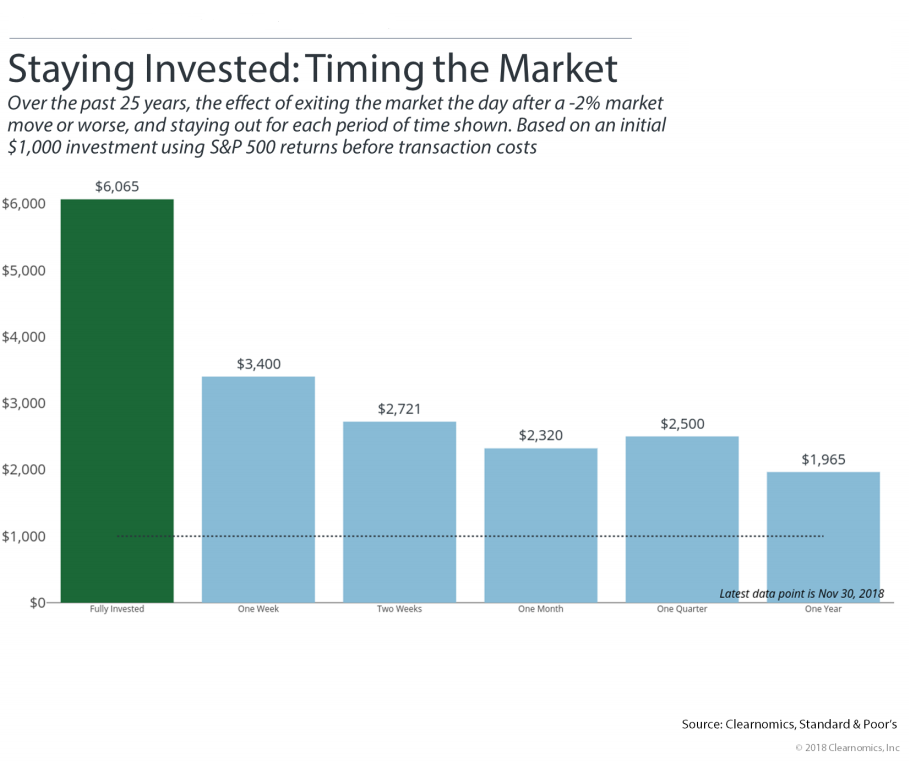

The Importance of Remaining Invested After a smooth 2017 where S&P 500 returns were positive every single month of the year (the first time this has occurred since the index was formed), the U.S. equity market has experienced two separate corrections in 2018. Corrections are a normal market phenomenon but can be a very stressful time for investors. It is human nature to feel the need to “do something” during periods of market volatility, but the data suggests that the impacts can be significant. The chart here shows the impact of exiting the market immediately following a -2% market move or worse, and the effect of remaining uninvested for a variety of time periods. The data is based upon the past 25 years of S&P 500 returns.

When we attempt to time the markets to protect gains or avoid losses, it can be easy to forget that we technically have to get that timing decision correct two separate times (once to get out, and once to get back in again). The evidence suggesting that this is a risky endeavor is overwhelming, and it can cause us to miss out on opportunities to grow and compound our wealth. The S&P 500 returned almost 5% last week, further reiterating the importance of staying invested. Any investors who sold their equities during the November selloff would have missed out on last week’s rebound and would now face a difficult decision about when to get back in.

by Connor Darrell CFA, Assistant Vice President – Head of Investments

The abbreviated week brought no respite for equity investors as global markets slid lower. U.S. stocks sold off the most, with the S&P 500 losing 3.77%. Losses were largely broad based but were a bit larger in the energy and technology sectors. However, we continue to see strong evidence that the U.S. economy remains on firm footing. A report issued by Adobe Analytics – which tracks transactions for 80 of the top 100 U.S. e-commerce retailers – suggested that Black Friday online spending was 23.6% higher than last year, providing further evidence of the strength of U.S. consumers. We continue to anticipate a very strong holiday shopping season.

Despite Agreement, Brexit Negotiations Remain a Factor After more than 20 months of negotiating, the 27 member nations (excluding Great Britain) of the European Union approved the terms of Britain’s withdrawal. The terms of the deal will now need to be reviewed and approved by British Parliament, which is scheduled to vote on December 11. However, according to the Eurasia Group, a political risk consultancy based in New York, there is a high probability that the agreement will be voted down, potentially forcing Prime Minister Theresa May into a difficult position. The official “break” date, where the UK will no longer be considered a member of the EU is March 29, 2019, and if no agreement has been approved by that date, there could be considerable ramifications for both European and British businesses. It is likely that these ramifications (which include higher costs and supply chain disruptions) will be large enough to incentivize leaders from both sides to continue working toward a final agreement, but the uncertainty surrounding a potential “no-deal” Brexit remains prominent and has been a significant contributor to the underperformance in European equities so far this year.

by Connor Darrell CFA, Assistant Vice President – Head of Investments After a brief bump following the mid-term elections, markets have struggled to maintain their footing over the past couple of weeks. That trend continued last week with the S&P 500 sliding down 1.54%. International developed markets followed suit, although the much-maligned emerging markets equity index managed a positive gain. The bond market benefitted from the volatility in equity markets as well as some dovish comments from Atlanta Fed President Raphael Bostic (a member of the interest rate setting FOMC chaired by Jerome Powell), who stated at a conference in Madrid that he does not think “we are too far from a neutral policy.” The comment suggested that fewer rate hikes may be necessary and was somewhat contradictory to the statement Jerome Powell made back in October that prompted a surge in bond yields. Ultimately, investors should continue to expect that the Federal Reserve will remain “data dependent” and will be very clear in communicating its intentions to markets.

Corporate Earnings Have Been Strong, But May be Poised to Taper Off On a year-over-year basis, Q3 earnings growth among S&P 500 companies is poised to reach its highest level since 2010. About half of that growth can be credited to tax reform, which decreased the tax burden on corporations and enabled them to report higher profits, but the other major contributing factor has been the strength of the U.S. consumer. However, despite the robust earnings growth that has been reported by U.S. companies, the equity market has failed to push meaningfully higher in 2018. This can be partially explained by the tendency for markets to be more concerned with the future rate of change of earnings, rather than the absolute numbers themselves. As the year-over-year benefits of tax reform disappear in Q1 of next year, consumers will take on the bulk of the burden in carrying earnings growth forward, and the bottom line is that earnings growth is likely to decelerate. The uncertainty surrounding how much earnings may decelerate is likely a contributing factor to some of the volatility we are observing in equity markets. We continue to believe that the economic environment is conducive to further gains, but caution that returns moving forward will be far less exciting than what investors have experienced over the past several years.

by Connor Darrell CFA, Assistant Vice President – Head of Investments Aside from a few “upsets” in individual races, there were no major surprises in the results of the U.S. midterm elections last Tuesday. Democrats managed to take control of the House of Representatives with Republicans maintaining control of the Senate. The initial reaction from markets was positive as the uncertainty surrounding the election results was lifted, although some of those gains were given up during Friday’s trading session. All in all, the U.S. equity market (as measured by the S&P 500) gained 2.21%, with international markets unable to keep pace. Bonds traded relatively flat as interest rates were largely unchanged following the Fed’s decision to stand pat at its November meeting. However, most market forecasters expect the Fed to implement one more rate hike before the end of the year.

Wages on the Rise Earlier this month, the October jobs report came in much stronger than many expected (255,000 new jobs vs. the consensus forecast of 188,000), but the number that caught Wall Street’s attention was the change in Average Hourly Earnings (AHE). AHE rose 3.14% year over year, the first time throughout this entire economic expansion that AHE growth exceeded 3%. For more than six months now, there have been more job openings available in the economy than there are unemployed workers. The logical consequence is that employers need to offer prospective employees more money in order to entice them to join their company as opposed to competitors, and it appears that the wage growth numbers are finally beginning to reflect that reality. Wage growth is an important contributor to late cycle inflation, which will be top of mind for many market strategists, as well as the Federal Reserve, over the next few months.

by Connor Darrell CFA, Assistant Vice President – Head of Investments Global equity markets generated solid gains last week despite a selloff on Friday. Friday’s volatility was sparked by a stronger than expected jobs report, which showed wages increased at the highest rate since 2009 and stoked concerns of higher inflation and an acceleration of rate hikes. Bonds also sold off as yields crept higher on the news.

Markets continue to be sensitive to any data that suggests further interest rate hikes may be warranted, but overall, the health of the U.S. economy and the robustness of corporate earnings should continue to drive returns.

Where Do We Go from Here? U.S. stocks sold off to the tune of about 7% in October, primarily as a result of rising interest rates, moderating global economic growth, and ongoing geopolitical uncertainties. As we discussed last week, part of the uncertainty permeating through markets from a geopolitical perspective is directly related to the mid-term elections. Of course, after Tuesday’s election results are finalized, any questions that markets may have about the composition of the U.S. legislative branch will be answered. Most analyses we have reviewed suggest that the Republicans have about an 80% chance of keeping control of the Senate, but that Democrats have a similar probability of taking control the House of Representatives. Ultimately, even if Democrats manage to gain control of both the Senate and the House, it is unlikely there will be any meaningful changes to federal policy. Most of the President’s policies have been enacted via executive order, and he will still maintain his veto power.

The one lingering concern will likely be the ultimate conclusion of the Mueller investigation and whether Democrats attempt to move forward with an attempt at impeachment. For obvious reasons, it is likely that markets would not react positively to such a development, but there are two reasons that we believe there is no cause for major worry at this time. First, this is likely to be a 2019 problem, rather than a 2018 one. Secondly, no matter what ultimately transpires, the markets are far more concerned about the economy and corporate earnings power than they are about disorder in Washington D.C. For now, investors will be looking to the upcoming holiday season for some relief from the recent volatility. U.S. Consumer Confidence is at an 18-year high, and if that confidence translates into spending, then markets could find good reason for festive cheer.