“True communication goes beyond talking and listening; it is about understanding.” – Gerald Campbell

Did You Know…?

by Elizabeth Wilson CPA, Vice President – Finance & Tax Services

The October 15 deadline for filing your 2018 tax return is quickly approaching. If you filed a six-month extension request by April 15, then your final return as well as any additional amount owed to the IRS is due. Here are some things to keep in mind between now and then.

- An extension to file your return does not also extend the amount of time you are given to pay your tax liability. Taxpayers with payments due when filing after the April 15th deadline should expect to pay both a late filing penalty and interest. If you are due a refund, there is good news – the late filing penalty is eliminated. For more information on how the IRS calculates penalties and interest, see the IRS website Tax Topics.

- If you can’t pay what you owe the IRS in one lump sum, you may qualify for alternative payment options. For example, if you owe less than $50,000 you most likely qualify to apply for an installment agreement which gives you an extended period of time to meet your tax obligations. Refer to the IRS Newsroom for more information.

- Self-employed individuals that have extended their return have until October 15 to fund their retirement plans. The IRS provides information on the various types of retirement plan options for self-employed individuals at IRS.gov.

As we approach the close of the 2018 tax year, it is good time to contact your financial advisor and/or tax professional to discuss tax planning for 2019. Keep in mind that Q4 2019 estimated payments are due by January 15, 2020.

The Markets This Week

by Connor Darrell CFA, Assistant Vice President – Head of Investments

There was much for the markets to digest last week, with the Federal Reserve opting to cut interest rates once again by an additional 25 bps. The committee of Fed policymakers were divided in their decision, with two members arguing that no cut was needed and one arguing for a larger cut. Stocks sold off marginally following the decision, but ultimately stabilized and were set to end the week in positive territory before news broke on Friday afternoon that lower-level Chinese officials cut their visit to the U.S. short. Markets interpreted this as a negative sign for the higher-level trade talks scheduled for early October.

In the bond market, yields crept lower as rising geopolitical risks in the Middle East seemed to push investors toward the relative safety of U.S. Treasuries. But with some members of the Federal Reserve policy committee dissenting this past week, markets will likely have less clarity about the future direction of interest rates throughout the remainder of 2019. Given this lack of clarity, investors should expect more interest rate volatility in the months ahead.

VNFA NEWS

Our team celebrated our VP of Finance & Tax Services last week as she was honored as the Rising Star at the Lehigh Valley Business CFO of the Year Awards. Elizabeth Wilson, CPA was recognized along with seven other financial professionals from non-profit and for-profit businesses at a breakfast ceremony Sept. 11.

READ MORE about the awards and event at lvb.com.

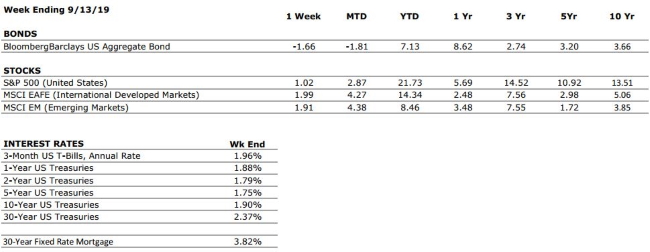

The Numbers & “Heat Map”

THE NUMBERS

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

U.S. ECONOMIC HEAT MAP

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

|

CONSUMER SPENDING |

A |

Our consumer spending grade remains an A. Surveys of US consumers continue to indicate that the consumer is in a strong position, and recent GDP data provided further evidence of healthy consumer spending. |

|

FED POLICIES |

B+ |

Our Fed Policies grade remains a B+ after the Federal Reserve opted to cut its interest rate target by 25 bps following last month’s meeting. The cut was widely anticipated by markets, and if history is any representation, it is unlikely to be the last. |

|

BUSINESS PROFITABILITY |

B- |

With most S&P 500 companies having reported Q2 earnings, the EPS growth rate for the second quarter is close to zero. Despite the weak growth rate, almost 75% of companies have beaten consensus estimates this quarter. |

|

EMPLOYMENT |

A |

The US economy added 130,000 new jobs in August, below the consensus expectations of analysts. However, despite the lower than expected job creation, there was evidence of an acceleration of wage growth. The labor market continues to look quite healthy. |

|

INFLATION |

A |

Inflation is often a sign of “tightening” in the economy, and can be a signal that growth is peaking. Despite a tight labor market, we continue to see no signs of an increase in inflation. This bodes well for the extension of the economic cycle. |

|

OTHER CONCERNS |

||

|

INTERNATIONAL RISKS |

7 |

Following a re-escalation of the US/China trade dispute, we have raised our “international risks” metric back to a 7. Other key areas of focus for markets include the ongoing Brexit negotiations, rising economic nationalism around the globe, and escalating tensions in the Middle East. |

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Quote of the Week

“Grit is that ‘extra something’ that separates the most successful people from the rest. It’s the passion, perseverance, and stamina that we must channel in order to stick with our dreams until they become a reality.” –Travis Bradberry

From The Pros… VIDEO

Pension Decisions: Lump Sum vs Payment Plan

Spend 5 minutes with Michael A. Ippoliti, MBA, CFP® as he provides an overview of the options facing individuals with pension decisions. He highlights some general pros and cons of lump sum versus monthly payments to take into consideration. WATCH NOW

The Markets This Week

by Connor Darrell CFA, Assistant Vice President – Head of Investments

Stocks logged their third consecutive week of healthy gains last week, with outperformance rotating toward small caps and value stocks. The shift into value and small cap stocks represented a meaningful change in investor preferences, which have favored large caps and growth stocks for much of the year. Bond investors saw losses as the yield curve steepened and most interest rates moved higher throughout the week. Bond yields were likely supported by stronger than expected retail sales and inflation data.

As far as economic data goes, there continues to be a disparity between measures of businesses and measures of consumers. Consumer data has remained strong as a result of low unemployment, rising wages, and relatively low inflation. However, trade uncertainties have made global businesses apprehensive to invest heavily in new projects, leading to weakening manufacturing activity and lower capital expenditures. In the absence of a trade deal, the U.S. consumer will likely continue to bear the responsibility of keeping economic momentum intact. However, an eventual deal remains our base-case scenario. In the meantime, we continue to advise against attempting to trade around short-term moves driven by speculation surrounding a trade deal. Investors would be well-served by remaining disciplined and diversified in an increasingly uncertain environment.

Oil Markets Disrupted by Attacks in Saudi

Arabia

Over

the weekend, attacks on Saudi oil assets caused major disruptions to facilities

that produce almost six million barrels of oil per day; approximately 5% of the

world’s daily oil output. Oil prices have moved higher as a result of the attacks,

and U.S. officials have made it clear that they believe Iran to be at fault and

that military action remains on the table. Putting aside the concern these

types of headlines may instill in us as global citizens, there are a few

important things to note from an investment perspective.

First, there is the obvious impact of higher oil prices. Generally speaking, higher oil prices lead to higher costs for everyday consumers. The good news is that global oil production is in a much different place than it was even five or 10 years ago, and the United States now has the ability to make up for shortfalls in global supply. As a result, it is unlikely that oil prices will be able to spike to levels that might lead economists to worry about their impact on economic activity. For perspective, West Texas Intermediate Crude prices were climbing into the low $60s per barrel as of Monday morning, far lower than the $100+ levels observed as recently as 2014.

Secondly, higher oil prices will likely provide some support for U.S. energy stocks, which have struggled year to date. Energy sector earnings have been lackluster since the precipitous drop in oil prices observed in 2015, and that has made it difficult for many energy companies to meet their profit and revenue targets. The extent to which the U.S. energy sector benefits will likely be a product of how long it takes Saudi Arabia to restore its production back to previous levels, but in the meantime, the United States’ recent investments in energy independence are likely to bear fruit.

In general, oil remains one of the most important basic resources for economic production, but the significance of events like this have declined over the past decade or so as a result of changes to the global supply network as well as advances in technology that have reduced the word’s dependence on oil. These types of events certainly require monitoring, but rarely require a change in portfolio strategy for the average investor.

“Your Financial Choices”

The show airs on WDIY Wednesday evenings, from 6-7 p.m. The show is hosted by Valley National’s Laurie Siebert CPA, CFP®, AEP®.

This week, Laurie welcomes Darlene Pors and Carla Hickey from the Chamber of Commerce Women’s Business Council to discuss: “Women in Business – Opportunities & Events.”

Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.

Valley National News

Our team, led by our CEO as Honorary Chair, is pleased to support the Volunteer Center of the Lehigh Valley Spirit of Volunteerism Awards.

Save the Date!

Nominate. Donate.

https://www.volunteerlv.org/spirit-of-volunteerism