by Connor Darrell

CFA, Assistant Vice President – Head of Investments

The

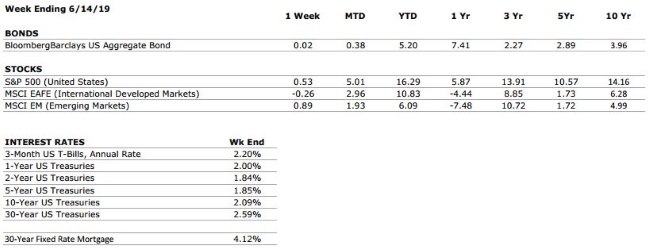

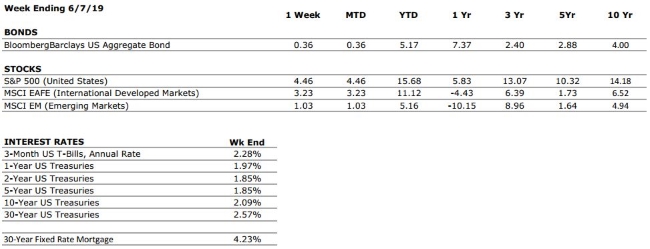

equity and bond markets continued to send different signals last week after

comments from Federal Reserve Chairman Jerome Powell helped propel the S&P

500 to new all-time highs but put further downward pressure on bond yields. The

equity market also benefitted from an announcement by President Trump that he

will hold an “extended meeting” with Chinese President Xi Jinping during the

G20 Summit in Japan this week. The ongoing trade dispute between the United

States and China continues to be a major factor for both equity markets and the

Federal Reserve, as the slowdown in trade activity is likely to be a hindrance

to economic growth. The total impact of

trade policy on economic activity over the long-term is not easily quantified,

making the Federal Reserve’s job even more difficult.

The rally in equities this month has come despite signals from global bond markets that global growth is slowing and that inflation is nowhere to be found. Equity markets are betting that central banks will have enough ammunition to stave off a meaningful decline in economic activity. Elsewhere, tensions in the Middle East have continued to push oil prices higher. On Thursday, President Trump authorized and then cancelled airstrikes against Iranian assets in response to the series of attacks that left several oil assets damaged in and around the Strait of Hormuz.

Geopolitics Not A Major Factor for Investors

In response to crippling economic sanctions that have led to a 90% reduction in the nation’s oil exports, Iranian-backed forces have begun lashing out at U.S.-allied interests in the region. The American response has been firm, leading many to speculate that the potential for a military conflict has increased. While the recent developments are concerning for a global economy that is struggling to maintain momentum (and of course even more so for the human lives that may be put in danger should tensions continue to intensify), history tells us that these types of events tend to only impact markets for a short period of time. Given the location of the risk (along a major oil trade route), we could continue to see volatility in the price of crude, but investors should avoid overreacting to geopolitical developments and maintain a disciplined, balanced allocation within their portfolios.