by

Connor

Darrell CFA, Assistant Vice President – Head

of Investments

A

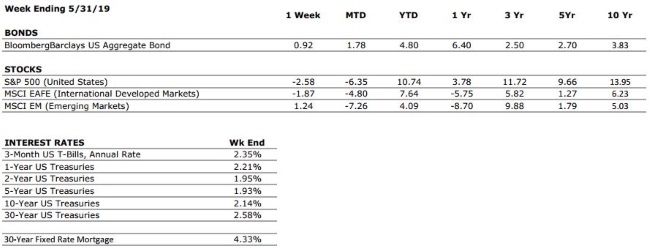

weaker than expected jobs report fed rising speculation that the Federal

Reserve will opt to lower interest rates in the coming months, leading to a

rally in equities that saw the S&P 500 rise by more than 4% last week.

Global manufacturing data also released during the week seemed to lend further

credence to this sentiment as trade tensions pushed global manufacturing

activity into contraction and down to its lowest reading since October of 2012.

It is becoming increasingly clear that the uncertainty related to global trade

is having an impact on business investment, and with the tensions likely to

persist in the near-term, investors should be prepared for additional

volatility in markets.

Don’t

Rely on the “Powell Put”

With

the sudden escalation of global geopolitical uncertainty threatening to slow

business investment and reduce economic growth, Federal Reserve policymakers

have found themselves in a very difficult (und unique) environment in which to

operate. Perhaps in response to the very high levels of uncertainty coming from

other areas of the financial world, it seems that Fed officials have made a

concerted effort to be extra communicative in recent months. For example,

during the last week of May (which included a market holiday), there were 13

separate speeches given by Fed officials; a staggering number when you consider

that the Federal reserve already meets two times per quarter and releases

detailed notes for public consumption after each meeting. It seems that the

Federal Reserve has felt the need to address the shorter-term shocks to markets

that have resulted from setbacks in trade negotiations and other geopolitical

concerns by constantly reminding investors that it is watching things very closely.

The timing of many of these statements has coincided

with rising levels of volatility in markets, leading some to refer to current

Fed policy as the “Powell Put.” With the Fed under the microscope, it is easy

overestimate its power and lose focus on all of the other factors that drive

markets over the long-term. In the

context of a $20 trillion economy, one or two 25-basis-point adjustments to

short-term interest rates are unlikely to have a profound impact on the

trajectory of economic growth, and investors would be well-served by broadening

their focus. In fact, we would argue that the most important thing for

investors to focus on is portfolio construction, and that this is the case no

matter what stage of the economic cycle we find ourselves in. The interaction

of monetary policy, the economy, and the stock market has become a defining

characteristic of the current economic cycle, but it shouldn’t be the key input

to determining the composition of one’s portfolio.

Lehigh Valley Business had invited our

Founder & Chairman, Thomas Riddle, to participate in a panel discussion

about Succession Planning at their Business Growth Symposium the morning of

June 13 at DeSales University. Tom will share his planning approach and

experience with the panel and audience.

Lehigh Valley Business had invited our

Founder & Chairman, Thomas Riddle, to participate in a panel discussion

about Succession Planning at their Business Growth Symposium the morning of

June 13 at DeSales University. Tom will share his planning approach and

experience with the panel and audience.