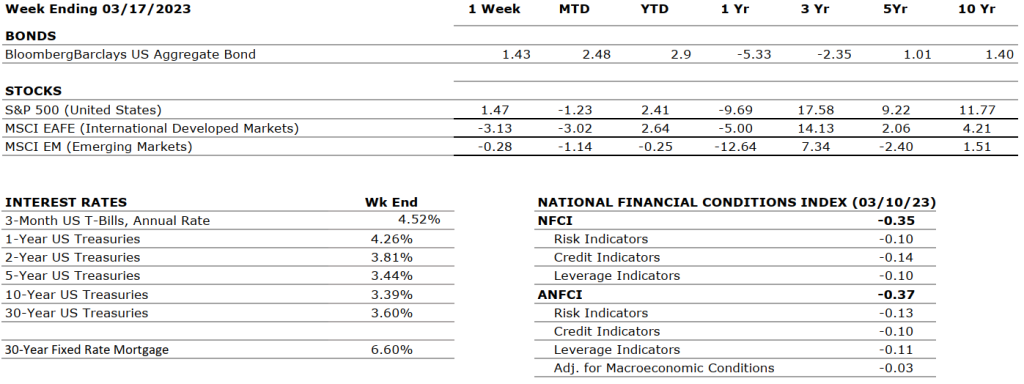

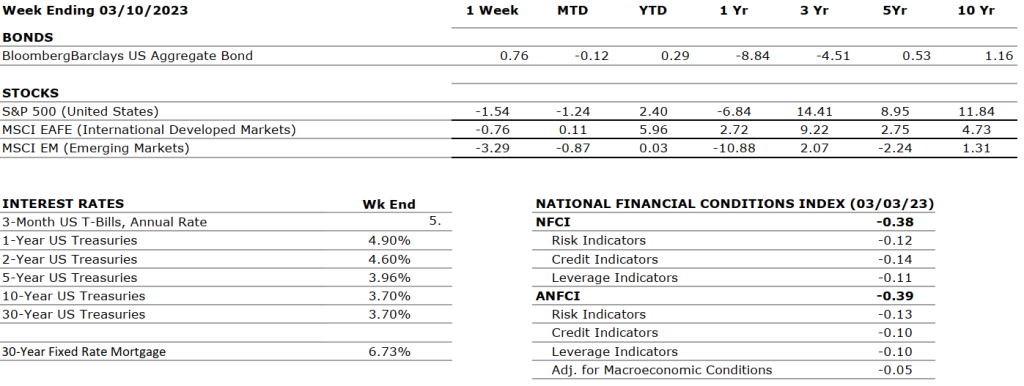

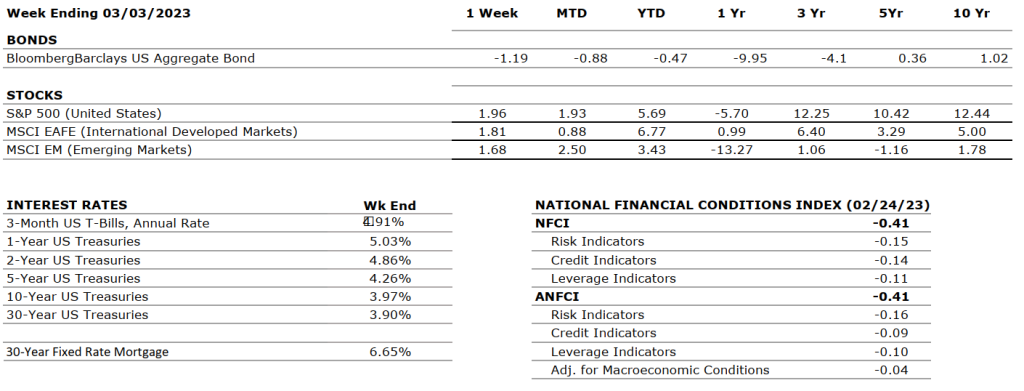

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five- and 10- yearreturns are annualized excluding dividends.Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

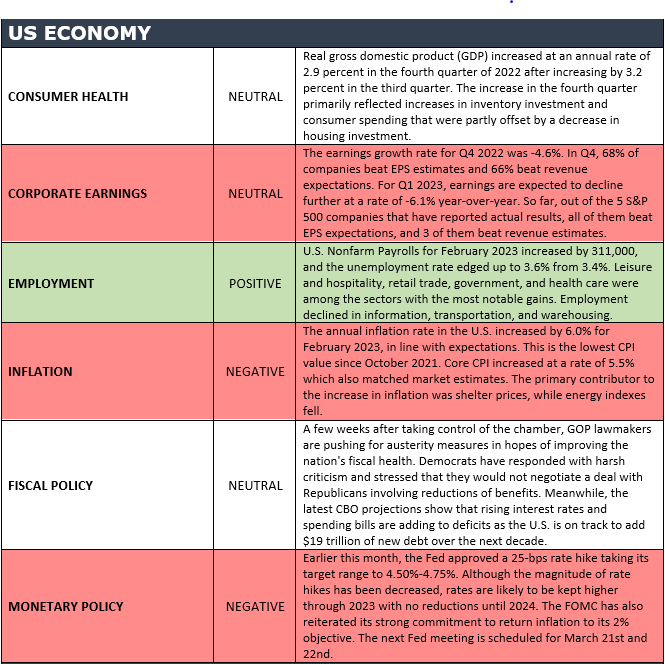

The health of the U.S. economy is a key driver of long-term returns in the stock market. Below, we grade key economic conditions that we believe are of particular importance to investors.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

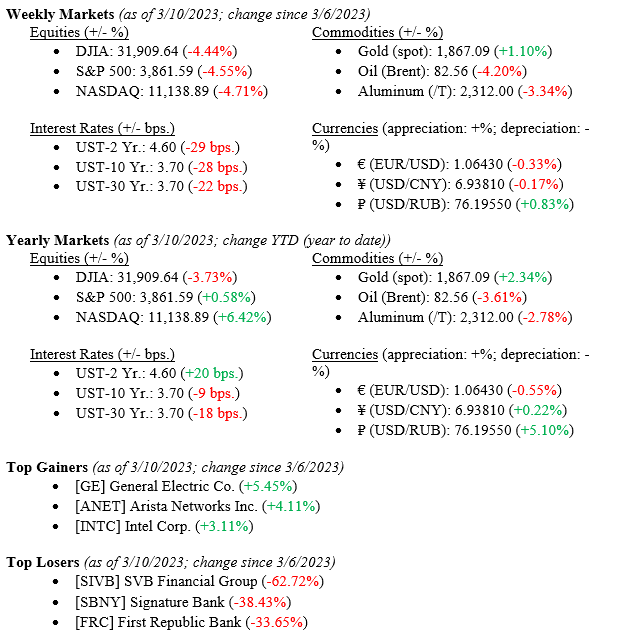

Despite last week’s dramatic sell-off across all equity market sectors, the –4.55% drop in the S&P 500 Index fails to tell the week’s full story. The Dow Jones Industrial Average was down –4.44%, and the NASDAQ fell –4.71%, in concert with the broader S&P 500 Index. The stock market’s decline directly implied strong jobs data released Friday and very hawkish comments made by Fed Chairman Jay Powell earlier in the week during his congressional testimony. By the end of the week, Silicon Valley Bank, a bank catering to tech start-ups, was on the brink of failure due to losses on bond reserve holdings, customer withdrawals, and shrinking liquidity. The FDIC seized Silicon Valley Bank, and by late Sunday evening, a new Fed liquidity facility was created and announced that depositors at Silicon Valley Bank would be made whole. We will discuss each of these events below. Meanwhile, in a massive flight-to-quality move, the 10-year US Treasury fell 28 basis points to close the week at 3.70%.

US Economy

Fed Chairman Jay Powell testified to congress for two days, first to the U.S. House of Representatives and secondly to the U.S. Senate. Chair Powell was adamant about his objectives to quell still hot-running inflation at these hearings. This message was factored into the markets and moved expectations on further Fed interest rate hikes to moves in the +0.50 – 0.75% at the March 21-22 meeting next week. As expected, markets reacted negatively to even higher than previously expected interest rates as higher rates increase funding costs, slow the economy, and increase the overall cost of expansion for corporations. This turn of events was a solid negative for markets, but the unwelcome news continued.

As mentioned above, last week Silicon Valley Bank, the so-called one-stop shop for technology start-ups in the U.S., failed as losses on its bond holdings created a liquidity crisis as depositors lined up to withdraw funds created an old-fashioned “run-on-the-bank.” Following this collapse, another tech-central bank, Signature Bank, also failed. These bank failures, while small by bank standards, prompted the Fed, the FDIC, and bank regulators to:

Seize Silicon Valley Bank and Signature Bank

Label Silicon Valley Bank and Signature Bank as new “Systemic Institutions.”

Guarantee depositors’ access to their accounts, even those over the $250,000 FDIC limit.

Create a new Bank Term Funding Program, which will provide liquidity to U.S. depository institutions by allowing them to pledge U.S. Treasury securities to the facility as collateral at PAR value. (This move by the government negates current book losses on U.S. Treasury holdings of banks and provides needed liquidity.)

This special Bank Funding program smooths/negates the duration risk that bank bond portfolios had as their holdings have lost money due to the rise of interest rates over the past year (remember, as interest rates rise, bond prices fall).

Certainly, these actions by the Fed and FDIC have stabilized the current issue impacting the banking sectors. These bank failures, again small by bank standards (Silicon Valley Bank assets were ~$200 billion compared to JP Morgan Chase assets ~ $2.6 trillion), point to a crack in the technology start-up funding world. Technology start-ups and start-up companies provide new jobs across all markets; funding these ideas is critical to their success until a replacement to funding institutions like Silicon Valley Bank are found, whether venture capital, private equity, or large banks like JP Morgan or Wells Fargo. This nascent industry will face headwinds.

Policy and Politics

There will be a lot of naysaying and gnashing of teeth this week in Washington as regulators, Fed officials, and Law Makers clash and cross-blame each other for 1) allowing banks to fail at all and 2) permitting yet another bailout by the Fed of another financial institution.

What to Watch

U.S. Core Consumer Price Index YoY for February 2023, released 3/14/2023, (prior 5.55%).

U.S. Inflation Rate for February 2023, released 3/14/2023, (prior 6.41%).

U.S. Core Producer Price Index YoY for February 2023, released 3/15/2023, (prior 5.37%).

U.S. Building Permits for February 2023, released 3/16/2023, (prior 1.339M).

U.S. Index of Consumer Sentiment for March 2023, released 3/17/23 (prior 67.00).

A massive batch of economic data is on deck for this week. Early in the week, important inflation information will be released, which will help gauge whether the Fed is impacting hard-hitting inflation that continues to hurt businesses and consumers. Mid-week building permits will add information about the housing industry and whether a spring bounce is on deck. Lastly, we will see how consumers feel as U.S. Sentiment for March 2023 is released.

In a conversation with our Founder and Chairman, Tom Riddle, over the weekend, we called on his previous experience as a bank examiner working for the U.S. Treasury Department. Tom recalled his methods for judging a bank’s health, “One does not only look at a bank’s balance sheet. A far more accurate reading is to evaluate a bank’s growth, or decline, of its net interest income.” “By this measure, banks we invest with at Valley National Financial Advisors are not those with declining or poor net interest income. However, Silicon Valley Bank would have been on such a list.” Tom continued, “banks with poor net interest income growth exhibit very unusual balance sheet characteristics such that they are lending money and offering deposit rates at levels that are higher than their investment returns.” Tom closed with, “It is a stressful time for banks that have ventured away from traditional banking.”

Looking beyond the Silicon Valley Bank meltdown, we have a busy week ahead with economic data, regulators, and lawmakers all helping to navigate the markets. The Fed may use this issue to slow or halt further interest rates, but inflation will need to continue to cool for this to happen. Meanwhile, corporate America is experiencing an unexpected earnings tailwind from cost cutting, supply chain stabilization, a declining dollar, and increased demand from China. Don’t hesitate to contact your financial advisor at Valley National Financial Advisors for help or guidance.

The Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

Real gross domestic product (GDP) increased at an annual rate of 2.9 percent in the fourth quarter of 2022 after increasing by 3.2 percent in the third quarter. The increase in the fourth quarter primarily reflected increases in inventory investment and consumer spending that were partly offset by a decrease in housing investment.

CORPORATE EARNINGS

NEUTRAL

The earnings growth rate for Q4 2022 was -4.6%. In Q4, 68% of companies beat EPS estimates and 66% beat revenue expectations. For Q1 2023, earnings are expected to decline further at a rate of – 6.1%. The forward 12-month P/E ratio for the S&P 500 is now 17.2 – below the 5-year and 10-year averages of 18.5 and 17.3, respectively.

EMPLOYMENT

POSITIVE

U.S. Nonfarm Payrolls for January 2023 increased by 311,000, and the unemployment rate hedged up to 3.6% from 3.4%. Leisure and hospitality, retail trade, government, and health care were among the sectors with the most notable gains. Employment declined in information, transportation, and warehousing.

INFLATION

NEGATIVE

The annual inflation rate in the U.S. increased by 6.4% for January 2023 compared to the December 2022 reading of 6.5%. This is the lowest CPI value since October 2021. Core CPI increased at a rate of 5.6% versus 5.7% in December. The primary contributors to the increase in inflation were shelter, food, gasoline, and natural gas. On the other hand, indexes for used vehicles, medical care, and airline fares decreased over the month.

FISCAL POLICY

NEUTRAL

A few weeks after taking control of the chamber, GOP lawmakers are pushing for austerity measures in hopes of improving the nation’s fiscal health. Democrats have responded with harsh criticism and stressed that they would not negotiate a deal with Republicans involving reductions of benefits. Meanwhile, the latest CBO projections show that rising interest rates and spending bills are adding to deficits as the U.S. is on track to add $19 trillion of new debt over the nextdecade.

MONETARY POLICY

NEGATIVE

Earlier this month, the Fed approved a 25 bps rate hike taking its target range to 4.50%-4.75%. Although the magnitude of rate hikes has decreased, rates will likely be kept higher through 2023 with no reductions until 2024. The FOMC has also reiterated its commitment to return inflation to its 2% objective. The next Fed meeting is scheduled for March 21st and 22nd.

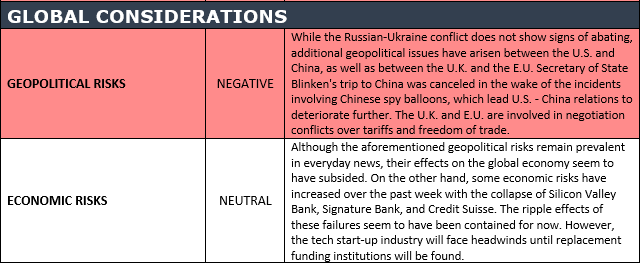

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEGATIVE

While the Russian-Ukraine conflict does not show signs of abating, additional geopolitical issues have arisen between the U.S. and China, as well as between the U.K. and the E.U. Secretary of State Blinken’s trip to China was canceled in the wake of the incidents involving Chinese spy balloons, which lead U.S. – China relations to deteriorate further. The U.K. and E.U. are involved in negotiation conflicts over tariffs and freedom of trade.

ECONOMIC RISKS

NEUTRAL

Although the aforementioned geopolitical risks remain prevalent in the daily news, their effects on the global economy seem to have subsided. On the other hand, domestic economic risks have increased over the past week with the collapse of Silicon Valley Bank, which also brought down Signature Bank, another tech-central bank. The ripple effects of these failures seem to have been contained for now. However, the tech start-up industry will face headwinds until a replacement funding institution is found.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in Wednesday, 6 PM “Your Financial Choices” on WDIY 88.1FM. Laurie and her guest Daniel Banks, President at Silver Crest Insurance, Inc will be discussing: Medicare Advantage Open Enrollment Considerations.

Women’s History Month is an annual celebration in March that recognizes and honors the contributions and achievements of women throughout history. It is held to increase awareness of women’s struggles, accomplishments, and contributions to society while promoting gender equality and women’s rights.

March was chosen as the month to celebrate Women’s History Month because of International Women’s Day, which falls on March 8th. Women’s History Month 2023 is “Celebrating Women Who Tell Our Stories.”

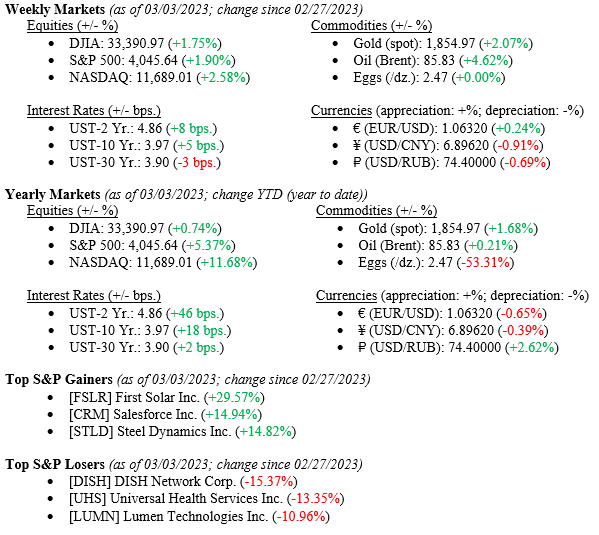

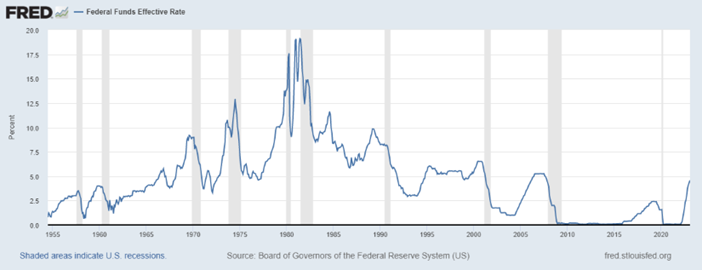

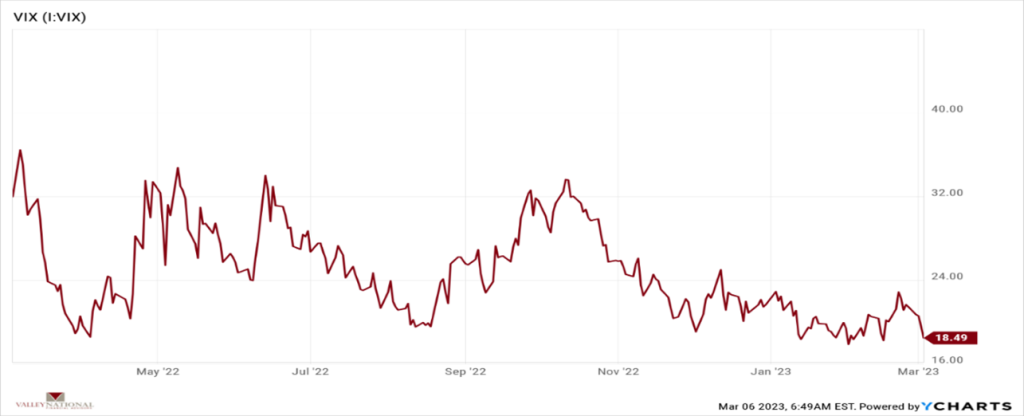

Despite U.S. Treasury Bond yields moving higher, equities notched a solid gain last week as all major indexes ended the week higher, with the Dow Jones Industrial Average rallying +1.75%, the S&P 500 Index moving up +1.90%, and the NASDAQ increasing by 2.58%. The 10-year U.S. Treasury Bond, after briefly touching 4.00% mid-week, closed the week at 3.97%. Oddly, even with higher bond yields, the VIX (Volatility Index, the CBOE Measurement of Expected Volatility) moved lower (18.49) and is down from its October high (33.63) (Chart 3). Further, Fed Fund Futures point to higher short-term rates and a higher terminal rate for Fed Funds rate around 5.25% (Chart 1). Lastly, corporate EPS (Earnings Per Share) releases for the 4th Q 2022 are over, and most were moderately higher even after many analysts projected lower EPS. After the 1st Q 2023 closes, markets will get fresh evidence of economic activity.

US Economy

Most inflation indicators are moving lower, and markets continue to point to higher short-term interest rates and a higher terminal rate for the Fed Funds Rate. Chart 1 below by the Federal Reserve of St. Louis shows the current Fed Funds Effective Rate of 4.75%. The average of Fed Fund Futures is now predicting a terminal rate of 5.25 – 5.50% by December 2023. Considering how far and fast we have moved in interest rates—from ZERO last year to 4.75% one year later—why are markets reacting so negatively to, at most, +0.75% higher from here?

It has been and continues to be our opinion at VNFA that the U.S. Economy remains healthy and will be able to easily digest up to three additional +0.25% rate hikes over the next three FOCM meetings, ending the year near 5.25 – 5.50%. Notwithstanding the 1980s inflationary period, multiple GDP (Gross Domestic Product) expansions occurred when interest rates were high, but the economy continued to grow.

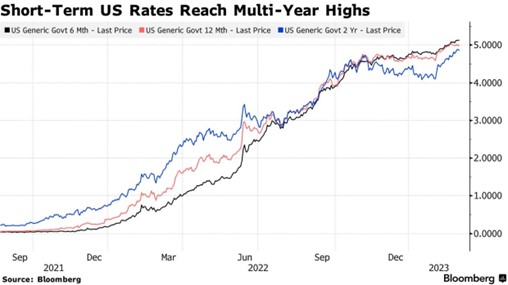

As mentioned above, bond yields continue to increase, especially in the short end of the yield curve (3 months to 2 years). Chart 2 below from Bloomberg shows generic bond yields, which continue to hit multi-year highs offering investors risk-free rates of return significantly higher than in previous years. The opportunity cost for staying out of equities and keeping safe on the sidelines by investing in short bonds (2-year yields ~5.00%) is much lower than in previous years when short rates were zero. However, we at VNFA want our investors to consider whether equity returns over the next two years will be higher than 5.00%. Given the information in front of us: bank health, labor markets, corporate earnings, and consumer spending, we believe investors still need equities in their portfolios to take advantage of future compounding returns.

Markets continue to be volatile, which is expected and common during the Fed tightening interest rates because of the implied uncertainty. However, the VIX (Volatility Index, the CBOE Measurement of Expected Volatility) moves lower. Chart 3 below from the Valley National Financial Advisors and Y Charts shows the VIX Index. The VIX decreases when there is less demand for put options (options bought by investors predicting lower equity prices). The VIX moves inversely to equity prices.

Global Economic Politics

The Russia/Ukraine war continues to muddle on without much hope for a cessation. Thankfully, a modest winter has helped EU countries avoid an economic disaster that could have happened given natural gas shortages due to the war. Sanctions on Russia have been de minimis as other countries such as China, and India has increased trade, replacing former western trading partners.

While finally coming out of zero-Covid lockdown, China has set the lowest GDP growth target in decades. Much can be said about China’s economic ambitions. Still, their new growth target of “only” 5% is telling, in that China may finally acknowledge the many issues, demographic among the most important, facing the country in the future.

What to Watch

U.S. Job Openings: Total Nonfarm, for January ‘23, released 3/6/23, prior 11.01M.

U.S. Initial Claims for Unemployment Insurance week of 3/4/23, released 3/9/2023, prior 190K.

U.S. Nonfarm Payrolls MoM (Month Over Month) for February ‘23, released 3/10/23, prior 517K.

U.S. Unemployment Rate for February 2023, released 3/10/23, prior 3.4%.

Equity markets and bond yields both ended higher last week. The Fed is on a course to reduce inflation to 2.00% while keeping full employment and a growing economy. This scenario would be considered an exceptionally soft landing and a tough one for Chairman Powell to “stick.” Every piece of the puzzle is known – higher rates, employment, economic growth. Short-term bond yields at 5.00% are incredibly enticing to investors still wounded from last year’s market wipe-out. However, wealth is gathered over exceptionally extended periods and is generational. Missing a few big days in the markets can make an enormous difference in portfolio returns, and market timing usually is a fool’s game. Stick to your investment plan and always look at the big picture rather than the minutia of daily market swings.

The Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

Real gross domestic product (GDP) increased at an annual rate of 2.9 percent in the fourth quarter of 2022 after increasing by 3.2 percent in the third quarter. The increase in the fourth quarter primarily reflected increases in inventory investment and consumer spending that were partly offset by a decrease in housing investment.

CORPORATE EARNINGS

NEUTRAL

The earnings growth rate for Q3 2022 was 2.4%. With 99% of S&P500 companies reporting actual results, the blended earnings decline was -4.6%. This is the first negative growth rate since Q3 2020 (-5.7%). Overall, 68% of companies beat EPS estimates and 66% beat revenue expectations.

EMPLOYMENT

POSITIVE

U.S. Nonfarm Payrolls for January 2023 increased by 517,000, almost three times the expected number of 187,000. The unemployment rate fell to 3.4% from 3.5% and is now the lowest in 50 years. Leisure and hospitality, health care, professional services, and government were among the sectors with the most notable gains.

INFLATION

NEGATIVE

The annual inflation rate in the U.S. increased by 6.4% for January 2023 compared to the December 2022 reading of 6.5%. This is the lowest CPI value since October 2021. Core CPI increased at a rate of 5.6% versus 5.7% in December. The primary contributors to the increase in inflation were shelter, food, gasoline, and natural gas. On the other hand, indexes for used vehicles, medical care, and airline fares decreased over the month.

FISCAL POLICY

NEUTRAL

A few weeks after taking control of the chamber, GOP lawmakers are pushing for austerity measures in hopes of improving the nation’s fiscal health. Democrats have responded with harsh criticism and stressed that they would not negotiate a deal with Republicans involving reductions of benefits. Meanwhile, the latest CBO projections show that rising interest rates and spending bills are adding to deficits as the U.S. is on track to add $19 trillion of new debt over the nextdecade.

MONETARY POLICY

NEGATIVE

Earlier this month, the Fed approved a 25 bps rate hike taking its target range to 4.50%-4.75%. Although the magnitude of rate hikes has decreased, rates will likely be kept higher through 2023 with no reductions until 2024. The FOMC has also reiterated its strong commitment to return inflation to its 2% objective. The next Fed meeting is scheduled for March 21st and 22nd.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEGATIVE

While the Russian-Ukraine conflict does not show signs of abating, additional geopolitical issues have arisen between the U.S. and China and between the U.K. and the E.U. Secretary of State Blinken’s trip to China was canceled in the wake of the incidents involving Chinese spy balloons, which lead US-China relations to deteriorate further. The U.K. and E.U. are involved in negotiation conflicts over tariffs and freedom of trade.

ECONOMIC RISKS

NEUTRAL

Although the aforementioned geopolitical risks remain prevalent in everyday news, their effects on the global economy seem to have subsided. China abandoned its zero-Covid policy, which will have a positive impact on the supply chain and the economy as a whole. The European economy also seems to be healthier than expected, partly due to an unusually warm winter that has provided some relief from increasing energy prices.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.