Laurie can

address questions on the air that are submitted either in advance or during the

live show via yourfinancialchoices.com.

Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.

According to the

US Census Bureau, the first Mother’s Day was organized by Anna Jarvis on May

10, 1908, in Grafton, West Virginia and Philadelphia, Pennsylvania. It was such

a success around the country that Jarvis asked Congress to set aside a day to

honor mothers. In 1914 Congress made the second Sunday in May Mother’s Day.

by Jonathan Susser, Investment

Technology Associate

Overview

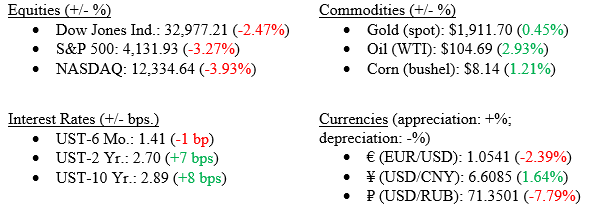

Global

pressures continue to weigh on the markets, leading to a poor week for US

equities and fixed income. Inflation remains a concern as agricultural

commodities and oil appreciate in price, hurting consumers’ wallets at the

grocery store and gas pump. The Russo-Ukrainian war continues to be a major point

of global focus as Western aid is distributed to Ukraine.

Markets (as of April 29th; change since April 25th)

US Economy

The 1Q22 earnings season continues—of the 266 companies in the S&P 500 to report so far, about 66% have beaten revenue estimates and 81% have exceeded profit expectations. For the S&P 500 overall, year-over-year sales growth is projected to be roughly 11.1% and earnings to rise approximately 0.6%, according to Bloomberg.

In March, personal income rose 0.5% over February, lower than the revised 0.7% estimate. Personal spending nearly doubled estimates of 0.6% growth at 1.1%. Savings declined month-over-month to 6.2% versus the revised 6.8% figure seen in February. Chart 1 below showcases income versus spending rates on a year-to-year basis.

Chart 1: Personal Income versus Spending Rates Year-over-Year

The PCE Deflator rose 0.9% month-over-month, meeting projections. This compares to February’s revised 0.5% increase. On a year-over-year basis, the PCE Deflator rose 6.6%, slightly below the 6.7% expected and higher than February’s 6.3% increase. The PCE Core Price Index rose 0.3% from February, and 5.2% higher than last year, slightly lower than 5.3% expectations, as seen in Chart 2.

Chart 2: PCE Core Inflation Year-over-Year

Policy and Politics

President

Biden requested $33 billion in both economic and military aid for Ukraine,

causing the Kremlin to reframe the conflict as a war against the West and threaten

retaliation. The Russian Defense Ministry claims that 1,351 soldiers have been

lost to Ukraine, while UK intelligence claims that number to be north of

15,000.

China’s

“Zero-COVID” lockdowns continue as roughly 180 million people across 27 cities remain

stuck in their homes with no end in sight. In Beijing and Shanghai alone, this

accounts for roughly 7.25% of China’s overall GDP.

What to Watch

The

Federal Reserve is expected to raise rates by 50bps at the FOMC meeting on May

4th.

US Nonfarm Payrolls data will be released on Friday,

May 6th, with estimates at 380k.

US Unemployment Rate data will be released on

Friday, May 6th, with forecasts around 3.5%.

THE NUMBERS The Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

NEUTRAL

Q1 2022 Real GDP shrunk at a 1.4% annual rate according to the first advance estimate. This is the first contraction since the beginning of the pandemic. The main factors that resulted in a decrease in GDP were a surge in imports and trade deficit highlighting that the U.S. is buying more goods from foreign countries. This may be an indication that the U.S. economy has recovered faster than other countries.

CORPORATE EARNINGS

NEUTRAL

For Q1 2022 the estimated earnings growth rate is 7.1% — the lowest since Q4 2020 (3.8%). This estimate was revised upward from the previous forecast of 6.6% in April 2022. So far, 55% of S&P500 companies have reported earnings — 80% reported a positive EPS surprise and 72% beat revenue expectations.

EMPLOYMENT

POSITIVE

Total nonfarm payroll employment rose by 431,000 in March, and the unemployment rate edged down from 3.8% to 3.6%. Job growth was widespread, led by gains in leisure and hospitality, professional and business services, retail trade, and manufacturing.

INFLATION

NEGATIVE

CPI rose 8.5% year-over-year in March 2022, the highest increase since 1982, driven by supply and demand mismatches and the additional strains on the global economy caused by the Russia- Ukraine conflict. Core CPI came in slightly below expectations (6.5% vs. 6.6%) while PPI hit the highest level on record (11.2%). Inflation concerns are clearly impacting the markets, the FED and consumer behavior.

FISCAL POLICY

NEUTRAL

Congress passed a $1.5 trillion spending package expected to be signed into law next week. Republicans rejected any additional COVID-19 related aid, which was removed from the bill. A $13.6 billion aid package to help Ukraine saw strong bipartisan support. The Violence Against Women Act was reauthorized and Democrats pushed for a 6.7% increase in domestic spending.

MONETARY POLICY

NEUTRAL

The Fed raised rates by the expected 25 bps in March and Jay Powell projected a clear path for 2022 with as many as six additional rate hikes bringing short-term rates to 1.75-2.00% by year end 2022. A 50 bps rate hike is expected at the next Fed meeting on 5/4/22.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEGATIVE

According to credit ratings agency S&P, Russia has defaulted on its foreign debt due on April 4th by offering to make payments in rubles and not dollars. Russia has 30 days to make a payment in dollars however, it is unlikely this will happen due to the current sanctions and restrictions on access to capital imposed by Western countries against Russia.

ECONOMIC RISKS

NEUTRAL

Supply chain disruptions in the U.S. are waning but the rising cost of oil due to the Russian- Ukraine war is likely to cause additional inflationary pressures not only on gasoline prices but also on many other goods and services. China’s zero-covid policy has placed Shanghai on lockdown and is increasing restrictions on other major cities including Beijing. This may result in additional supply chain issues and inflationary pressures.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Tune in Wednesday, 6 PM for “Your Financial Choices” with Laurie Siebert on WDIY 88.1FM. Laurie will discuss: Estate Planning Implementation

Laurie can address questions on the air that are submitted either in advance or during the live show via yourfinancialchoices.com. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.

Team VNFA is hard at work this week refreshing the Community Bike Works garden for our 2022 Volunteer Challenge project.

Did You Know…? Voting is open for the Volunteer Center of the Lehigh Valley Volunteer Challenge. Team VNFA is partnered this year with Community Bike Works.

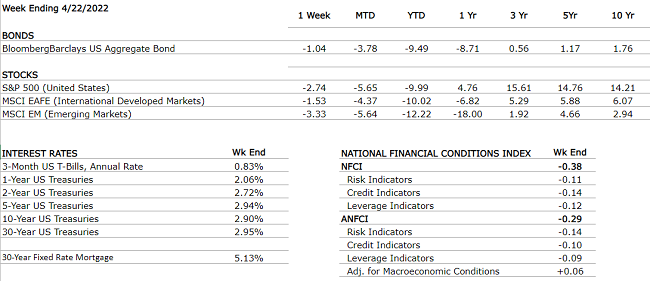

by William Henderson, Chief Investment Officer Global anxiety bled into U.S. markets, already skittish about higher rates and sticky inflation, and left us with an extremely poor week for equity and bond returns. For the week ending April 22, 2022, the Dow Jones Industrial Average fell -1.9%, the S&P 500 Index fell -2.8% and the NASDAQ lost -3.8%. The poor returns for the week only added to poor full year returns across all market sectors. Year-to-date, the Dow Jones Industrial Average is down -6.4%, the S&P 500 Index is down -10.0% and the NASDAQ is down -17.8%. The dispersion between the Dow Jones and the NASDAQ returns reminds us of the importance of a diversified equity portfolio that crosses all market sectors. Hawkish comments (meaning – those with inflation concerns and thereby calling for higher interest rates) from several Fed governors last week pushed bond yields higher once again and the yield on the 10-Year U.S. Treasury ended the week at 2.90%, seven basis points higher than the previous week.

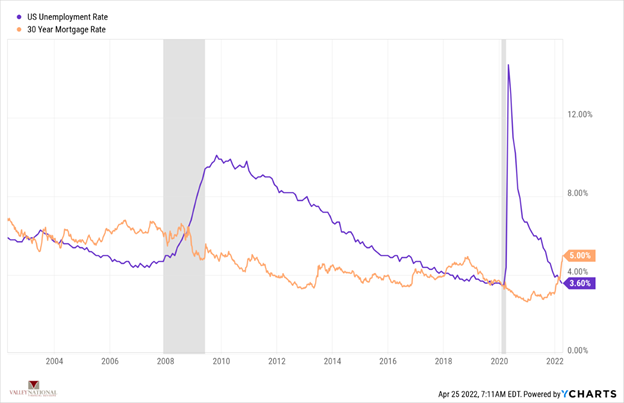

We have stated

many times about the solid condition of the U.S. economy when you consider the

consumer, the labor market and the health of banks and corporations.

Several

Wall Street prognosticators and economists are calling for a recession in

either late 2023 or 2024. We are not in

that camp, based solely on our long-standing view that recessions are almost

always

preceded by a weak housing market and poor labor conditions – neither of which

are present now. The chart

below from Valley National Financial Advisors and YCharts shows the 20-year

unemployment rate, currently 3.6%, and the 30-year fixed mortgage rate,

currently 5.00%. Both levels

support the premise that the U.S. economy is in sound financial shape as

employment is solid and mortgage rates remain

reasonable, especially for first-time home buyers.

Yet, the markets are falling

week-after-week. The markets

are not digesting the global unrest (Ukraine / Russia War), global economic

concerns (EUR region could see a recession as soon as 2023) and continued

worrisome news on COVID lockdowns in Shanghai and Beijing, China, which risk

another global supply chain meltdown. There

is an old economic axiom that states: “When

the U.S. gets a cold, the world gets the flu.” We are not willing to change

Wall Street or economic axioms here, but it would seem to us that the world has

the flu, and we are at risk of catching a cold. Our

“cold”

is certainly being exacerbated

by the Fed’s current aggressive strategy on raising interest rates.

What

is most puzzling is the reaction from the market, given the fact that the Fed

has been completely transparent on its path to higher rates.

Fed

Chairman Jay Powell is intently focused on bringing inflation under control and

closer to their 2.5% target rate and the easiest way to accomplish

this is through higher rates to quell hot inflationary pressures.

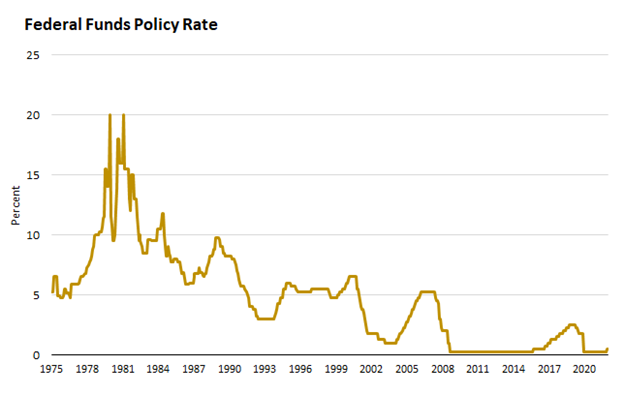

Even with higher rates on the

horizon, the economy will continue to expand at an estimated 3% in 2022,

which is strong by recent historical standards, and well below the 6% GDP

(Gross Domestic Product) growth we saw in 2021. Markets have dealt with rising

interest rates in the past and have performed quite nicely. The economy is

sound, the consumer is armed with more than $2 trillion

in accumulated savings and wage growth is accelerating, so consumers are not

reliant on borrowing or low interest rates to fuel household consumption, which

makes up 70% of GDP. Lastly, by any measure, interest rates remain

historically low and are still technically fueling economic growth.

(See

the chart below from FactSet showing the Federal Funds Rate from 1975).

Valley National Financial

Advisors recently published a piece sourced from Clearnomics, Inc. called “In

times of stress on the markets, staying with a long-term investment plan is

prudent” READ

IT HERE. The premise of the piece is that time is the key ingredient in

investing. Financial

markets are inherently volatile over days and weeks. The stock market is no

better than a coin flip, rising only slightly more than 50% of the time, and

down days tend to be much worse than up days. This can be frustrating to

investors who expect the stock market to consistently rise and achieve its

30-year average total return of 11.5% in any given year. There

have been very few instances over the span of 10 or 20 years (The Great

Depression being one) where stocks have had negative returns.

When

you add in the long-term compounding of interest and dividends, real personal

wealth is created.

Global uncertainty will continue

to persist, and markets hate uncertainty. Watch this week for earnings release

data on several important tech stocks (Apple, Amazon & Alphabet (Google))

and key inflation data on Friday. The earnings information should help with the

direction of the stock market and data will show if the Fed is starting to

reel in inflation.

THE NUMBERS The Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

US ECONOMY

CONSUMER HEALTH

POSITIVE

U.S. Real GDP growth for Q4 2021 increased at an annual rate of 7.0% compared to 2.3% in Q3 (according to second estimate). Real GDP increased by 5.7% in 2021 versus a decrease of -3.4% in 2020. For Q1 2022, estimates show GDP growing at 1.5% at an annual rate while the expected growth rate for 2022 is 3.0% year-over-year.

CORPORATE EARNINGS

NEUTRAL

For Q1 2022 the estimated earnings growth rate is 6.6% – the lowest since Q4 2020 (3.8%). This estimate was revised upward from the previous forecast of 4.5% in March 2022. So far, 20% of S&P500 companies have reported earnings – 79% reported a positive EPS surprise and 69% beat revenue expectations.

EMPLOYMENT

POSITIVE

Total nonfarm payroll employment rose by 431,000 in March, and the unemployment rate edged down from 3.8% to 3.6%. Job growth was widespread, led by gains in leisure and hospitality, professional and business services, retail trade, and manufacturing.

INFLATION

NEGATIVE

CPI rose 8.5% year-over-year in March 2022, the highest increase since 1982, driven by supply and demand mismatches and the additional strains on the global economy caused by the Russia- Ukraine conflict. Core CPI came in slightly below expectations (6.5% vs. 6.6%) while PPI hit the highest level on record (11.2%). Inflation concerns are clearly impacting the markets, the FED and consumer behavior.

FISCAL POLICY

NEUTRAL

Congress passed a $1.5 trillion spending package expected to be signed into law next week. Republicans rejected any additional COVID-19 related aid, which was removed from the bill. $13.6 billion aid package to help Ukraine saw strong bipartisan support. The Violence Against Women Act was reauthorized and Democrats pushed for a 6.7% increase in domestic spending.

MONETARY POLICY

NEUTRAL

The Fed raised rates by the expected 25 bps in March and Jay Powell projected a clear path for 2022 with as many as six additional rate hikes bringing short-term rates to 1.75-2.00% by year end 2022. The probability of a 50 bps rate hike in May is now estimated at 91%.

GLOBAL CONSIDERATIONS

GEOPOLITICAL RISKS

NEGATIVE

According to credit ratings agency S&P, Russia has defaulted on its foreign debt due on April 4th by offering to make payments in rubles and not dollars. Russia has 30 days to make a payment in dollars however, it is unlikely this will happen due to the current sanctions and restrictions on access to capital imposed by Western countries against Russia.

ECONOMIC RISKS

NEUTRAL

Supply chain disruptions in the U.S. are waning but the rising cost of oil due to the Russian- Ukraine war is likely to cause additional inflationary pressures not only on gasoline prices but also on many other goods and services. China’s zero-covid policy has placed Shanghai on lockdown and is increasing restrictions on other major cities including Beijing. This may result in additional supply chain issues and inflationary pressures.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.