We are hiring! Team VNFA is seeking an Investment Technology Associate to work as part of our Investment Department. Join Our Team – Valley National Financial Advisors

Current Market Observations

by William Henderson, Chief Investment Officer

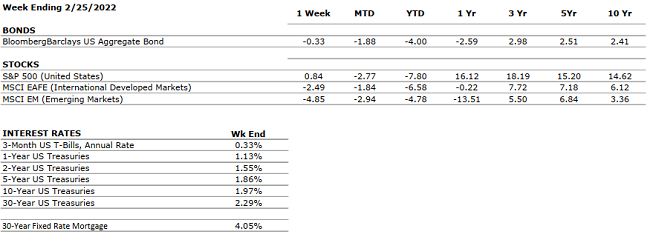

Market volatility prevailed last week as the Russia / Ukraine “crisis” spiraled into a full-scale invasion and war between the two countries. On a continent that has been free of international aggressions of this sort since WWII, Russia acted unilaterally and invaded Ukraine. International reaction was mostly unified with quick condemnation from all countries except China, who remained silent. Markets ended the week on a mixed note, but wild price swings of 500 and 1000 points (on the Dow Jones Industrial Average) were common all week. The Dow Jones Industrial Average fell -0.7%, the S&P 500 Index gained +0.1% and the NASDAQ lost -0.2%. Year-to-date returns remain well in negative territory for all three major indexes. Year-to-date, the Dow Jones Industrial Average is down -6.0%, the S&P 500 Index is down -7.8% and the NASDAQ is down -12.4%. Even bonds were not spared last week in the modest sell-off as the yield on the 10-Year U.S. Treasury rose five basis points week-over-week to end at 1.97%.

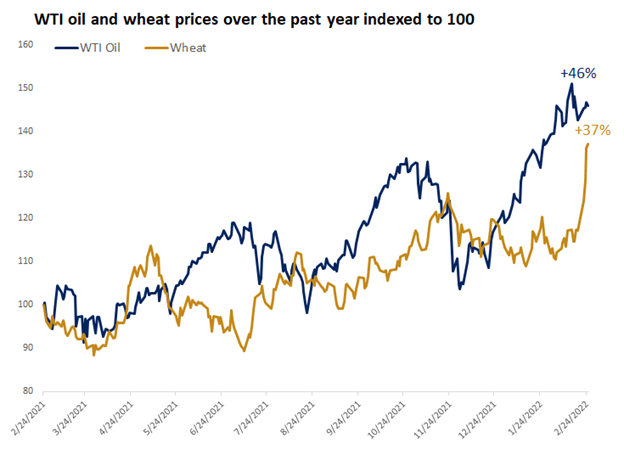

The Russian invasion has spiked market volatility, increased uncertainty around the pace of the global recovery from the pandemic and thankfully brought unilateral financial sanctions to Russia. Volatility results simply from the uncertainty surrounding the duration of the Russia / Ukraine war and the impacts it is having on commodity prices; as Russia is a significant producer of several major global commodities such as oil, wheat, and palladium (a critical rare earth used in catalytic converters). See the chart below from FactSet showing the recent spikes in prices of oil and wheat.

Thankfully, the reaction from the global community to the Russian invasion has been dramatic and financial sanctions such as limiting access to SWIFT banking channels and freezing of $630 billion of foreign reserves have already had an impact. Russia has closed its stock market, and the Russian Central Bank raised short-term rates from 9.5% to 20% to defend the tumbling Ruble. Of course, the reaction by the Russian people was a run on banks and ATMs in a last dash effort to get hard currency before an expected crash. Beyond financial sanctions and hardship on Russians themselves the international community has been swift in condemning Vladmir Putin personally and supporting Ukraine as much as possible. Given Ukraine is not a NATO country but borders several including Poland and Romania actual military support will be precarious and certainly measured baring a full-scale global conflict.

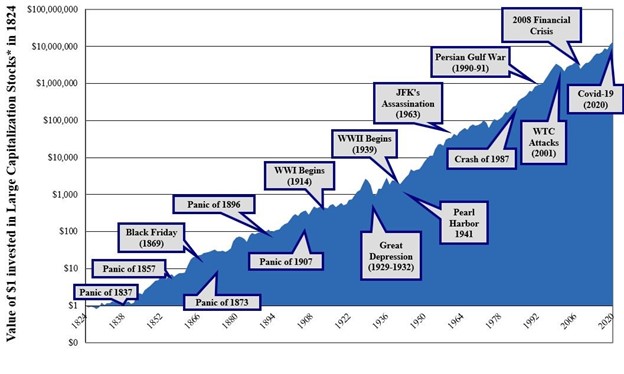

As mentioned, fear, uncertainty and volatility are never associated with good times in markets – in fact quite the opposite. However, historically, markets look past geopolitical events and move higher over extended periods of time; and that alone should be an investors’ focus. (See the chart below from Haverford Trust & Ibbottson. Associates showing major geopolitical events and the increase in $1 invested in Large Cap Equities).

While the underlying strength in the U.S. economy and thereby the markets exist, the current global uncertainty will prevail and grab all headlines. Higher commodity prices, specifically oil, have the propensity to impact the recovery and ongoing growth in the economy. Whether sanctions will prevail, and Russia retreats or U.S. policy makers impact markets by releasing strategic petroleum reserves, opening the Keystone XL pipeline or allow fracking again, we shall have to see. Typically, sell-offs in markets are short-lived and offer buying opportunities for longer-term investors. This week Fed Chairman Jay Powell reports to Congress and we may hear comments around the pace of rate hikes and balance sheet reduction in 2022. That story is significantly more important than what we are hearing from our national news media. Lastly, on Friday we will get another reading on U.S. employment conditions as the February jobs data is released.

The Numbers & “Heat Map”

THE NUMBERS

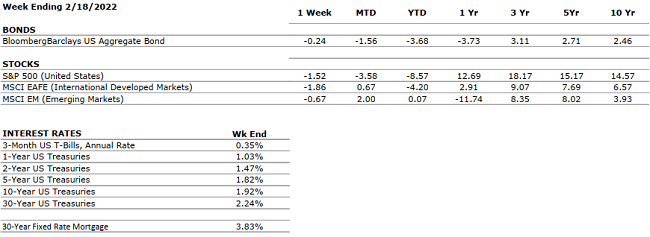

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

|

US ECONOMY |

||

|

CONSUMER HEALTH |

POSITIVE |

U.S. Real GDP growth for Q4 2021 increased at an annual rate of 6.9% compared to 2.3% in Q3 (according to advance estimate). The acceleration was driven primarily by private inventory investment. Real GDP increased by 5.7% in 2021 versus a decrease of -3.4% in 2020. Disposable income saw a slight increase of 0.3% and personal saving rate decreased to 7.4% in Q4 from the previous 9.5% in Q3 highlighting increased consumer spending. |

|

CORPORATE EARNINGS |

POSITIVE |

Fourth quarter earnings are showing strong results with 76% of companies that reported earnings so far beating estimates by an average of 8.2%. Some notable positive (Amazon) and negative (Facebook) surprises in big tech. Revenues also well above estimates with 77% of S&P 500 companies reporting actual revenue above forecasts. Blended earnings growth rate for 2021 was 47%. |

|

EMPLOYMENT |

POSITIVE |

U.S. Payroll Report for January U.S. added 467,000 jobs in January, beating estimates of 125,000. Red-hot private sector hiring drives the payrolls surge. Revisions add 709,000 jobs in prior two months. Unemployment rate rises to 4% from 3.9%. |

|

INFLATION |

NEGATIVE |

CPI rose 7.5% year-over-year in January 2022, the highest increase since 1982, driven by the global supply chain backlog and continued consumer pent up demand. Inflation concerns are clearly impacting the markets, the FED and consumer behavior. |

|

FISCAL POLICY |

NEUTRAL |

The Build Back Better Bill has been scaled back from $2.2 trillion to a $1.8 trillion version as Senator Manchin continues to hold back support. President Biden has mentioned the idea of breaking up the BBB Bill into smaller pieces to be able to pass fractions at a time. The economy seems to be digesting a new world where fiscal policy is no longer considered an economic stimulus. |

|

MONETARY POLICY |

NEUTRAL |

Fed discussed a triple threat of tightening: raise interest rates, halt purchases, and reduce its balance sheet (reducing holdings of Treasurys and mortgage-backed securities). Gradual and steady reduction of liquidity will be key in preserving market performance (fast and sudden changes would most likely result in panic-driven sell offs). |

|

GLOBAL CONSIDERATIONS |

||

|

GEOPOLITICAL RISKS |

NEGATIVE |

The Russian invasion into Ukraine has now turned into a full-blown global event. US, UK and EU authorities are taking many steps to cripple Russia including closing their access to SWIFT. Commodity prices are spiking along with Oil. COVID-19 concerns continue to abate and re- openings are more the norm than closures and lockdowns. The CDC is easing rules. |

|

ECONOMIC RISKS |

NEUTRAL |

Supply chain disruptions in the U.S. are waning but now there are trucker protests on the Canadian / U.S. border. Canada is the second largest trading partner with the U.S. (after China) but our largest export market. |

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

Quote of the Week

“Peace cannot be kept by force; it can only be achieved by understanding.” – Albert Einstein

Tax Corner

The IRS warned earlier this month to stay vigilant as scammers work year-round: https://www.irs.gov/newsroom/irs-warning-scammers-work-year-round-stay-vigilant

If you receive an e-mail from CCH-ReturnNotification@wolterskluwer.com with the subject: “2021 Electronic Return Accepted by the IRS” – it is a real confirmation and not a scam. This e-mail message is generated from our tax software provider to let you know that the IRS has received your return. There is no action required.

“Your Financial Choices”

Tune in Wednesday, 6 PM for “Your Financial Choices” with Laurie Siebert on WDIY 88.1FM. Laurie will discuss: Talking to Children About Finances

Laurie can address questions on the air that are submitted either in advance or during the live show via yourfinancialchoices.com. Recordings of past shows are available to listen or download at both yourfinancialchoices.com and wdiy.org.

VNFA NEWS

Team VNFA is pleased to share that we are partnering with with Community Bike Works for the 2022 Volunteer Challenge. For our project, we will be restoring their garden which is located at Keck Park’s bike shop. Prior to the COVID-19 pandemic, this garden was used to grow vegetables for healthy snacks and meals as part of their youth program. Our team is excited about the opportunity to bring this garden back to life. Meet our partner and follow our journey to the May 11th Challenge! Community Bike Works – We Teach Lessons Through Bicycles (communitybikeworks.org)

Tax Corner

Remember to provide the amount of the Recovery Rebate Credit (also known as the Stimulus Payment) you received in 2021 with your tax documents. The Recovery Rebate Credit was $1,400 for each eligible individual ($2,800 for a joint return) plus $1,400 for each dependent. The IRS distributed the advanced refund based on 2019 or 2020 returns starting in March 2021. The payment was either a direct deposit, check or a prepaid debit card, so make sure to check their records / bank statements to see if this was received. While it is not considered taxable income, it is important to let your tax preparer know if you received that money.

REMINDER: If you are using your eVault Client Portal to upload tax source documents. Please put them together and upload one file or as few files as possible. When you are finished, e-mail our Tax Department at tax@valleynationalgroup.com.

Current Market Observations

by William Henderson, Chief Investment Officer

Gangbuster numbers in retail sales and existing home sales failed to move markets higher as the continued unrest in the Russia / Ukraine put a damper on the markets. President Biden spoke towards the end of the week and said, “he believed an invasion by Russia into Ukraine was imminent.” That is all the fragile markets needed to chalk up another losing week across all three major stock market indexes. The Dow Jones Industrial Average fell -1.9%, the S&P 500 Index lost -1.6% and the NASDAQ lost -1.8%. Weekly returns added to a poor year so far in 2022, and all three major indexes are sitting on negative year-to-date numbers. Year-to-date, the Dow Jones Industrial Average is down -6.0%, the S&P 500 Index is down -8.6% and the NASDAQ, which naturally tilts to growth stocks and is much more sensitive to interest rates moves, is down -13.3%. Fortunately, as we have said over and over, when risk assets sell off, investors flee to the safety of bonds. Treasury rates moved lower across the curve 1-5 basis points: while the 10-Year U.S. Treasury Bond remained unchanged at 1.92%.

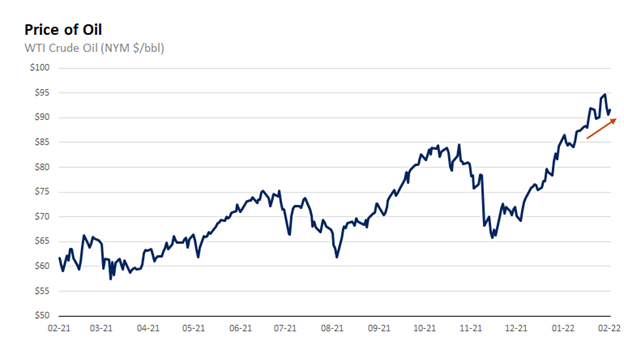

The geopolitical situation remains fragile, but markets have typically tended to look past lesser geopolitical crises, instead focusing on where there may be pockets of economic impact. For example, Russia remains one of the largest oil producers especially in the European region where it also supplies up to 40% of natural gas to the region. We’ve certainly seen an impact on oil as the price of a barrel of West Texas Intermediate (WTI) has increased over the past several months. See the chart below from FactSet of the price of WTI since February of 2021.

Oil is a critical component of many things well beyond simple heating and gasoline and the impact of higher oil prices are felt everywhere. As recent as 2019, the United States was completely oil independent producing enough energy to supply our own needs. The current administration killed the Keystone XL and banned new fracking on day 1 of taking office.

Beyond the Russia / Ukraine situation there were pockets of good news, as mentioned above. Sales of existing homes rose +6.7% in January from the prior month to a seasonally adjusted rate of 5.5 million units, according to the National Association of Realtors. The housing market remains extremely competitive even in the face of rising mortgage rates in recent months. Additionally, U.S. retail sales for the month of January came in well ahead of expectations at +3.8% vs estimates of +1.9%, despite continued noise around the omicron variant. Retail sales increased in online sales, furniture and autos. As mentioned last week, the consumer remains well positioned to fuel the great “second reopening” of the economy especially as we move into spring and summer travel season.

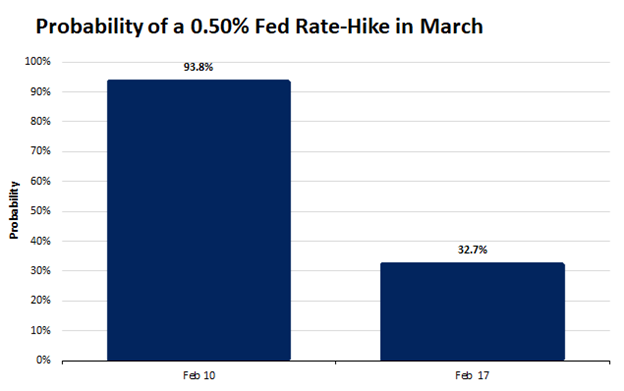

A final piece of economic news released last week was the Fed minutes from the January FOMC meeting. The minutes provided some comfort to the markets as they did not seem overly hawkish (higher rates) and contained no material surprises. Economists had been predicting a +0.50% rate hike at the March 15-16 meeting; but the minutes revealed a Fed willing to raise rates at a gradual and measured pace. Almost immediately, markets adjusted the probability of a +0.50% rate to less than 33% from 94% (see chart below from FactSet showing the change in rate expectations from February 10 to February 17).

In our opinion, this is good news for the markets. Inflation is running at a level that warrants higher interest rates but interest rates also fuel the economy so it can be a slippery slope for the Fed – raise rates to combat inflation but don’t kill the economic growth we are seeing. We believe a series of +0.25% rate hikes in a gradual, measured, and transparent manner is the right recipe for the Fed to quell inflation but continue to allow economic expansion. We further expect a gradual flattening of the yield curve (curve showing interest rates over time from short-term Treasuries to long-term bonds) as short rates rise but pressure on longer-term bonds continues due to pension funds, foreign buyers and investors seeking bonds as a risk management tool in their portfolios.

This week we get a few more economic indicators including Revised 4th Quarter GDP (prior +6.9%) and U.S. Initial Claims for Unemployment. It is a holiday-shortened week and headlines will be dominated by the situation with Russia / Ukraine, and less so by the sound foundation underlying the growing U.S. economy.

The Numbers & “Heat Map”

THE NUMBERS

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

|

US ECONOMY |

||

|

CONSUMER HEALTH |

POSITIVE |

U.S. Real GDP growth for Q4 2021 increased at an annual rate of 6.9% compared to 2.3% in Q3 (according to advance estimate). The acceleration was driven primarily by private inventory investment. Real GDP increased by 5.7% in 2021 versus a decrease of -3.4% in 2020. Disposable income saw a slight increase of 0.3% and personal saving rate decreased to 7.4% in Q4 from the previous 9.5% in Q3 highlighting increased consumer spending. |

|

CORPORATE EARNINGS |

POSITIVE |

Fourth quarter earnings are showing strong results with 76% of companies that reported earnings so far beating estimates by an average of 8.2%. Some notable positive (Amazon) and negative (Facebook) surprises in big tech. Revenues also well above estimates with 77% of S&P 500 companies reporting actual revenue above forecasts. Blended earnings growth rate for 2021 was 47%. |

|

EMPLOYMENT |

POSITIVE |

U.S. Payroll Report for January U.S. added 467,000 jobs in January, beating estimates of 125,000. Red-hot private sector hiring drives the payrolls surge. Revisions add 709,000 jobs in prior two months. Unemployment rate rises to 4% from 3.9%. |

|

INFLATION |

NEGATIVE |

CPI rose 7.5% year-over-year in January 2022, the highest increase since 1982, driven by the global supply chain backlog and continued consumer pent up demand. Inflation concerns are clearly impacting the markets, the FED and consumer behavior. |

|

FISCAL POLICY |

NEUTRAL |

The Build Back Better Bill has been scaled back from $2.2 trillion to a $1.8 trillion version as Senator Manchin continues to hold back support. President Biden has mentioned the idea of breaking up the BBB Bill into smaller pieces to be able to pass fractions at a time. The economy seems to be digesting a new world where fiscal policy is no longer considered an economic stimulus. |

|

MONETARY POLICY |

NEUTRAL |

Fed discussed a triple threat of tightening: raise interest rates, halt purchases, and reduce its balance sheet (reducing holdings of Treasurys and mortgage-backed securities). Gradual and steady reduction of liquidity will be key in preserving market performance (fast and sudden changes would most likely result in panic-driven sell offs). |

|

GLOBAL CONSIDERATIONS |

||

|

GEOPOLITICAL RISKS |

NEUTRAL |

The Russia/Ukraine situation is very fluid with comments from Vladmir Putin, Volodymyr Zelenskyy and Joe Biden being part of the mix each day. COVID-19 concerns continue to abate and re-openings are more the norm than closures and lockdowns. |

|

ECONOMIC RISKS |

NEUTRAL |

Supply chain disruptions in the U.S. are waning but now there are trucker protests on the Canadian / U.S. border. Canada is the second largest trading partner with the U.S. (after China) but our largest export market. |

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.