by William Henderson, Vice President / Head of Investments

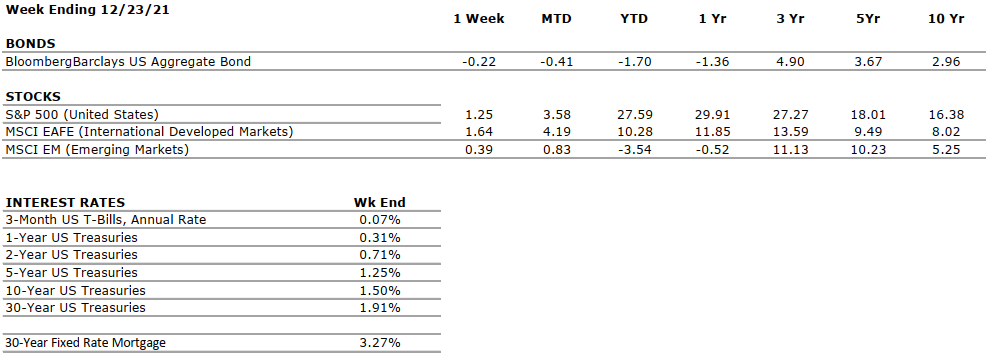

A shortened Christmas Holiday week pushed markets higher even in the face of increased omicron variant threats and global travel snafus. The Dow Jones Industrial Average rose +0.2%, the S&P 500 Index gained +1.2%, and the NASDAQ gained a healthy +3.1%. Further, year-to-date returns remain well into near-record territory for 2021. Year-to-date, the Dow Jones Industrial Average has returned +19.7%, the S&P 500 Index +27.6% and the NASDAQ +22.2% giving us solid returns across all market sectors. With the healthy returns in risk assets, as expected, bonds sold off. The 10-year U.S. Treasury bond rose by nine basis points to close the week at 1.50%. The fixed income markets react as quickly as the stock market to good news or bad news and each market reminds us why investors own each asset class. Equities remain a portfolio’s return generator and bonds remain a portfolio’s risk management tool.

As mentioned above, the week gave

us mixed news on the pandemic and its

impact on the U.S. economy and financial markets. Cases of the omicron variant

spread rapidly in pockets of

the country, and the government

announced an initiative to distribute COVID-19 tests to the public for

free.

Lastly,

regulators

approved two new pills that will be available by prescription for those who are

sick with COVID-19.

In a revision to last quarter’s

GDP, the U.S. government reported economic growth last quarter was slightly

stronger than it had estimated previously. In its final estimate released last

Wednesday, GDP growth in the third quarter was 2.3%,

an

upward revision from the original release of 2.1%.

By comparison, GDP accelerated at annual rates of 6.4% and 6.7% in the first

and second quarters of 2021,

respectively. A

report on Bloomberg showed that Christmas

shopping, both in person “bricks and mortar” and online was much stronger than

2020. According

to the report by Mastercard SpendingPulse, U.S.

holiday sales jumped 8.5% from last year as consumers spent more money on

clothes, jewelry, and electronics. Sales

boomed across the board during the holiday season defined as November 1 to

December 24. Many consumers were savvy

shoppers and started earlier than normal,

most likely due to widely reported supply chain concerns,

which in the end, were largely unfounded rumors as most retailers were

plentifully stocked with goods.

As we move into 2022, it is

important to keep the markets in perspective. Certainly, central

banks globally are taking a more hawkish tone and higher short-term rates are a

given next year, but that information is already priced into equities. Two

questions are typically bantered about: 1) Is the market going higher or lower

today? 2) Is today a good day to buy (invest)? And

my answer to both questions is always the same – YES. Yes,

the markets will go up or down today and YES, today is a good day to buy

(invest). Long-term positive returns on

investment portfolios are driven by long-term investment plans and a commitment

to sticking to your investment plan. We’ve

seen this all year as the market

rallies

back as quickly as it sold off. Perspective

and commitment are what matter the most.