by Connor Darrell

CFA, Assistant Vice President – Head of Investments U.S.

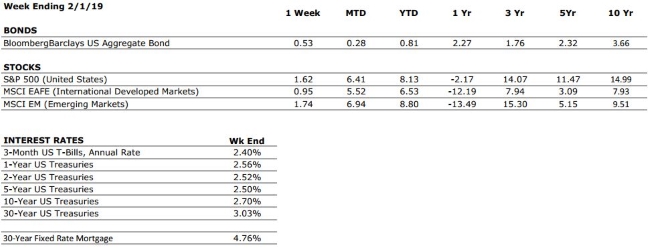

stocks posted positive returns for the eighth straight week despite unexpectedly

disappointing retail sales data. Stocks were primarily supported by optimism

that the U.S. and China might make progress on a trade agreement before U.S.-imposed

tariffs are set to more than double on March 1. Bond yields jumped higher to

start the week but reversed course following the weak retail sales data

released on Thursday. Bonds ended the week relatively flat as a result.

Starting Point Matters We have consistently warned of the potential perils of attempting to time the market, and the past few months have only served to lend further credence to those warnings. But that doesn’t mean that investors should not consider point-in-time analyses when evaluating their long-term strategy. Following the tumultuous end to 2018, markets have rebounded considerably, and risks now look evenly balanced. We continue to believe that while recent economic data has sent mixed signals to investors, the probability of a U.S. recession in the near-term remains low. However, the reality is that we find ourselves in what is very likely to be the latter stages of the economic cycle, and this fact carries long-term implications for investors. Given the stage of the cycle in which we currently find ourselves, investors need to be aware that the long-term expected returns across asset classes look quite a bit lower than they did in the past. The successful implementation of an investment plan is a dynamic process that responds to the market environment. As such, in an environment where market returns will be lower, investors may need to consider saving more or spending less in order to stay on track.

The show airs on WDIY Wednesday

evenings, from 6-7 p.m. The show is hosted by Valley National’s Laurie Siebert

CPA, CFP®, AEP®.

This

week, Laurie and her guest Attorney Charles Stopp, from the law firm

of Steckel and Stopp, will discuss:

“Special Situations and Elections in Inheritance Tax

Filings.”

Laurie and Attorney Stopp will take your

calls on this or other topics at 610-758-8810 during the live show, or via yourfinancialchoices.com.

Recordings of past shows are available to listen or download at both yourfinancialchoices.com and

wdiy.org.

2019 Volunteer Challenge Project Our team is pleased to announce our 2019 non-profit partner for the Volunteer Challenge. Paxinosa Elementary in Easton is located in the West Ward and is designated as a Trauma Sensitive School. With the help of our Communities in Schools coordinators, Valley National is going to create a much-needed “Just Press Pause” room for teachers to recharge, reset and reduce stress.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

US ECONOMIC HEAT MAP

The health of the US economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

CONSUMER SPENDING

A+

Consumer confidence was hindered somewhat by the market volatility experienced during December. We are awaiting further data from the US Department of Commerce (which was delayed due to the government shutdown) in order to make an assessment regarding whether this merits a new grade.

FED POLICIES

C-

The Federal Reserve implemented its fourth interest rate hike of the year in December. Rising interest rates tend to reduce economic growth potential and can lead to repricing of income producing assets.

BUSINESS PROFITABILITY

B+

Corporate earnings remain strong, but we anticipate earnings growth will taper off in 2019. We are also beginning to see a higher number of companies reducing forward earnings guidance, a sign that earnings growth may have reached its peak in 2018.

EMPLOYMENT

A+

The US economy added 304,000 new jobs in January, soundly beating estimates for the second straight month. The labor market is one of the strongest components of the economic backdrop at this time.

INFLATION

B

Inflation is often a sign of “tightening” in the economy, and can be a signal that growth is peaking. The inflation rate remains benign at this time, but we see the potential for an increase moving forward. This metric deserves our attention.

OTHER CONCERNS

INTERNATIONAL RISKS

5

The above ratings assume no international crisis. On a scale of 1 to 10 with 10 being the highest level of crisis, we rate these international risks collectively as a 5. These risks deserve our ongoing attention.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

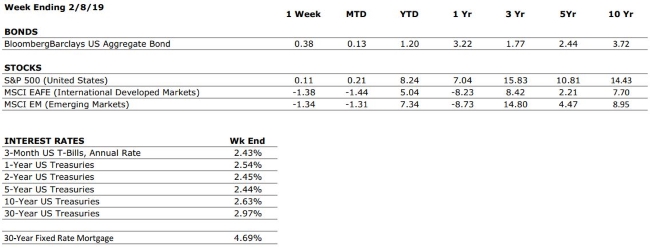

by Connor Darrell CFA, Assistant Vice President – Head of Investments Global equity markets weakened a bit last week, posting mixed results after news reports suggested that U.S. and Chinese leaders are unlikely to meet before the “trade truce” expires on March 1. Sentiment across markets has remained far more positive than it was at the latter end of 2018, with credit spreads declining to their lowest level since November. Government bonds also fared well as yields continued to decline. The yield on the 10-Year Treasury Note dropped to close the week at 2.63%, down from its high of 3.24% back in November.

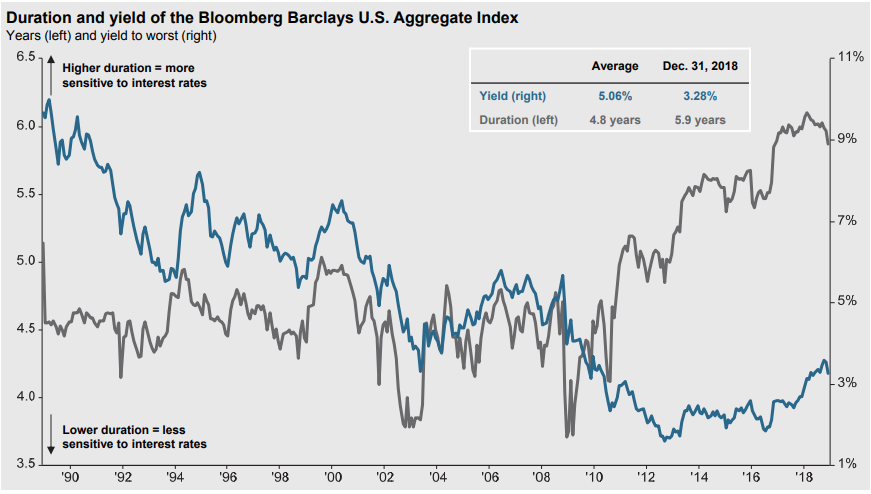

How Bond Investing Has Changed Since the Financial Crisis In the world of finance, everything is interconnected, and sometimes it can be incredibly enlightening to take a look at how a change in one area of the economy can have long lasting impacts on global financial markets. The post financial crisis monetary policy environment (marked by artificially low interest rates and high liquidity) has influenced nearly every corner of the economy and the investing world. One major byproduct has been a significant shift in the composition of major bond indices, particularly the Bloomberg Barclays U.S. Aggregate. Over the past 11 years, the yield offered by the average bond in the index has unsurprisingly come down, but the average maturity has also grown longer. Those longer maturities have increased the duration of the index, which is a measure used by bond investors to evaluate how sensitive an investment is to changes in interest rates (see chart provided by JP Morgan Asset Management).

To understand what has transpired, we need to assess the decision making of bond issuers. Low interest rates mean low borrowing costs for corporations, and that provides an incentive for businesses to seek longer term financing (in order to lock in lower rates for a longer period of time). This has changed the mix of securities that make up the index, leading to a higher proportion of longer-term bonds. Passive bond investors should be aware of the changes in the composition of the underlying index being tracked, as the risk/reward outlook for the Bloomberg Barclays Aggregate has become less attractive (lower yields and higher rate sensitivity). In the context of the active vs. passive debate, the proponents of active management may have the strongest argument when it comes to fixed income, where an active manager may be able to manage the tradeoff between yield and duration more effectively.

The show airs on WDIY Wednesday evenings,

from 6-7 p.m. The show is hosted by Valley National’s Laurie Siebert CPA, CFP®,

AEP®.

This week,

Laurie will address: “Tax

Questions from Listeners.” Laurie will take your calls on this or

other topics at 610-758-8810 during the live show, or via yourfinancialchoices.com.

VNFA In the Community We are proud to support our community of estate professionals as a sponsor for the Estate Planning Council of the Lehigh Valley’s seminar today on “Estate Planning in a World of Rapidly Advancing Technology.” As technology plays a bigger role in our financial lives, it is critical that we understand how it impacts our estate planning in accessing our accounts and in securing digital assets. We will share more with you on this important topic in the future.

The Estate Planning Council of the Lehigh

Valley was founded in 1967 by a group of 10 estate planning

professionals. As an Accredited Estate Planner (AEP®), our own Laurie

Siebert is part of the board for the council. In addition to her

participation, many others from our advisory team are council members. Laurie

also discusses Estate Planning topics regularly on “Your Financial Choices,”

which airs weekly on WDIY 88.1FM. Visit yourfinancialchoices.com to

listen to recent recordings on this and other related topics.

Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized excluding dividends. Interest Rates: Federal Reserve, Freddie Mac

US ECONOMIC HEAT MAP

The health of the US economy is a key driver of long-term returns in the stock market. Below, we grade 5 key economic conditions that we believe are of particular importance to investors.

CONSUMER SPENDING

A+

Consumer confidence was hindered somewhat by the market volatility experienced during December. We are awaiting further data from the US Department of Commerce (which has been delayed due to the government shutdown) in order to make an assessment regarding whether this merits a new grade.

FED POLICIES

C-

The Federal Reserve implemented its fourth interest rate hike of the year in December. Rising interest rates tend to reduce economic growth potential and can lead to repricing of income producing assets.

BUSINESS PROFITABILITY

B+

Corporate earnings remain strong, but we anticipate earnings growth will taper off in 2019. We are also beginning to see a higher number of companies reducing forward earnings guidance, a sign that earnings growth may have reached its peak in 2018.

EMPLOYMENT

A+

The US economy added 304,000 new jobs in January, soundly beating estimates for the second straight month. The labor market is one of the strongest components of the economic backdrop at this time.

INFLATION

B

Inflation is often a sign of “tightening” in the economy, and can be a signal that growth is peaking. The inflation rate remains benign at this time, but we see the potential for an increase moving forward. This metric deserves our attention.

OTHER CONCERNS

INTERNATIONAL RISKS

5

The above ratings assume no international crisis. On a scale of 1 to 10 with 10 being the highest level of crisis, we rate these international risks collectively as a 5. These risks deserve our ongoing attention.

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.

We are proud to support our community of estate professionals as a sponsor for the Estate Planning Council of the Lehigh Valley’s seminar today on “Estate Planning in a World of Rapidly Advancing Technology.” As technology plays a bigger role in our financial lives, it is critical that we understand how it impacts our estate planning in accessing our accounts and in securing digital assets. We will share more with you on this important topic in the future.

We are proud to support our community of estate professionals as a sponsor for the Estate Planning Council of the Lehigh Valley’s seminar today on “Estate Planning in a World of Rapidly Advancing Technology.” As technology plays a bigger role in our financial lives, it is critical that we understand how it impacts our estate planning in accessing our accounts and in securing digital assets. We will share more with you on this important topic in the future.